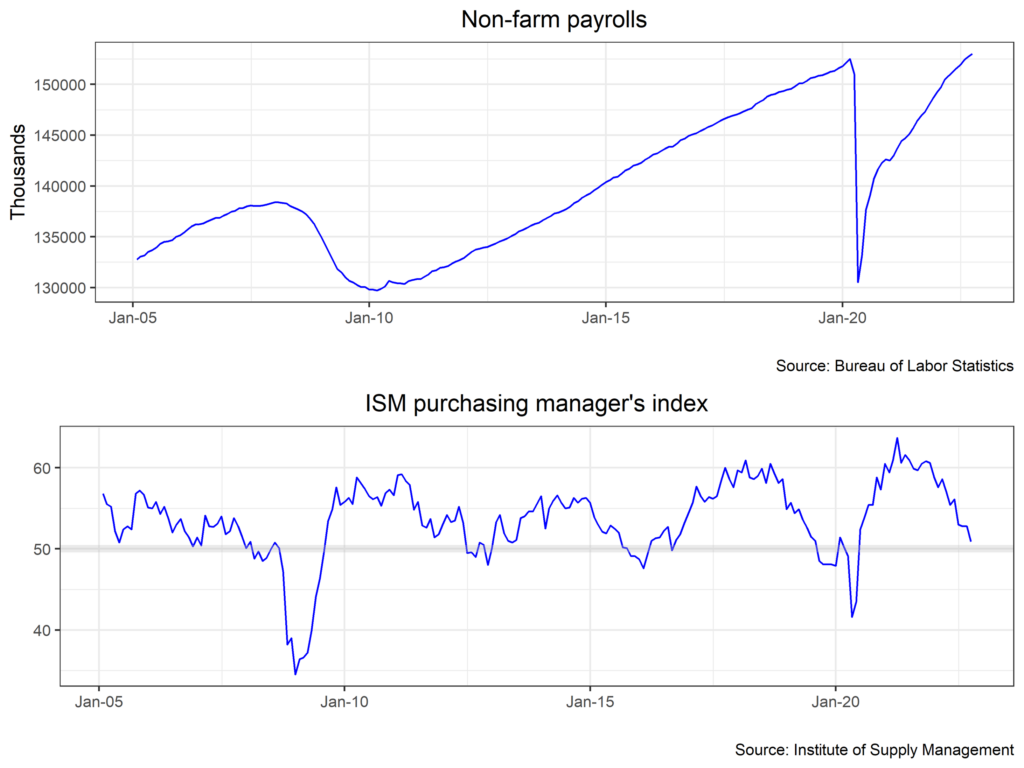

September brought little in the way of relief for those looking for a Fed pivot, and the Astor Economic Index® remained constrained at a below-average reading. As in recent months, the U.S. labor market is somewhat at odds with the global economy and other domestic data prints, with job gains elevated despite softening purchasing manager indices. We dive into the details below.

The ideal resolution to the U.S. inflation story is a “soft landing”: weaker consumer demand, lower savings, constrained margins, and softer wage growth without the economy experiencing an outright recession. None of these are achievable without a looser labor market; indeed, the Federal Reserve has pointed to job openings per person as a crucial metric to show that the Fed is making progress toward economic equilibrium. August’s non-farm payroll print provided little comfort that the labor market is working in the Fed’s favor, with 263,000 new jobs added (above consensus) and the unemployment rate dropping to 3.5% as more people left the labor force. Ideally, the Fed would like to see softer prints (perhaps in the neighborhood of 100k), slow nominal wage growth, and higher participation rates to right-size the balance in labor supply and demand.

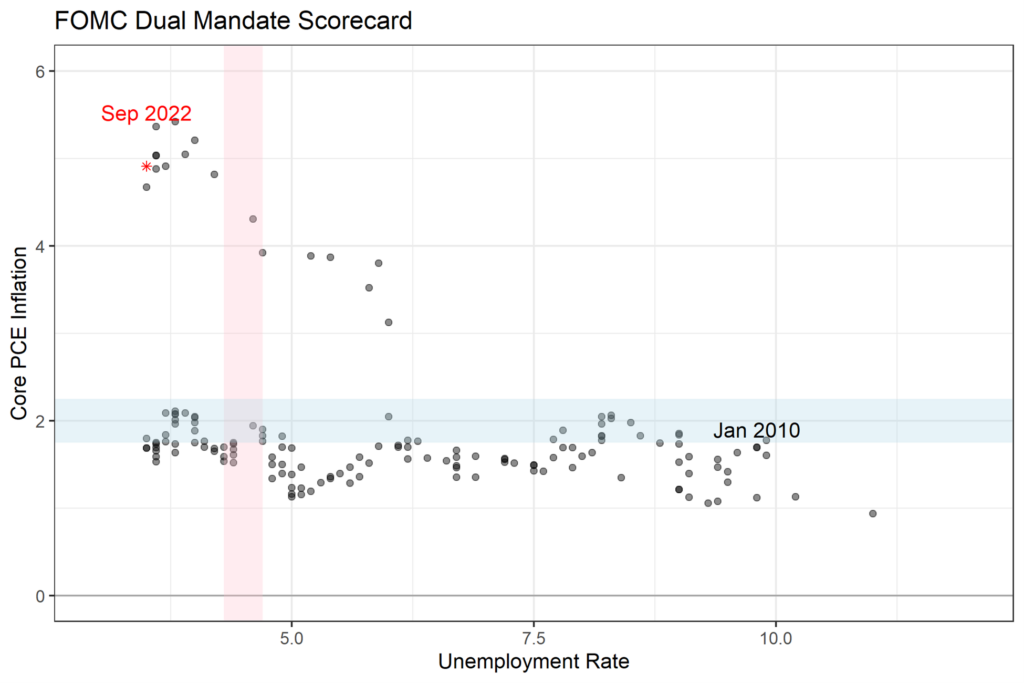

September’s Consumer Price Index (CPI) was well over consensus, with core CPI of 6.6% (6.5% survey) y/y, or 0.4% (0.2% survey) m/m. It is increasingly difficult (and foolish) to explain away hot CPI prints by looking around corners or isolating key factors. In recent months, economic pundits alternated between a series of hopeful narratives: the housing component in CPI is badly lagged and will come down sharply in months to come, or that we should look past energy prices, or that transportation costs should drop quickly. All of these are probably true, but they do not excuse “sticky” (i.e. components of inflation likely to persist) CPI above 6%, even when excluding housing. In sum, expect persistently higher than target CPI for some time to come.

As a result, we believe it is likely the Fed will continue down a path of aggressive hikes, including a 75 bps hike at the next meeting in November. 75bps also seems likely in December, and the terminal Fed Funds rate of 4.5% previously discussed in months past now seems like a lower bound, with markets predicting 5% in early 2023. All in all, the economy has proven resilient to policy thus far (with the large caveat that monetary policy works with a large lag), but financial markets have started to creak, and it seems more possible today than in months past that the Fed will be hiking into (and possibly though) a recession in 2023 or 2024 as inflation remains resilient.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and are subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index® (AEI): The AEI is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The AEI is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The AEI is not an investable product and it should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-311519-2022-10-19