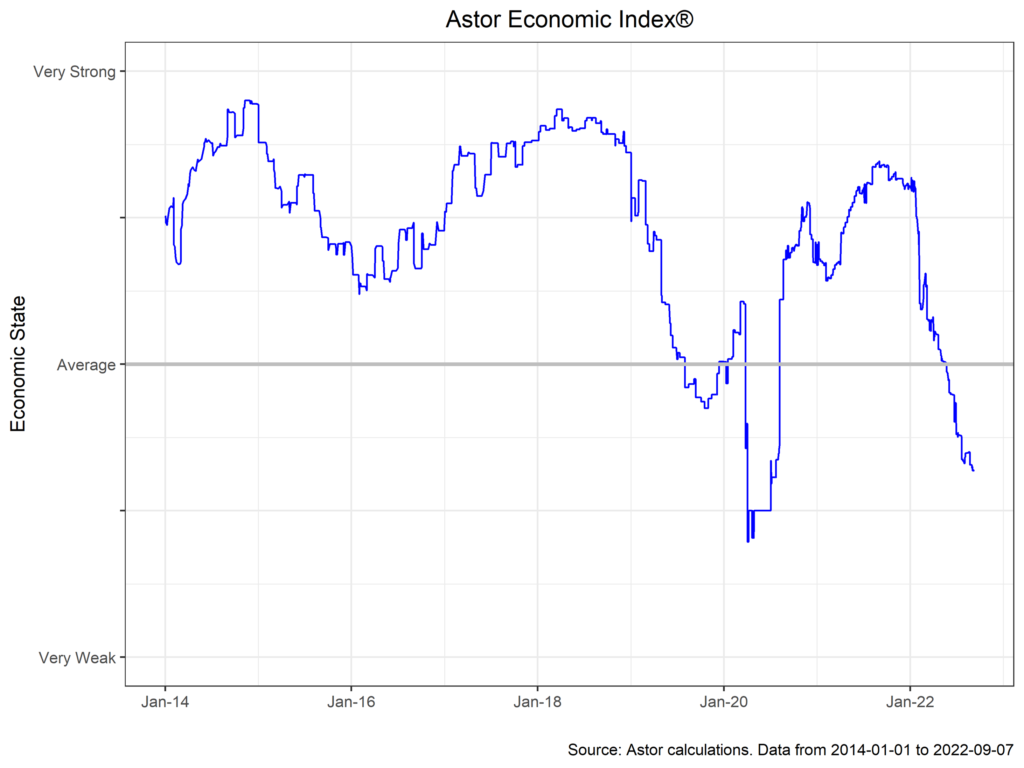

The U.S. economy has proven resilient to firming monetary policy so far this year. The Astor Economic Index® (AEI) is at a level consistent with below-average growth but above outright recession. This is consistent with other nowcasts and forecasts of the U.S. economy: Bloomberg consensus for Q3 GDP growth is at 1.4%, down a tad from 1.5% and in line with the Atlanta Fed’s forecast, which has declined from 2.6%.

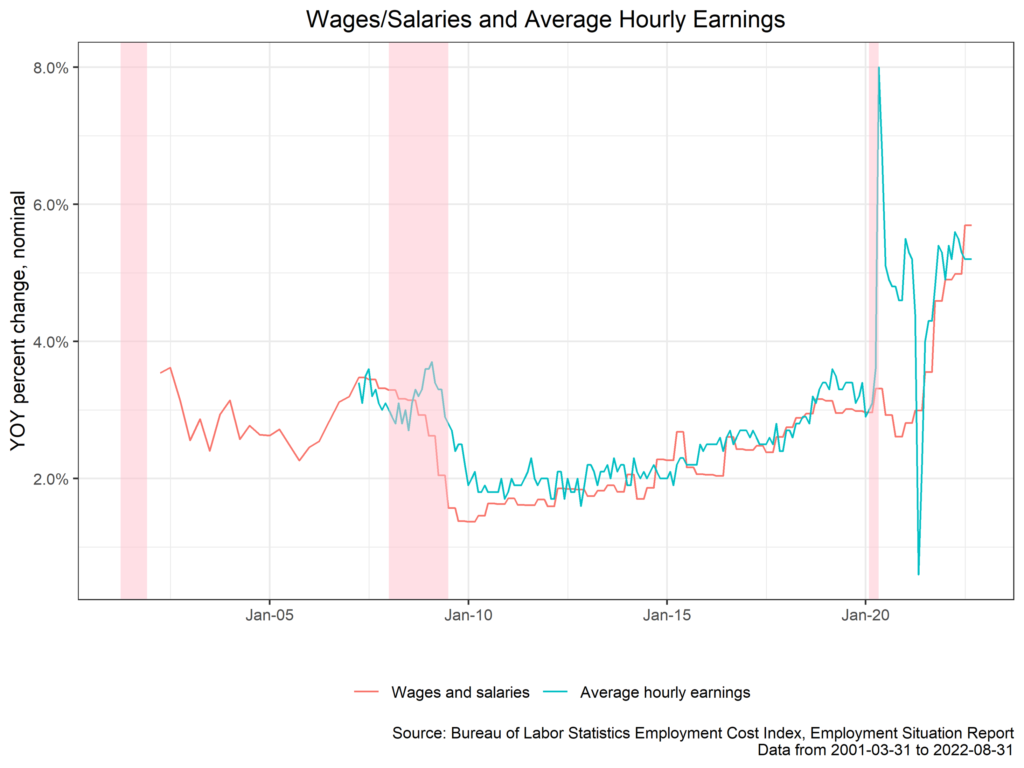

As in months past, the AEI® has been supported by a strong labor market, but this month’s reading bucked a few trends. Nonfarm payrolls gained 315,000 in August, but U3 ticked up to 3.7%. This was something of a perfect reading for the Fed, with labor market gains more muted than July, and the unemployment rate moving up from additional labor force entrants rather than cooling hiring trends: labor force participation improved to 62.4% from 62.1% in the month prior, a long-awaited sign that Americans are moving off the labor market sidelines. Wage growth will need to cool for the Fed to be successful in meeting its policy goals, and a labor market with more participants should help calm earnings. Average hourly earnings were modestly lower than the month prior at 0.3% m/m (5.2% y/y), which the Fed will take as a good sign.

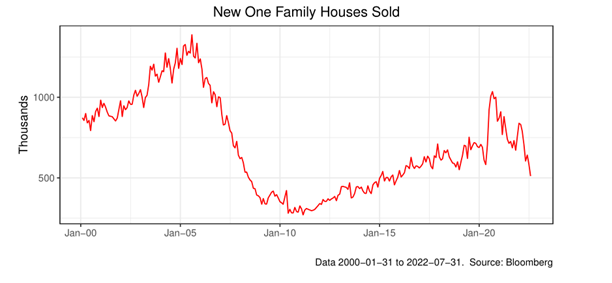

The housing market is thought to be one of the primary channels through which monetary policy impacts the U.S. economy, and that theory seems to be validated over the past few months. Average 30-year mortgage rates reach a peak of 5.89%, the highest level since 2008. In turn, home purchases have slowed considerably since the beginning of the year, with new home sales at 511k (SAAR) in July, down from 831k in January, as mortgage payments erode new homeowner’s buying power. Inventory has also begun to climb in some markets.

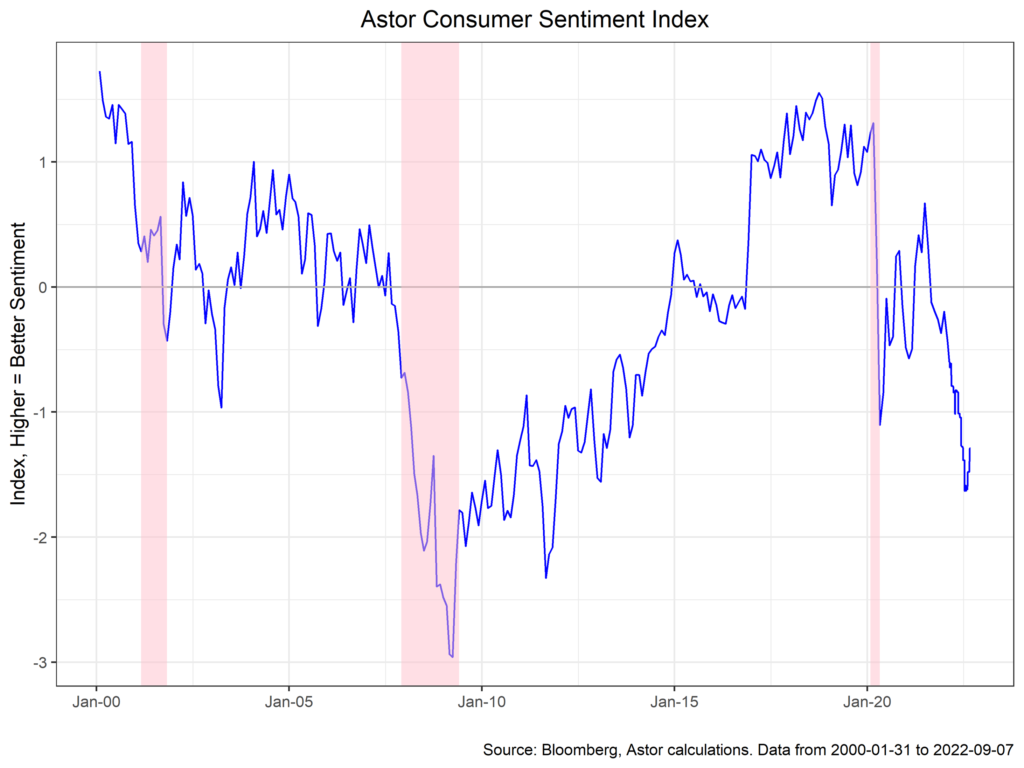

Finally, it is worth mentioning recent trends in consumer sentiment. Consumers have been remarkably pessimistic about the state of the economy lately, a feeling which is at odds with their financial situation and the health of the labor market. The cause has been inflation (read: gasoline prices), and gauges of consumer sentiment have tracked the price at the pump quite closely. It is perhaps unsurprising then that consumer sentiment has improved as gas prices have fallen this month.

Based on improving labor market dynamics and a slowing housing market, the Fed could be forgiven for thinking that monetary policy was having its intended effect and thus opening the door to smaller rate hikes in the future. The Fed, however, has been quite explicit in saying they will not be slowing down anytime soon, with Chairman Powell drawing parallels to the Voeckler era. The Fed will need to see further sustained disinflation in core PCE and CPI (rather than energy prices coming down), as well as slowing hiring and less robust consumer demand before they consider pausing.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and are subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index® (AEI): The AEI is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The AEI is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The AEI is not an investable product and it should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-299809-2022-09-09