As the markets hit that magical percent drawdown number, market experts tell us we are in a bear market.

If only they told us sooner…

Inflation was not transitory after all, and the Fed needed to react which led to the typical result from raising rates quickly… Again, who could predict that mailing money to everyone while supply chains were broken would result in higher prices? Too much money chasing too few goods is the classic definition of inflation. With “mailbox” money intersecting in addition to supply constraints it couldn’t have been any clearer! If only they raised rates a little, tiny bit as they mailed money to people, it could have directed the support money to where it was needed – buying necessary goods to survive. True, some of the money ended up as savings in banks or paid down debt but a substantial amount went to the NASDAQ, private equity, speculative crypto investments and luxury goods.

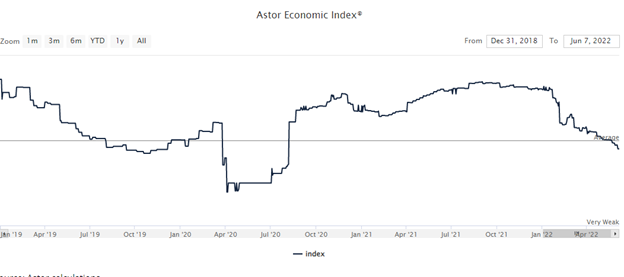

What has happened is all the market appreciation that was associated with unproductive economic activity funded by low rates, stimulus or government spending is being sucked out and we are headed back to where we started before COVID March 2020. It is as if the last two years never existed, and we are starting from that point. They couldn’t buy an expansion and the markets are giving us the engagement ring back. The question to now ask is “will the level act as support, stabilizing the stock market and then we head back up and an expansion begins after the 1.5% contraction in Q1?” I don’t know for sure, but my guess is we stabilize and then head back down to where a garden variety recession would have taken us in 2020 (as the Astor Economic Index had started to indicate in 2019).

The Fed missed this one by a mile. The inflation was NOT transitory, no matter which definition you use, and prices for most things (especially wages) are inelastic on the downside. This is the biggest stimulus followed by an enormous spending bill that is creating the largest inflation I can remember. My conclusion is that we will need the largest ammunition to fight this, and it will be longer and harder than most anticipated. In my opinion, this is a ~50% decline correction, but not all at once. We generally don’t have a huge recession when the economy is adding 300k jobs a month. However, the market and asset prices have exploded from enormous liquidity and suddenly that liquidity has halted and that’s what’s happening. This recession will be hardest felt on asset prices alongside places that benefited most from the combination of low rates and excess liquidity. Labor and the middle-income work force will have a better time dealing with this recession then past recessions. This is because the relationship between Labor, capital, and resources has shifted and changed how recessions impact these pillars.

Inflation is not going away, and rates are not coming back down. In fact, markets can survive higher rates but they need visibility first. Since the Fed was blind to the outcome of the spending and stimulus, I think it is a long time before they have visibility the markets like. This time things that are scarce should do fine. Resources that are limited or hard to produce, labor of special skill sets (even menial but a specific skill set) will do better than commodities services. This one is going to be complicated….

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index® : The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-282879-2022-07-07