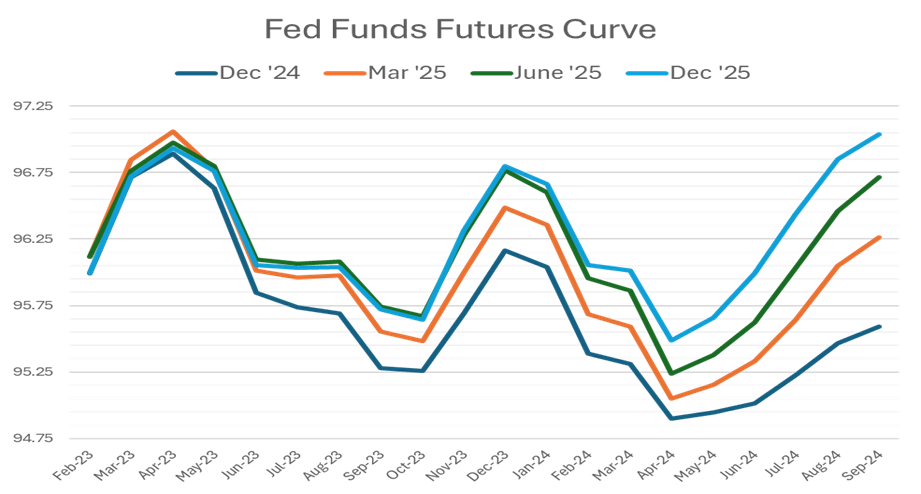

As we navigate the final stretch of 2024, it’s evident that the financial markets have become increasingly optimistic about potential Federal Reserve rate cuts. Recent movements in the Fed Funds futures market, in particular, highlight this growing optimism. Specifically, the market is currently pricing in 100 basis points of cuts across the remaining three meetings of this year, with an additional 150 basis points anticipated for 2025 (chart 1). However, we believe this exuberance might be misplaced.

Chart 1

Source: Bloomberg

Historical Perspective and Current Trends

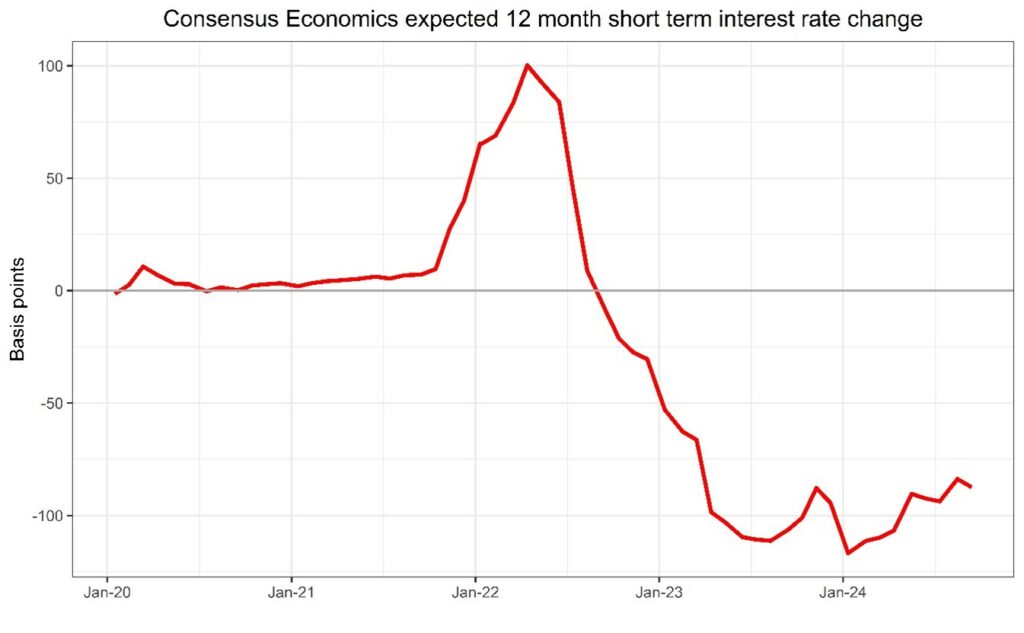

A glance at historical trends reveals that economists have been anticipating interest rate cuts for the past two years, only to face disappointment as the Fed maintained a more cautious stance. This pattern is illustrated below (Chart 2), which tracks economists’ recent expectations for changes in the fed funds rate. Despite persistent forecasts for easing, the Fed has consistently surprised the market with its steady approach to monetary policy.

Chart 2

Economic Indicators and Fed’s Stance

Our proprietary Astor Economic Index®, a gauge of economic conditions, has shown a steady increase since the beginning of the year, although recent data/reports in this quarter have caused the index to ease a bit. Currently, the index measures economic growth to be slightly above average, suggesting a resilient economy. While recent payroll reports indicate a downward trend, they still reflect stable if not healthy economic activity, a crucial pillar of economic stability. Nevertheless, we should remain vigilant for any emerging signs of labor market weakness.

Moreover, the latest “nowcasts” from the Federal Reserve Banks of New York and Atlanta also suggest above-trend growth. Consensus among a panel of sophisticated economists aligns with this view, projecting trend growth for the coming year.

Inflation, a key factor influencing the Fed’s decisions, has markedly improved compared to last year and is approaching, though still slightly above, the Fed’s target. The prevailing belief is that inflation will align with the Fed’s target in the medium term, which is central to their rate-setting criteria. However, it is worth noting that the most recent Core CPI reading came in slightly above expectations, adding a layer of complexity to the inflation outlook.

The Fed’s Likely Path

Given the current economic indicators and inflation dynamics, it seems unlikely to us that the Fed will implement aggressive rate cuts without clear evidence of economic weakness or significant undershooting of inflation targets. The Fed’s cautious approach reflects a balanced view of ongoing economic strength and inflationary pressures.

Conclusion

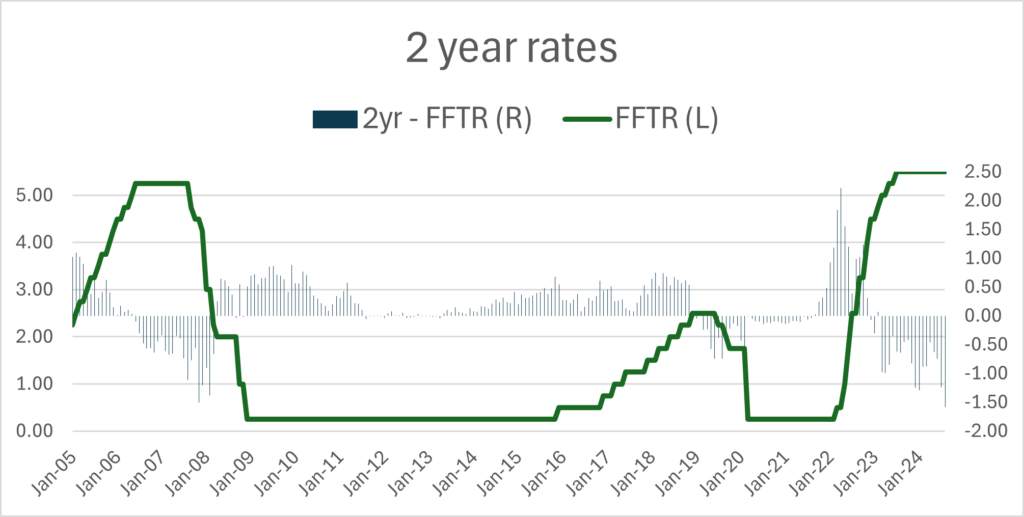

Investors have seen a nearly 125 basis point move lower in 2-year treasury rates in the third quarter (as of the time of this writing), unambiguously reflecting a dramatic change in rate expectations. With this aggressive move, short term rates have moved into a historically wide relationship with the current Fed Funds target rate.

Chart 3

We think the market’s anticipation of substantial Fed easing may be overly optimistic. As the Fed continues to monitor economic and inflationary conditions, we think it is more probable that their approach to rate cuts will remain measured and incremental. This cautious stance might leave some market participants disappointed if they were expecting more aggressive easing measures. As always, staying attuned to economic data and the Fed’s evolving perspectives will be crucial for navigating the remainder of 2024.

DISCLOSURES

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-607127-2024-09-16