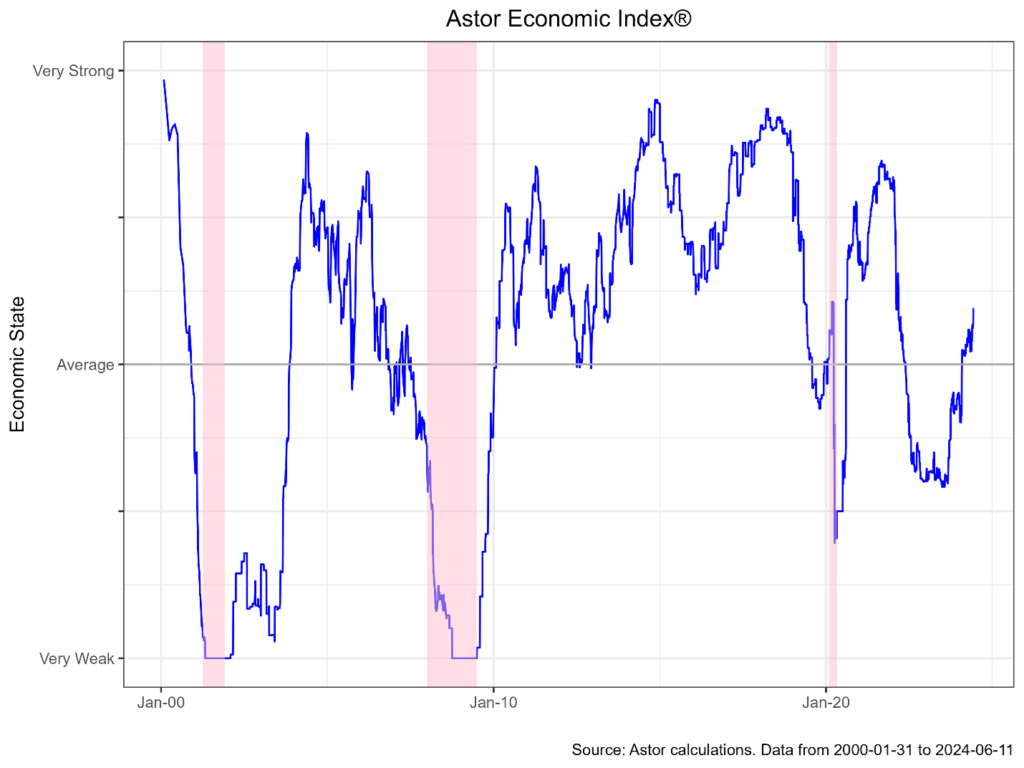

From our perspective, recent data has brought the near-term macro trajectory into clearer focus. For some time, the distribution of potential outcomes for inflation and growth was wide: it was unclear whether price pressures (and output) would moderate significantly over the next year. Although uncertainties do remain, it seems likelier today than in months past that the worst of inflation is finally under control, and that growth has reached a steadier state. The Astor Economic Index® ticked up into the above average range.

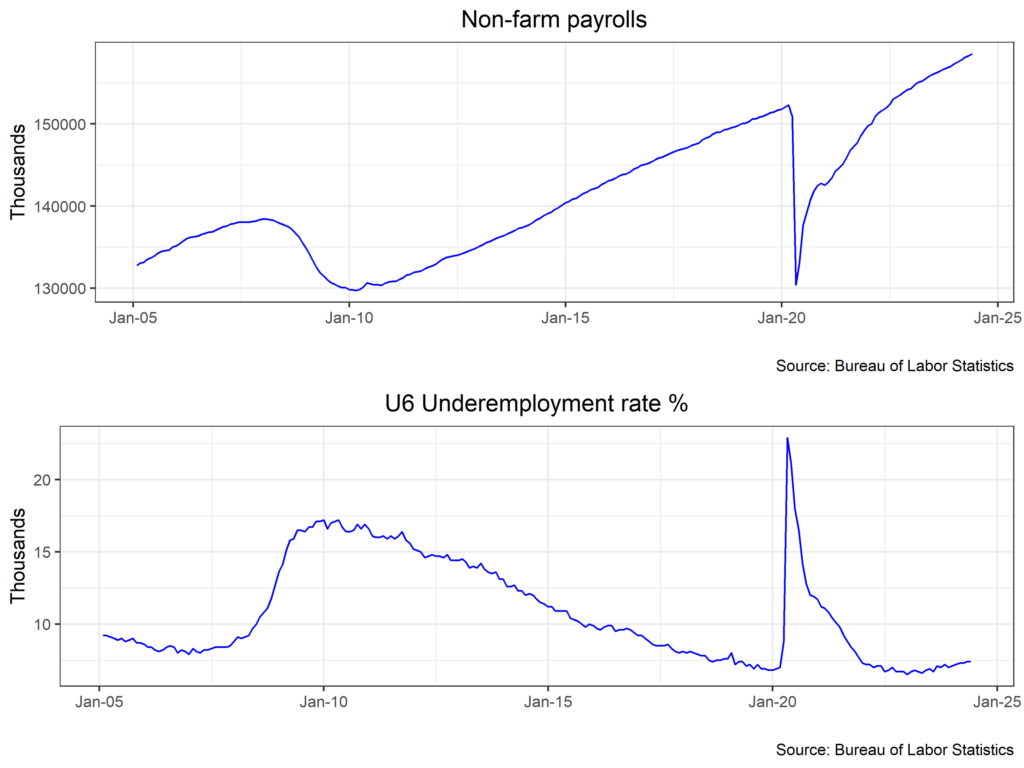

Employment, and concordantly income driven consumption, remain the pillar of the domestic economic expansion. Non-farm payrolls were up 272,000 in May, a barn burner of a report compared to expectations for 180,000. As a result, we added REITs to our Dynamic Allocation strategy and cut from our shorter duration fixed income holdings. Note that other measures of employment are roughly at their historical averages, with job quits and openings falling, and U6 unemployment ticking up to 7.4% (the same as the month prior). We think the economy is in a solid place, but one can certainly find data that points to softening.

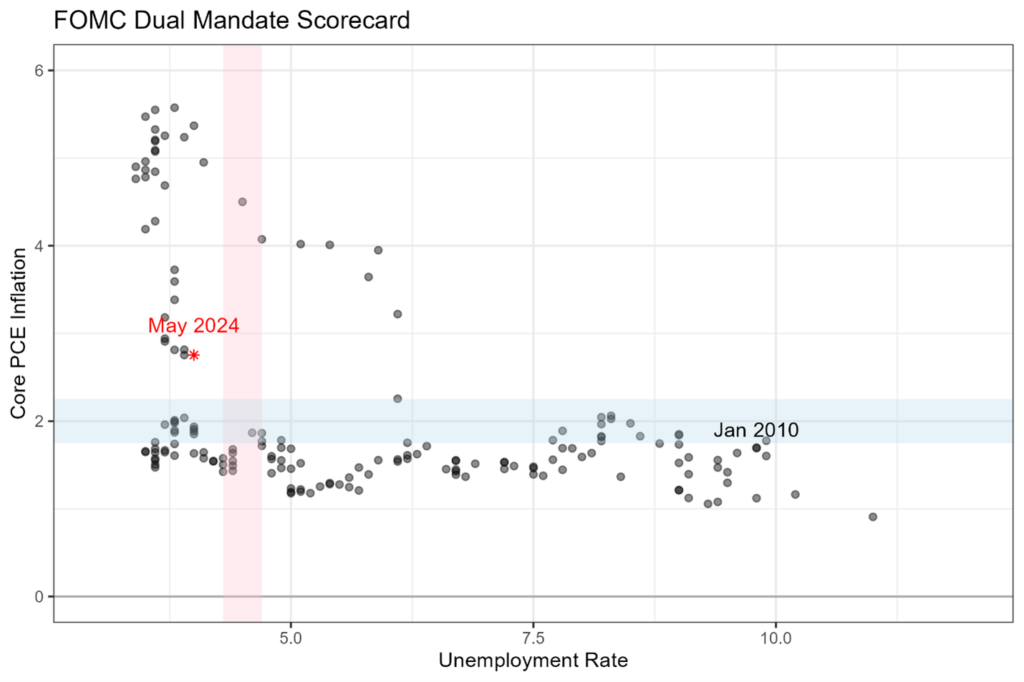

We’ve continued to lengthen the duration of our Active Income portfolio as we feel more solid ground under our feet for the trajectory of rates. High yield valuations are quite stretched, with the spread on the Bloomberg High Yield Index a meager 3.1% over Treasuries. As a result, we trimmed our senior loan position and added longer duration Treasuries. Recent data has validated our thinking – headline CPI printed 0.0% m/m and core was up 3.4% y/y, both below expectations. Make no mistake – inflation will follow a volatile path downwards (shelter, in particular, has proven stubborn), but the trend should remain towards cooling overall. The Fed now reckons that 25bps of cuts will be appropriate in 2024, with four more cuts following in 2025. Markets, as of this writing, see about 40bps of cuts (1 1/2ish moves) this year, as derived from fed funds futures. Regardless of whether the FOMC or markets are right, both are finally dancing to the same tune, which we have been preaching for some time – a gradual return to a normal economy.

DISCLOSURES

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

Astor’s strategies seek to achieve their objectives by investing in Exchange-Traded Funds (“ETFs”). An ETF is a type of Investment Company which attempts to achieve a return similar to a set benchmark or index. ETFs are subject to substantially the same risks as those associated with the direct ownership of the securities comprising the index on which the ETF is based. The value of an ETF is dependent on the value of the underlying assets held. ETFS typically incur fees that are separate from those fees charged by Astor. ETFs are subject to investment advisory and other expenses which results in a layering of fees for clients. As a result, your cost of investing in Astor’s strategies will be higher than the cost of investing directly in ETFs and may be higher than other investments with similar objectives. ETFs may trade for less than their net asset value. Although ETFs are exchange traded, a lack of demand can prevent daily pricing and liquidity from being available. Investors should carefully consider the investment objectives, risks, charges, and expenses of the ETFs held within Astor’s strategies before investing. This information can be found in an ETF’s prospectus.

The mentioned strategies are offered in various formats. Clients invested in the strategies can have different results depending on the specific investment program and product type chosen.

MAS-M-562091-2024-06-18