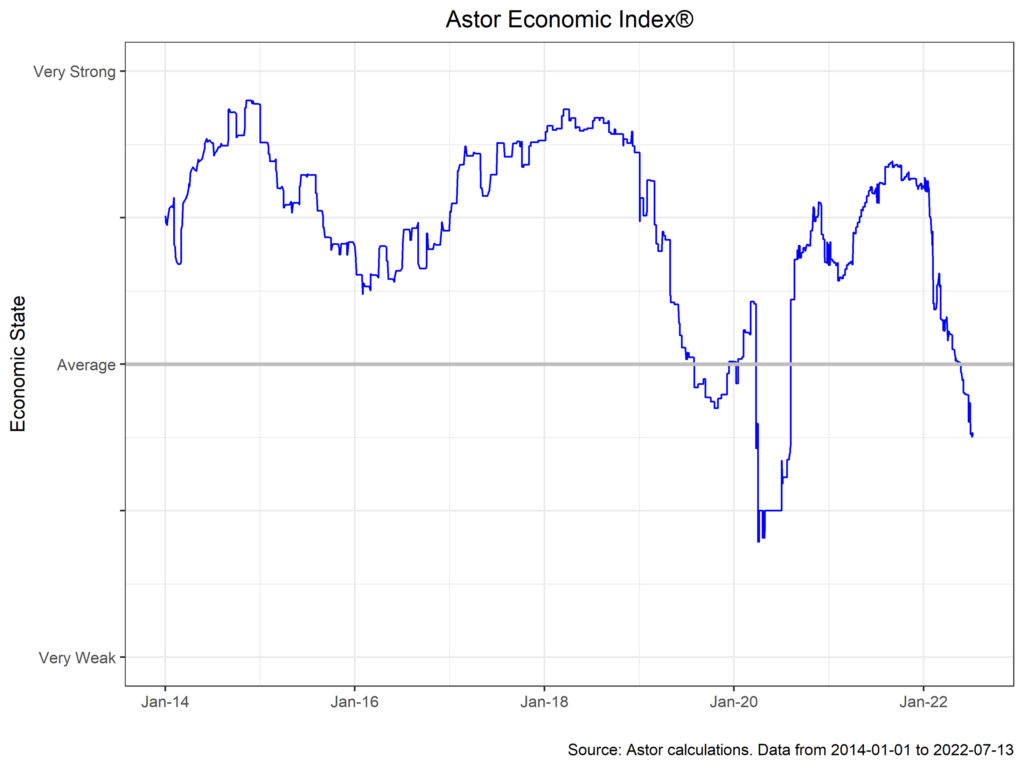

The U.S. economy is at an interesting crossroad: the labor market is showing continued strength despite weakening output, burgeoning inflation, and an increasingly hawkish Fed. The Astor Economic Index has taken the side of the naysayers, posting consecutive declines for the last 11 months. The index now lies somewhere in the below-average to weak range. This comports with other nowcasts of the macro picture, with the Atlanta Fed nowcast for Q2 GDP growth at -1.2% q/q.

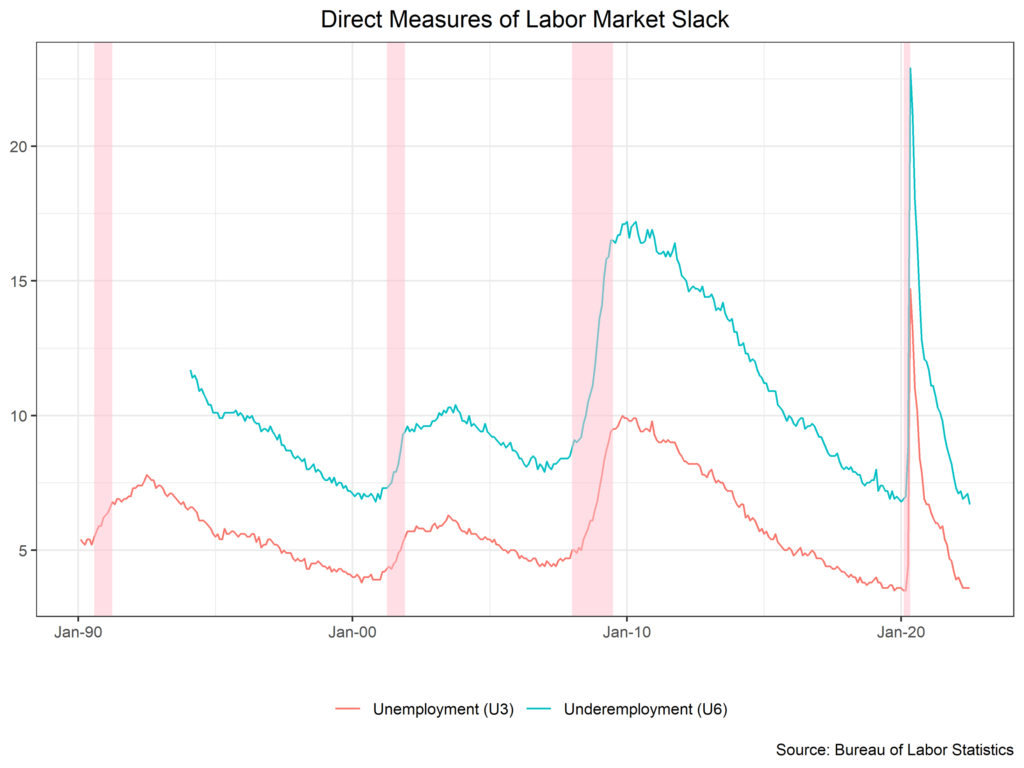

This is despite strong growth in non-farm payrolls, which posted an above consensus 372,000 gain m/m, with U3 unemployment steady at 3.6%. U6 unemployment, which includes those holding part time jobs declined to 6.7% from 7.1% in the month prior. The labor market has thus far proven robust to rising rates and dwindling business confidence. Non-farm payrolls, however, are just one indicator of labor market health. Inflation tends to erode take-home pay, and indeed, real average hourly earnings declined 3.6% y/y, a forty year low. Jobless claims, a famously noisy series, have also begun to tick up, with the most recent initial claims reading of 244,000 a yearly high. Nonetheless, by all appearances, the labor market remains very tight.

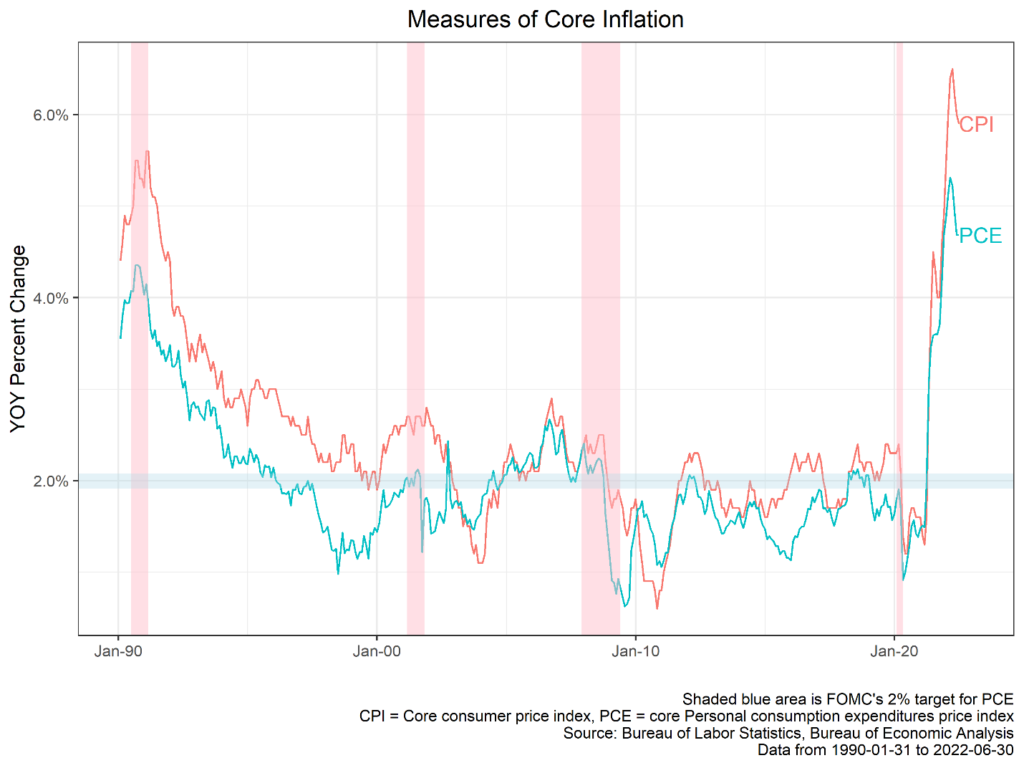

A healthy labor market likely gives the Fed fuller confidence in an aggressive hiking cycle, and the FOMC will certainly need to stick to their guns given the most recent Consumer Price Index reading of 9.1% y/y (core 5.9%), the highest reading since 1981. A few items are worth mentioning beyond the headline numbers. First, inflation was broad-based. Energy, of course, was the single largest contributor, but many other sectors saw increases: restaurants meals, for example, were up 10% y/y. Second, shelter costs, which tend to be sticky, were up 5.6% y/y, which could cause inflation to be durably above target in the medium term. Finally, it’s worth noting that commodity prices, including oil, have cooled substantially since the reference date for the most recent CPI print. The driver is not so much supply and demand fundamentals, but rather expectations for an impending global slowdown.

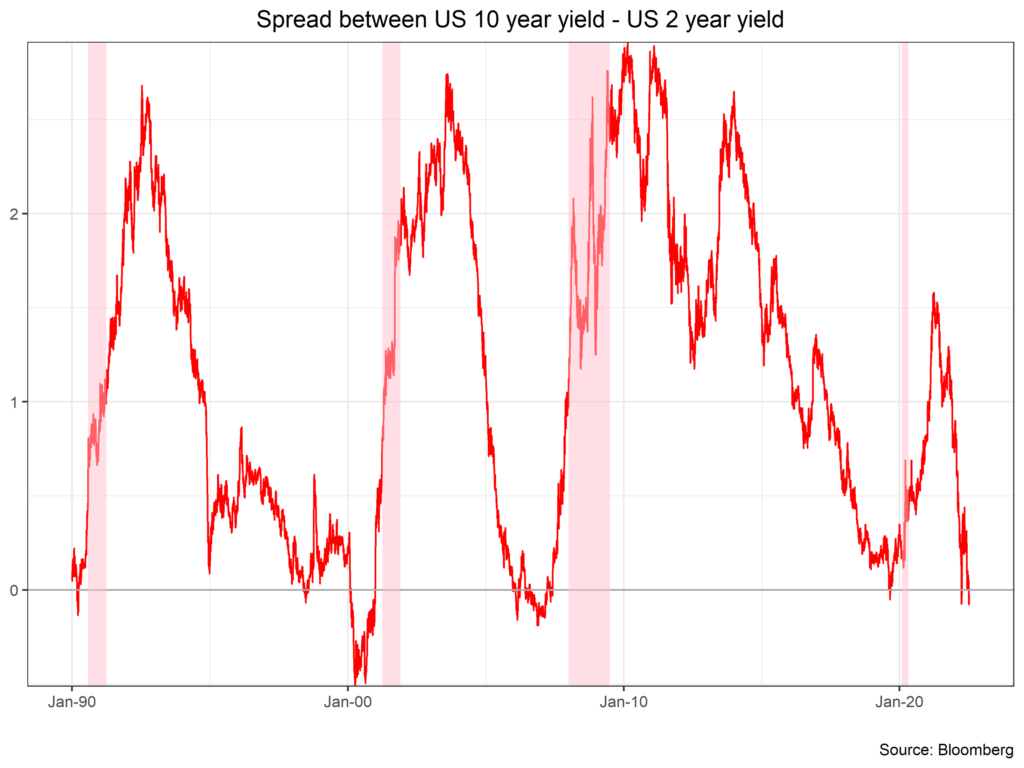

The Fed is likely to speed up the pace of rate hikes in response, with the average market participant (via the Fed Funds futures market) expecting somewhere between a 75bp and 100bp hike next meeting. Ultimately, the Fed seems increasingly comfortable with solving a supply side issue with demand destruction. The market seems to take the FOMC at its word, with two year rates exceeding ten year rates.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-285548-2022-07-15