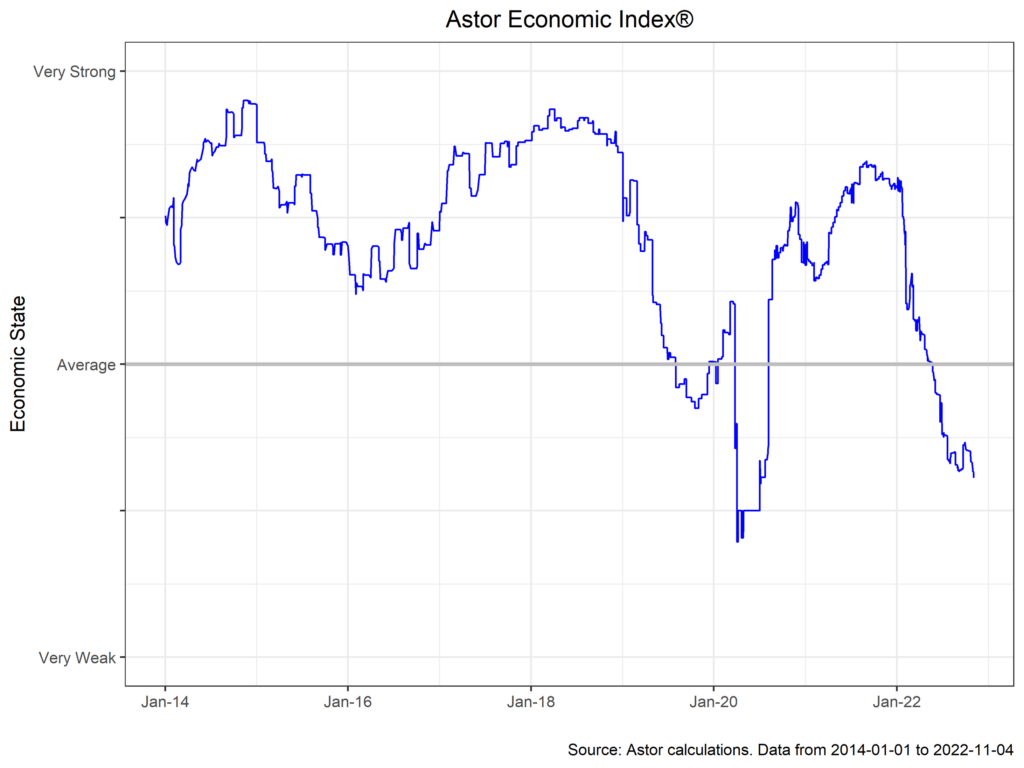

The Astor Economic Index®, our nowcast of the U.S. economy, is essentially unchanged from the prior month at a level consistent with below-average economic output. Nonetheless, the intervening period has had several significant data prints, which we discuss below. In sum, recent trends suggest that the window to a soft(er) landing is now more open than it has been in the past, but risks are still weighted to the downside.

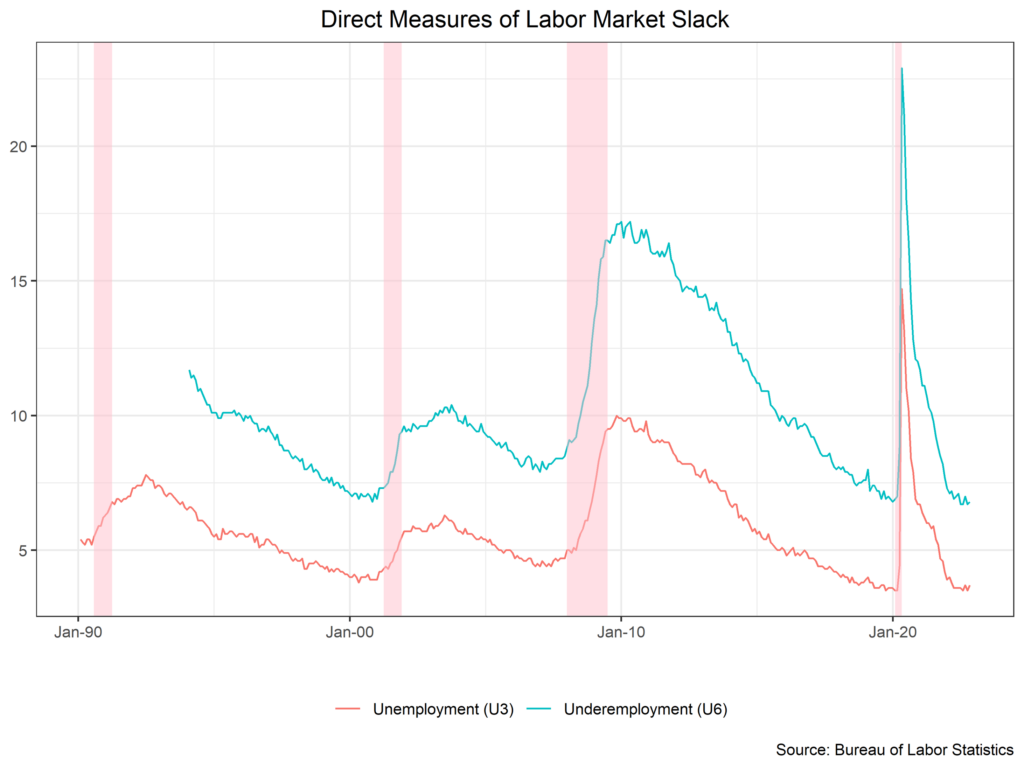

As usual, we begin with the labor market. Recall that the Federal Reserve would like to see significant cooling in hiring and job openings as a sign that it is making progress in lowering inflation, as a looser labor market should (further) lower real wage gains and thus aggregate demand. The latest nonfarm payroll report had a bit of good news and bad news for the Fed. The headline print of 261k was above estimates, and prior months were revised up, suggesting that the Fed still has some ways to go to bring hiring down – Bloomberg Economics estimates that monthly declines of 35k are necessary for inflation to return to 2%. Average hourly earnings were also hot at 0.4% m/m (4.7% y/y). On the other hand, the household survey has continued to diverge from NFP prints, with the unemployment rate rising to 3.7%, and layoffs (particularly in the tech sector) seem to be gaining traction.

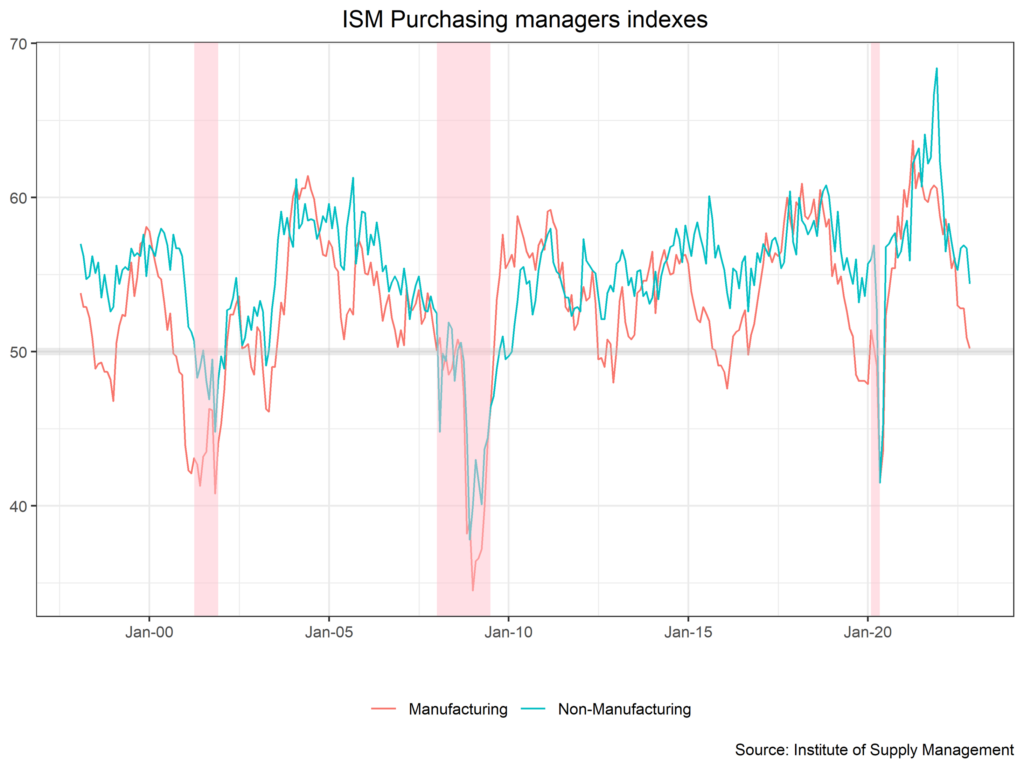

Purchasing manager indices are also worth noting. Both ISM services and manufacturing have softened considerably (see chart below) in the past six months, with manufacturing barely above 50 (the level consistent with neither growth nor contraction). Prices paid declined along with a backlog of orders. New orders and exports dropped for services, with noted weakness in real estate. S&P PMIs, which measure the same thing as the ISM in a slightly different manner, are already well into contraction territory.

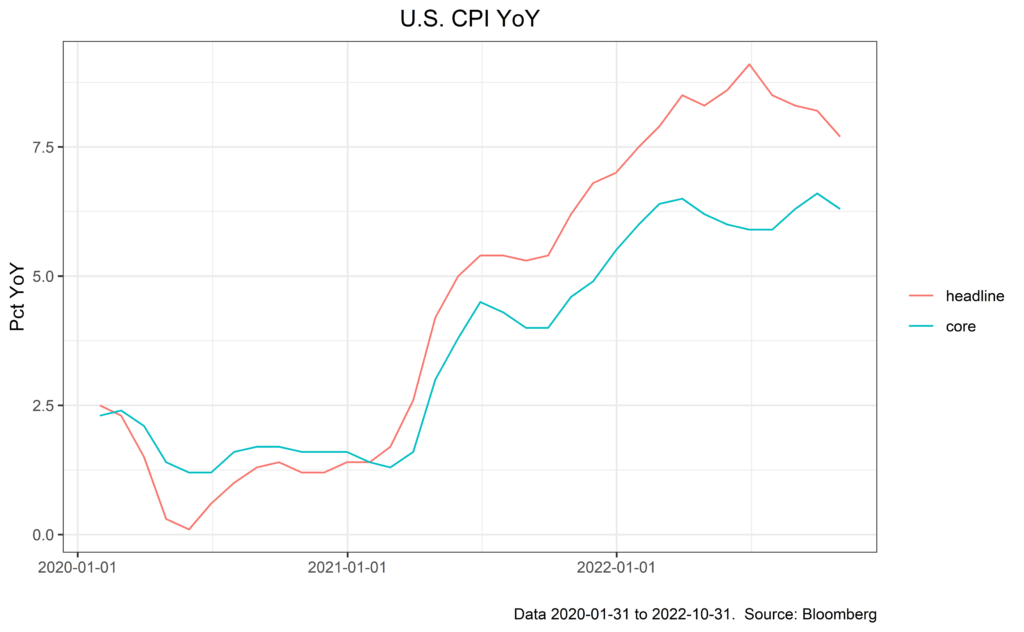

Astute readers will notice that this blog now comes later in the month, to better coincide with the month’s Consumer Price Index release. As far as the U.S. economy is concerned, as goes inflation, so goes domestic macroeconomic prospects. Higher inflation means that the Fed will be forced to tighten financial conditions quicker and to a higher level, and probably crush economic growth along the way.

The October CPI report provided much-needed relief to financial markets, with headline up 0.4% m/m (7.7% y/y) and core up 0.3% m/m (6.3% y/y), well below consensus estimates. The drivers were further disinflation in goods across household items, apparel, and used cars. Services also came in a bit softer from airfares. Trimmed mean CPI, which hints at the breadth of inflation, has moderated to 0.4%.

Recent price action (the Nasdaq was up 7.3% on Nov 10th) might be a bit misjudged, in our view. A large driver was the period adjustment of health insurance costs (based on retained earnings), which dropped 4% m/m and will not be repeated in future months. Housing, meanwhile, remains hot (0.8% m/m), although subject to a large lag. The report does give space to the Fed for slower rate hikes in the future, with 50bps penciled into the December meeting. However, CPI and labor market data are unlikely to have shifted the Fed’s view on the terminal rate, which the market adjusted 20bps lower after the CPI print. The U.S. economy has proven robust, and cooler inflation print does not make a trend. We will need to see several more inflation misses before we (and the Fed) can confidently say inflation has peaked.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and are subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index® (AEI): The AEI is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The AEI is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The AEI is not an investable product and it should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-321350-2022-11-15