Over the past few months, forecasts of an imminent recession have been pushed further and further away. Instead, consensus views vacillate between two scenarios: an economy “stuck” at higher growth and higher interest rates for the time being, and the much-heralded soft landing, with a slowly cooling labor market and inflation coming down over time. The Astor Economic Index®, for its part, has picked up of late, returning to about average growth from the below average range. We delve into some of the evidence for the higher for longer or soft-landing scenarios below.

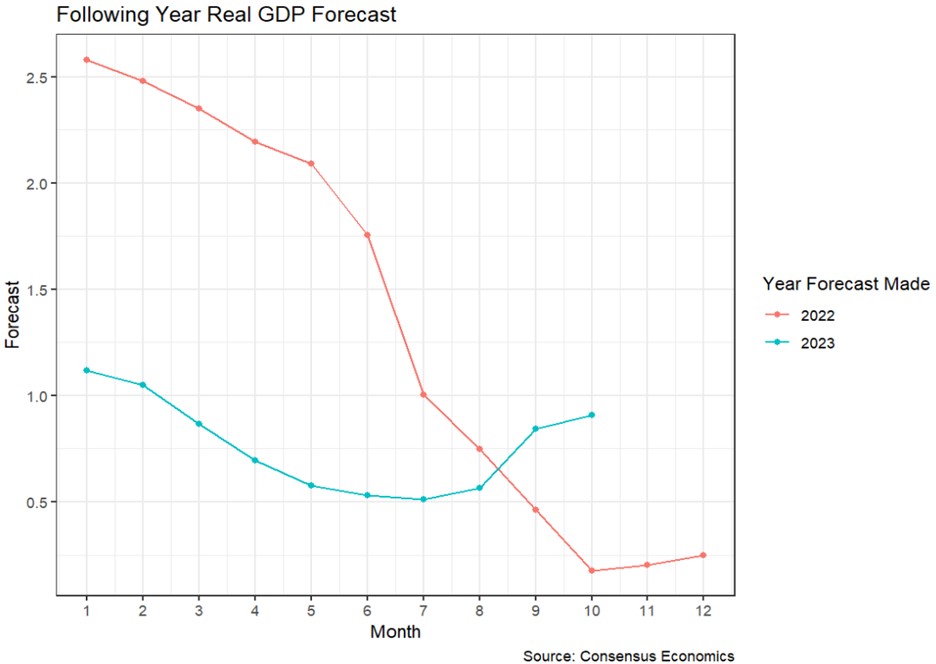

Forecasts for output growth have been (wrongly) pessimistic for some time: recall the consensus forecast in 2022 for 2023 declined precipitously throughout the year – real GDP (q/q SAAR) has remained above 2% this year. Recently, forecasts for 2024 have begun to tick up as the economy proves surprisingly robust. What explains the discrepancy? The impact of rate hikes on the real economy has taken some time to add drag, with the bulk of high yield rollovers due not until 2024/2025. Similarly, the vast majority of mortgages are fixed rate, adding less pressure on households to consume less.

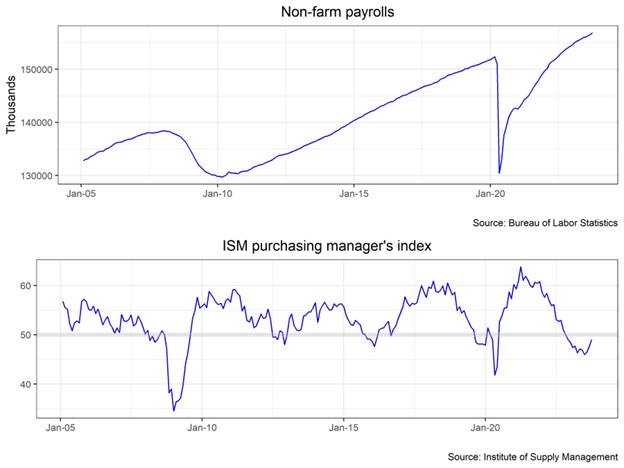

It is often said that the best hedge for inflation is a job, and here too the economy has defied predictions. Non-farm payrolls printed above consensus (Bloomberg median of 170,000) at 336,000, led by gains in hospitality and leisure. Prior months were revised upwards by 119,000 as well. Real wages are a surprisingly thorny series to track, but most estimates suggest that pay has kept pace or exceeded prices, buying the U.S. consumer. Soft landing proponents can point to flat m/m average hours worked and slowing wage gains. Purchasing Manager Indices appear to have bottomed out, with ISM manufacturing ticking back up towards the neutral line (49 in September), blowing past expectations (Bloomberg median survey 47.9). Services cooled somewhat, printing at 53.6, down from 54.5 the month prior but still solidly in expansion territory.

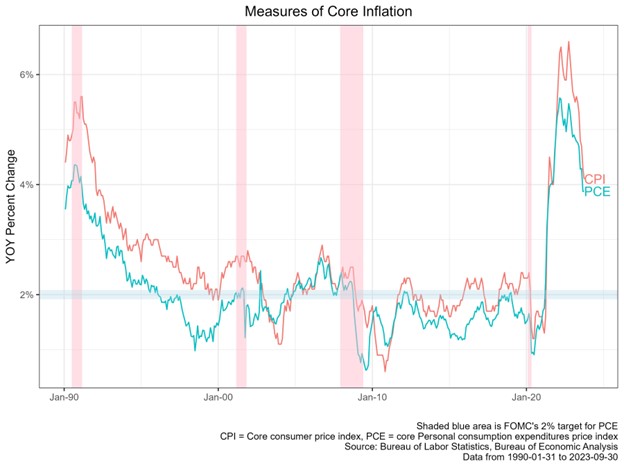

The most recent Consumer Price Index print was a mixed bag, but ultimately points to inflation running cooler but still too high. Headline CPI was up 3.7% y/y, with core up more at 4.1% y/y. Housing continues to make up the bulk of the index, with owners’ equivalent rent up 0.6% m/m. Other service sector prices increased as well. Encouraging, goods prices ticked down (-0.4% y/y) as used car prices came off the boil. The UMich survey for 1 year ahead inflation was also hot, with the survey median of 3.8% the highest in several months.

In sum, we see an economy resistant to the Fed’s best efforts to bring down inflation. The Fed’s dot plot shows the FOMC believe the Fed Funds rate will be above 5% in 2024. Interestingly, the rates market has finally started to sing the Fed’s tune: recall that at the beginning of September, markets were pricing ~50bps of cuts by July 2024. The 10 year treasury has sold off as economic reality hits home, reaching as high as 4.8% in October. As a result, financial conditions have finally started to tighten, and it will be important to see if this in turn flows through to the real economy.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-439003-2023-10-13