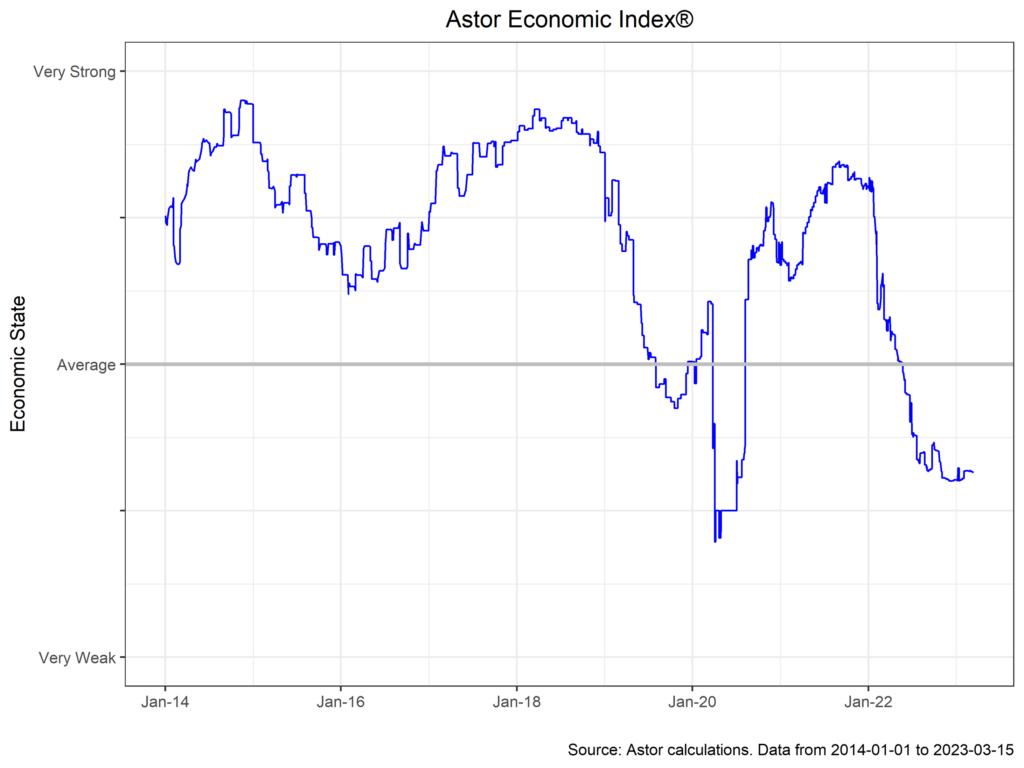

Harold Wilson, the former Prime Minister of the United Kingdom, said (probably apocryphally) that “a week is a long time in politics”. In economics, a day can prove to be a lifetime, as recent events have shown. Banking sector stress over the past week has led to a dramatic repricing across the fixed-income world, and a stunning change in market expectations for Fed policy. The Astor Economic Index®, for its part, remains at a level consistent with weak economic fundamentals. We discuss recent labor market and price data briefly below, as well as the implications of financial stress for Fed policy moving forward.

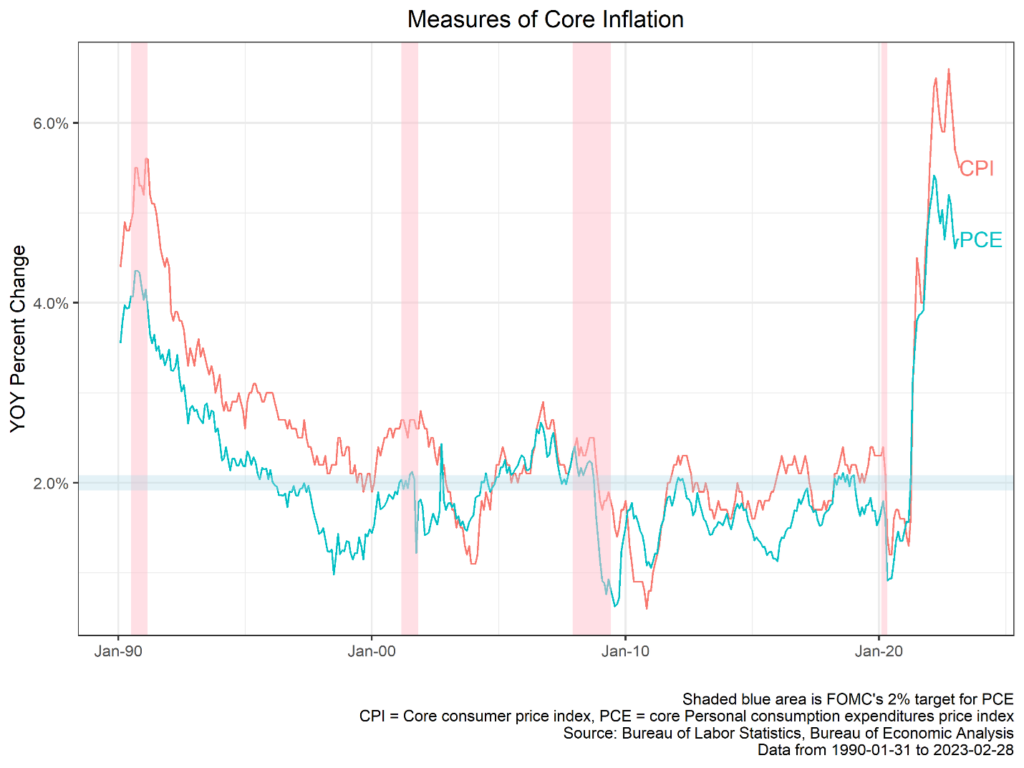

Both non-farm payrolls and the Consumer Price Index point to further inflation. Non-farm payrolls for the month of February were above expectations at 311,000 m/m, with further gains in average hourly earnings. A slowdown in construction hiring has been expected for some time (monetary policy is thought to impact housing first), but job gains in that sector were solid. Core CPI, meanwhile, came in a bit higher than expected at 0.5% m/m, led by housing, which is having an outsized impact on inflation. If private rent measures are to be believed, we may see a reversal of that trend in the coming months (despite differences in new vs continuing rental agreements). Nonetheless, core services excluding housing, the measure that Chair Powell watches closely, was up 0.5% m/m as well, pointing to broad inflation trends across the economy.

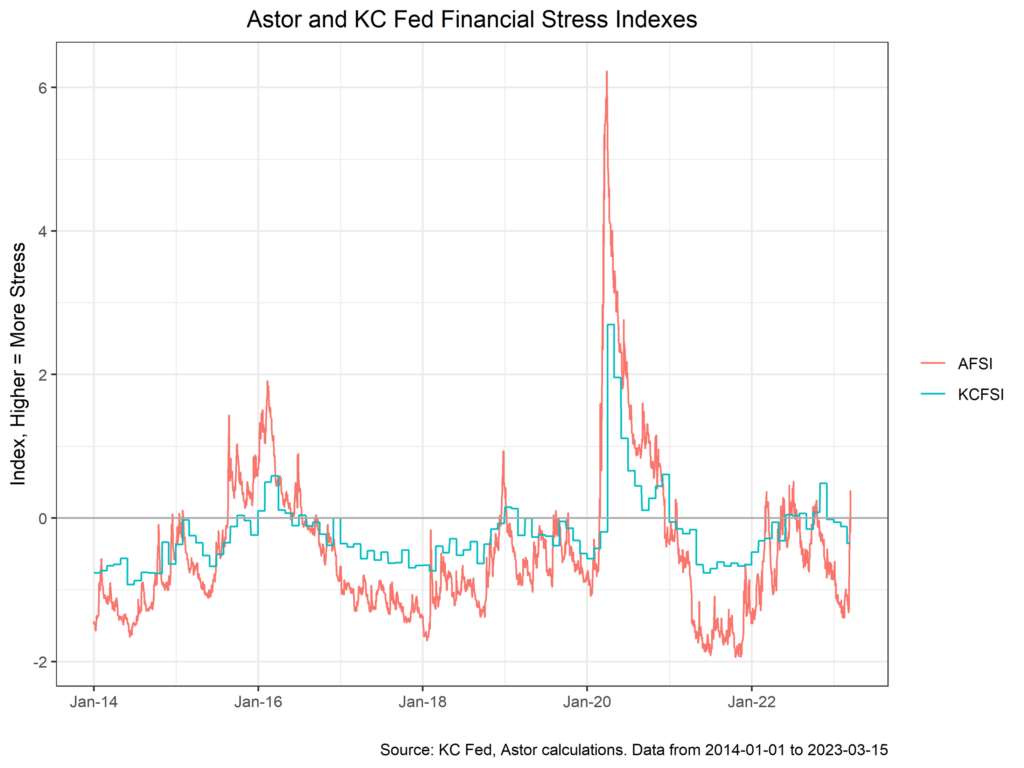

“The Fed is going to hike until something breaks” has been a common refrain in financial circles for the past year, and something has indeed broken, with the shuttering of two banks in the U.S. Price action has been deleterious for other mid-size regional banks, and investors have begun to look further afield, with high yield spreads and CDS prices rising. The Astor Financial Stress Index, our composite view of trends in financial markets, has jumped quite noticeably from two weeks prior.

In sum, we are left with a creaking financial system and robust measures of the real economy. As a result, financial stability and monetary policy are at a bit of a standoff here: tighter monetary policy is probably necessary to bring inflation down to target, as the data mentioned above show, but higher rates will likely prompt more banking system stress. To state the obvious, inducing a recession from a financial crisis is not the intended mechanism of transmission from monetary policy that the Fed has in mind, nor is it the type of economic landing they wish to achieve.

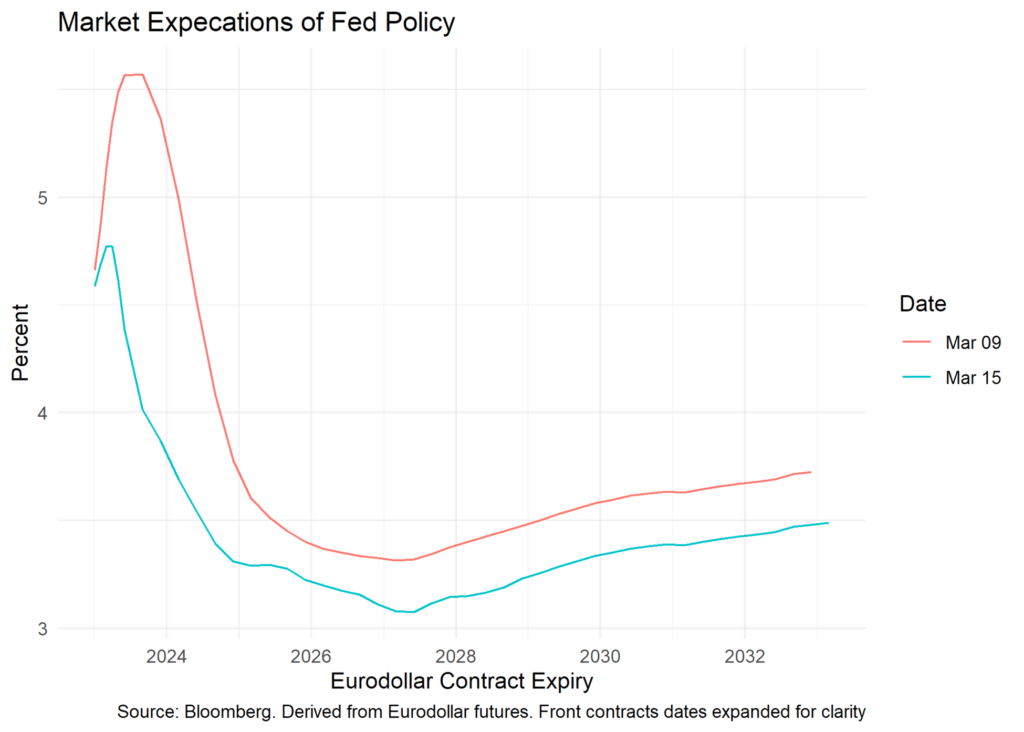

The Fed would ideally like to manage the financial stability portion of policy with other tools (like the recently announced Bank Term Funding Program), freeing up monetary policy to do what needs to be done in the real economy. However, should contagion rear its ugly head, the Fed will have no choice but to revise down its intended policy path. Another concern is the supply of credit to the economy, as banks tightening down the hatches could easily spill over into economic growth. The market, for its part, has made up its mind: the chart below depicts the stunning repricing of Eurodollar futures from last week to this writing.

The March meeting of the FOMC will be crucial to better understanding how the Fed intends to balance these contradictory goals. A 25bp hike would indicate the Fed feels confident about the financial system weathering more hikes or is perhaps more worried more about the stickiness of inflation than any further stability concerns. In aggregate, the labor market and the economy look to be chugging along, but new risks mean that that assessment could change very quickly. We will be watching the Fed, financial markets, the banking sector, and inflation very closely over the next month.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-361324-2023-03-16