With the ebbing of the global pandemic, one may have hoped February would mark the beginning of business as usual and a return to focusing on supply chains and other macroeconomic fundamentals. Unfortunately, the war in Ukraine has added another exogenous shock to the system. We’ll delve into the U.S. economic situation below, and touch on possible impacts to the U.S. from the conflict as well.

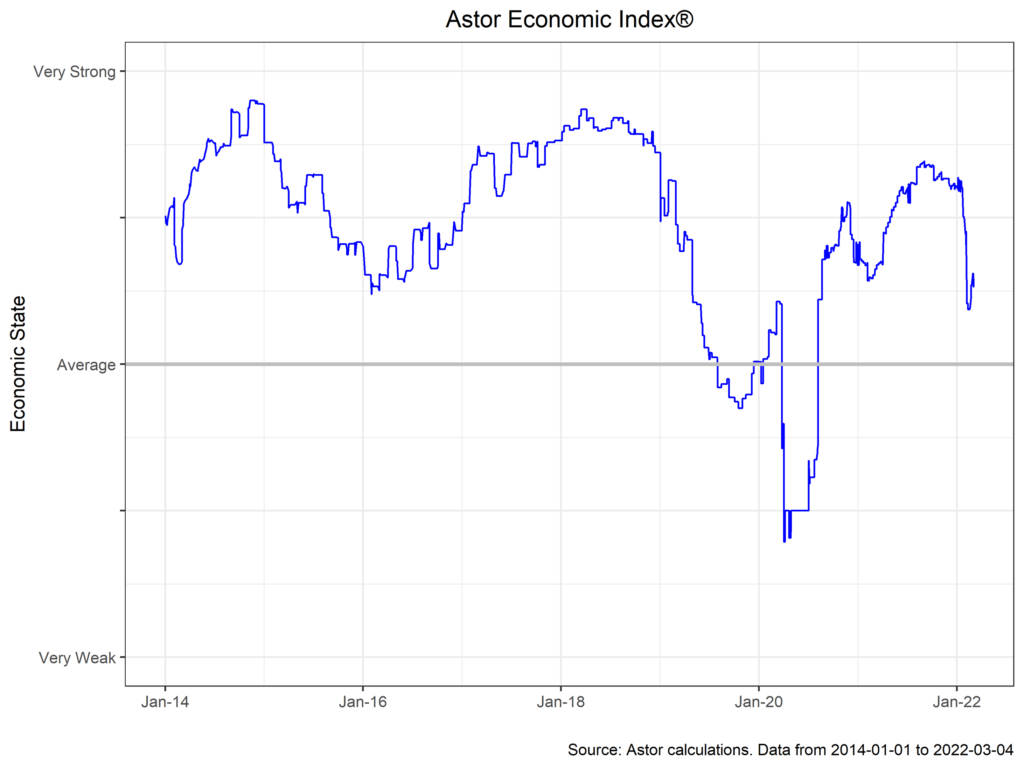

The Astor Economic Index, our nowcast of the U.S. economy, is slightly lower than it ended in January, continuing a trend towards returning to potential output. In sum, the domestic situation in the U.S. is still quite strong, with robust domestic demand and hiring. Data coming off pandemic era highs is likely to be salubrious to the extent it indicates normalization of consumption habits and lessens pressures on supply chains and thus inflation. Q1 growth estimates from the private and public sectors range from 0.5% to 2% – a healthy result, considering the backdrop.

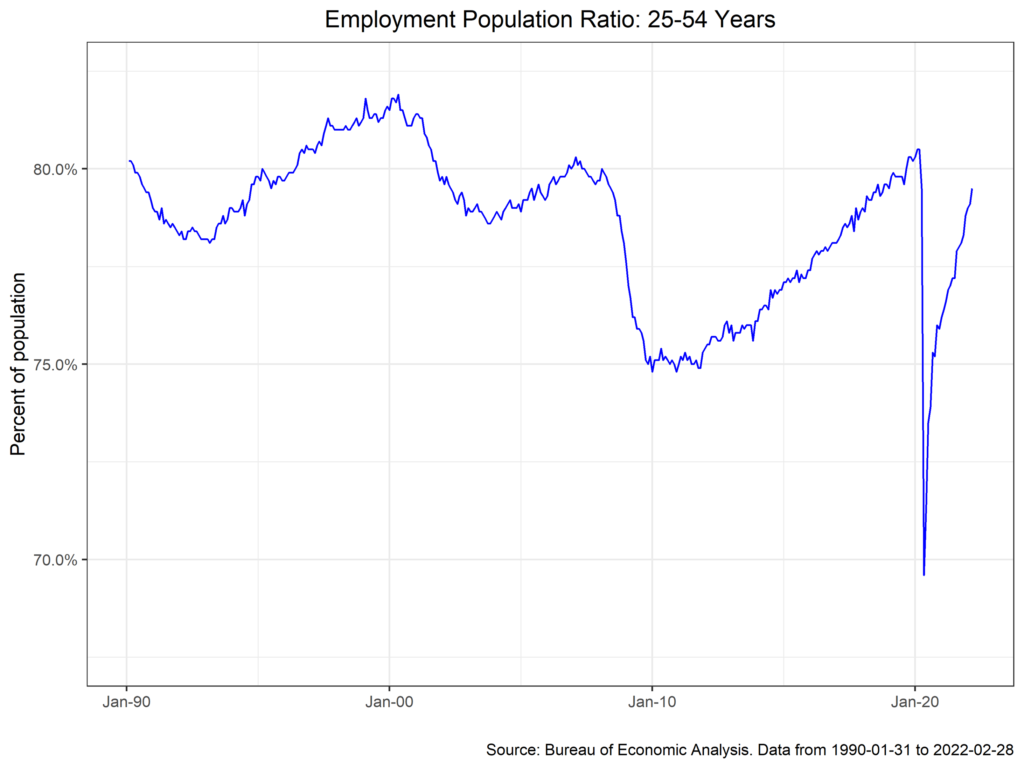

The labor market is a continued source of strength in the U.S., with non-farm payrolls printing at a strong 678,000 m/m, along with some strong revisions, and beating Bloomberg survey estimates of 423,000. Labor participation has also improved as concerns around the pandemic fade, bringing workers back off the sidelines.

U3 unemployment is now estimated at 3.8%, its lowest level since the pandemic began, and provides substantial evidence to the Fed that the labor market is nearing the Fed’s estimate of full employment. On the other hand, real wage growth, which is somewhat subject to interpretation, has remained solidly negative, allaying fears of wage price spiral.

The war in Ukraine introduces new complexity in assessing the external environment for the United States. Russia is a small part of the world economy, contributing about 3% to global output. It is, however, an outsized player in the supply of commodities, purchases of which are likely to be directly curtailed by Western sanctions. This feeds into concerns around inflation, particularly in the energy sector, with the front WTI future contract spiking above $100 a barrel. Nonetheless, the direct impact to the U.S. economy is likely to be modest and mostly felt through higher inflation, barring any further escalation.

Of course, this comes at an inopportune time for the Fed, which is already balancing the risk of sustained inflation against faster rate hikes. So far, the crisis has not fundamentally changed the Fed’s reaction function, beyond introducing a new downside risk to output and upside risk to inflation. We will be watching the Fed’s meeting on March 16th very closely to better understand how they view the path forward and keeping our eye closely on price pressures and supply chains.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

AIM-3/10/22-BP551