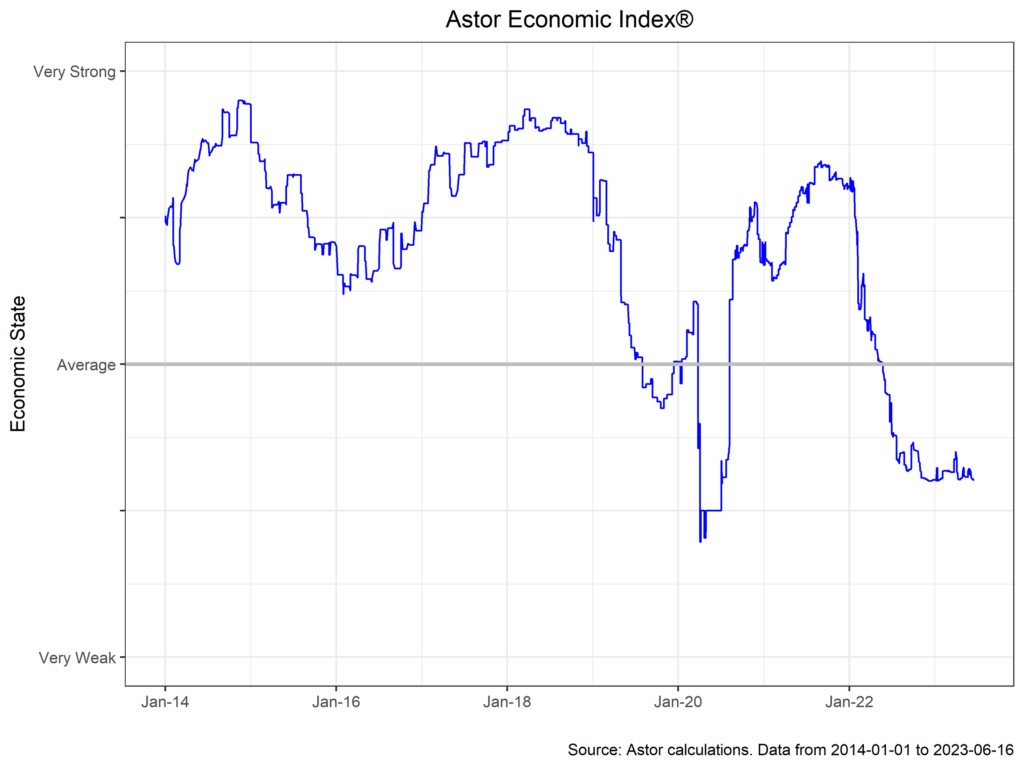

The U.S. economy has continued its normalization over the past month, with key measures of output and labor moving towards the pre-pandemic trend. For the pessimistic, there are plenty of cracks in the data to support a narrative of underlying weakness, but the overall picture is one of robust demand and gradual cooling. The The Astor Economic Index® is in broad agreement with this notion, sitting at a level consistent with average to below average domestic growth. Inflation, meanwhile, continues to slow, but at a speed at odds with the Federal Reserve’s reaction function. We discuss the labor market, inflation, and the recent Fed meeting below.

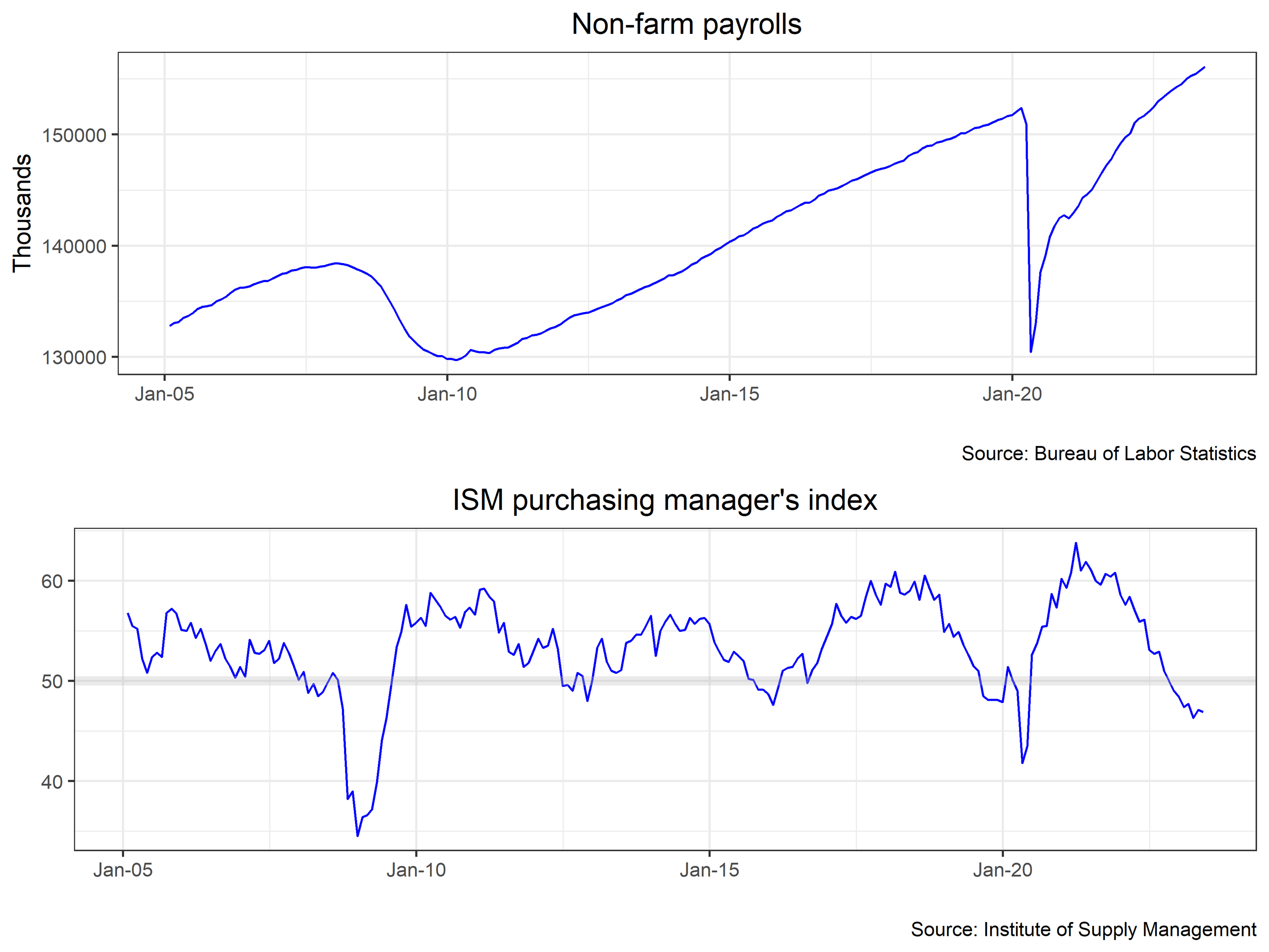

The labor market remains the key to understanding the trajectory of the U.S. economy. Robust employment supports consumer demand (in addition to the rundown on personal savings), which in turn props up prices in goods and (particularly) services. Non-farm payrolls surprised once again to the upside in May, printing at 335,000 (expected 195,000), with prior months revised upwards by 90,000 – a strong print, no matter how you cut it.

Nonetheless, it is fair to say that labor signals are a bit more balanced now than in the past. Jobless claims, which measure applications for unemployment benefits, have ticked up modestly, with initial claims at 262,000 and continuing claims at 1.7m. Overall, however, claims are lower than the historical average, suggesting the recent pickup is more of a return to business as normal rather than an imminent recession.

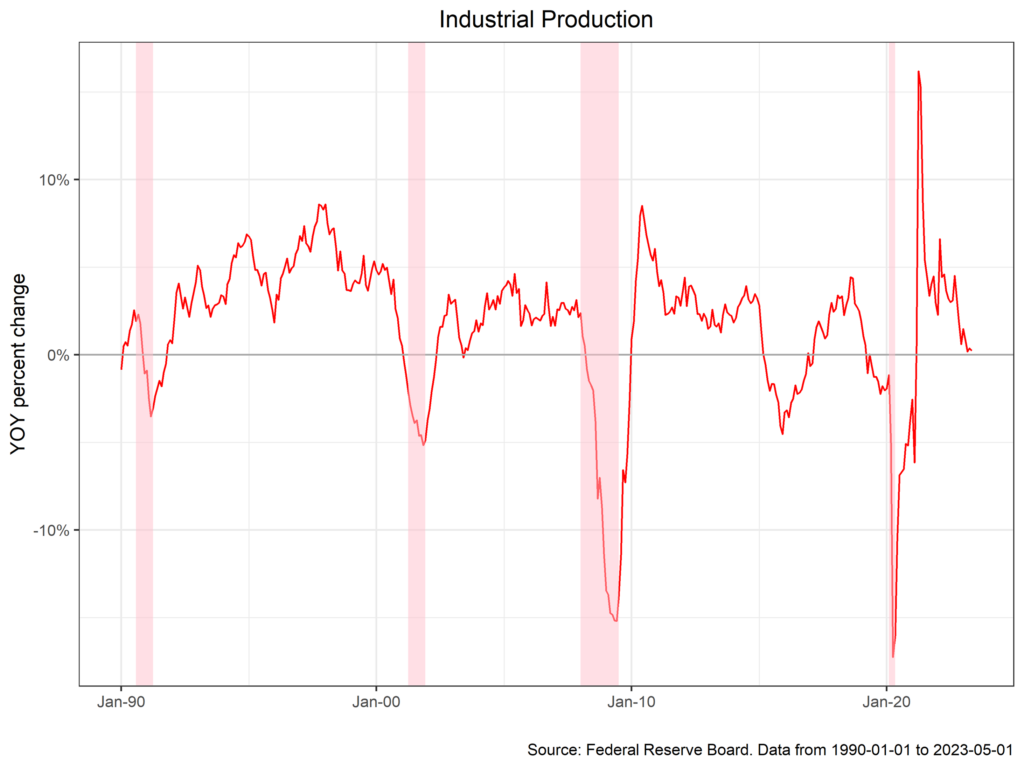

Other (especially survey based) data is mixed. Industrial production, for example, has moderated substantially (-0.16 % y/y in May), a rate that has typically preceded recessions, and retail sales have also softened. Manufacturing PMIs (in the chart above) remain solidly in contraction territory, driven by weak new orders, and service sector PMIs have declined as well.

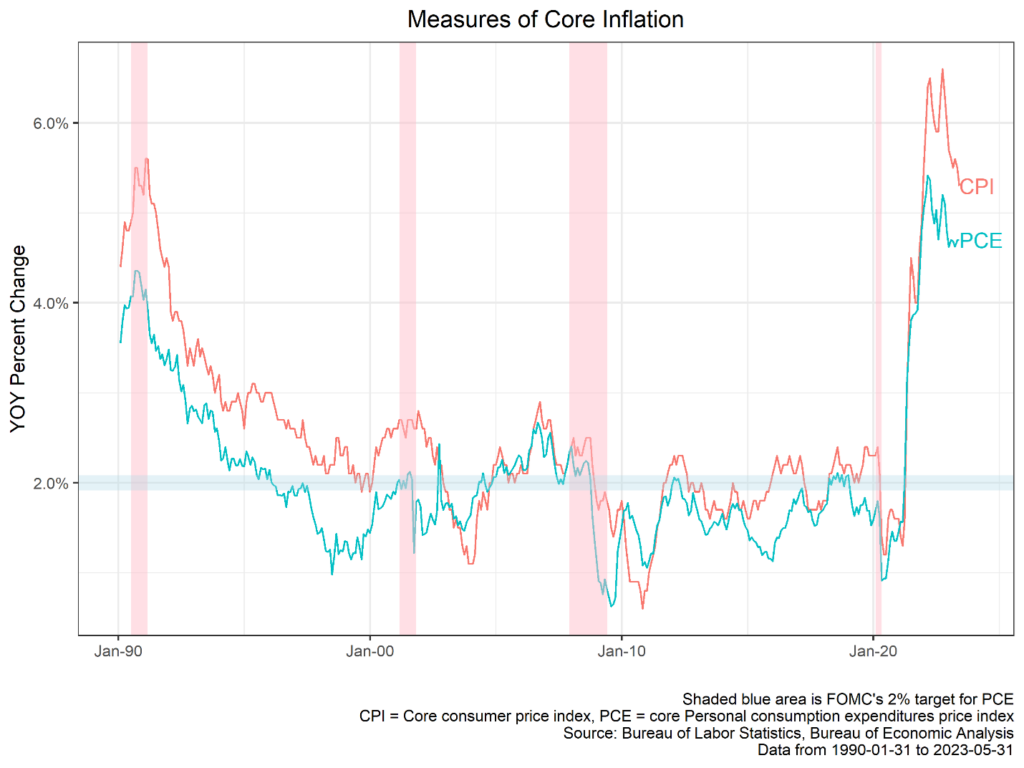

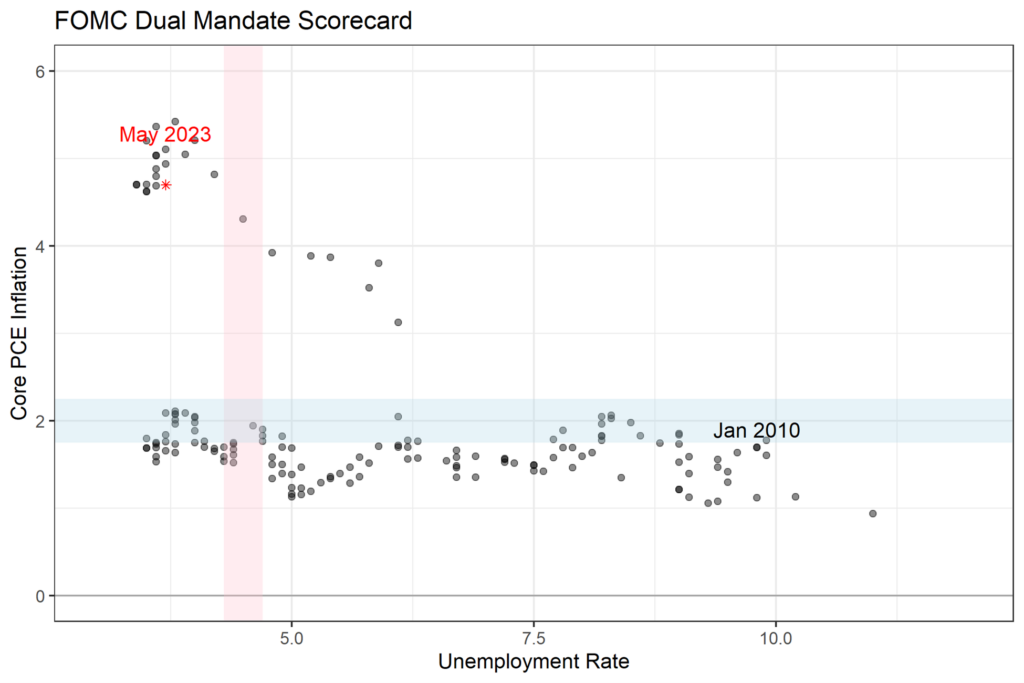

Inflation data remain the ultimate exercise in motivated reasoning. Core CPI for May came in close to expectations at 5.3% y/y (0.4% m/m SA), with headline CPI at 4.0% y/y on the back of declining energy prices. Doves can credibly point to a sustained decline in inflation over the past six months, and the distribution of inflation is now narrower than in the past. Moreover, and as we’ve noted previously, inflation is now driven by services rather than the hot demand for goods seen in the pandemic. Within services, shelter contributed 0.24pp to the monthly core reading, a trend that is unlikely to continue if private rent measures are anything to go by. Expectations are well anchored, with the University of Michigan 1 year median inflation reading dropping to 3.3%.

On balance, however, inflation is looking problematically persistent. Core CPI has hovered around 5% over the past three months, and looking past broader housing trends, services inflation is unlikely to moderate until consumer balance sheets normalize, given the outsize impact that demand is currently producing. Estimates of PCE after adjusting for real time shelter costs are also much higher than the Fed’s target.

The Federal Reserve is more sympathetic to the later view. Despite pausing rate hikes for the first time in over a year at the June FOMC meeting, FOMC participants revised up their median expected terminal rate for 2023 by 50bps to 5.625. It is probably worthwhile to take the Fed at its word: inflation is too hot, shows no signs of cooling durably, and the labor market remains supportive. Market participants are skeptical: Fed Fund futures are pricing a substantially lower terminal rate and rate cuts towards year end and into 2024. Between the wish and the thing, the world lies waiting.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-395276-2023-06-20