As usual, we’ll be looking at recent economic data this month, but we’ll also expand on some of the themes we’ve seen this year and look ahead to our base case for 2022. It’s worth noting that our portfolio decisions are made by the current state of the U.S. economy, rather than any forecast, but the end of the year provides an opportunity to take stock of where we’ve been, and where we might be headed.

In sum, we boldly expect growth and inflation to moderate throughout 2022 towards trend.

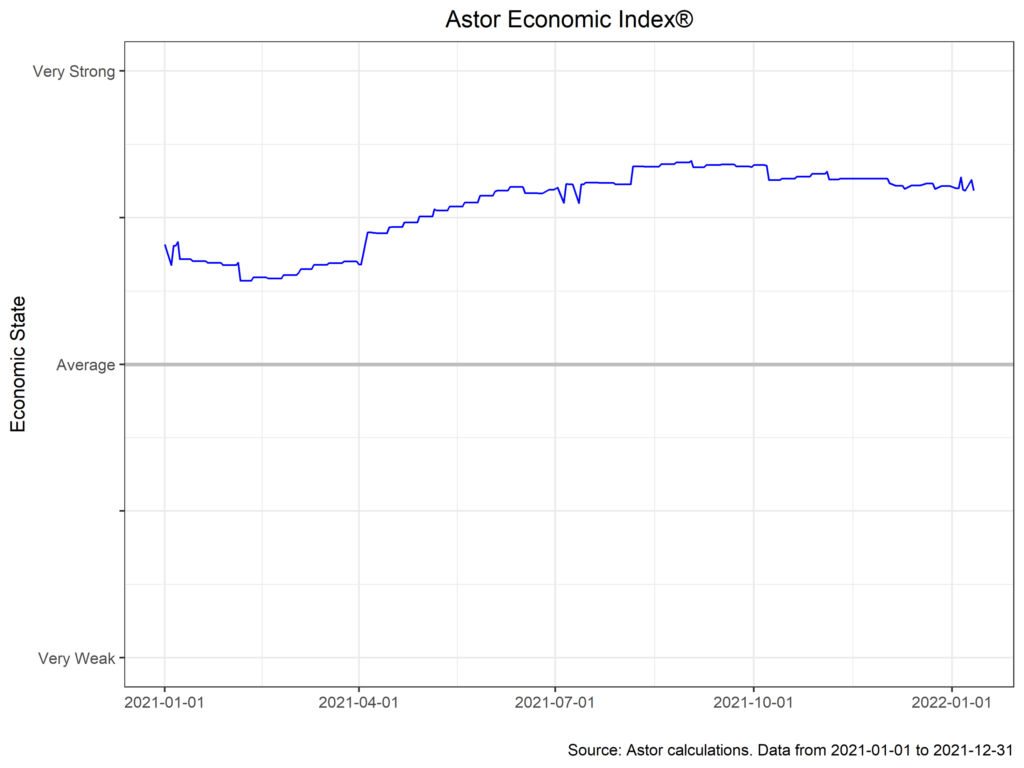

Let’s begin with the obvious: economic growth has been strong and above trend in 2021, and the month of December was no different. Our nowcast of the U.S. economy, the Astor Economic Index® (AEI), was essentially unchanged last month and remained at a level consistent with very strong economic growth. It does not make for a very exciting chart, but it is a positive one.

The AEI picked up steam as 2021 progressed, driven by robust consumer demand, strong fiscal and monetary support, and of course some degree of normalization following the depths of the pandemic. If the theme of 2020 was the COVID-19 pandemic, then 2021’s was a consumer bonanza, with consumption patterns skewed towards goods and away from the historical preference for services. We see the most likely scenario for the economy in 2021 as moderating but strong growth on the back of continued demand and the rightsizing of pandemic era trends. Risks, however, are weighted to the downside for this outlook, based on the interplay between labor market trends, inflation, and Federal Reserve policy.

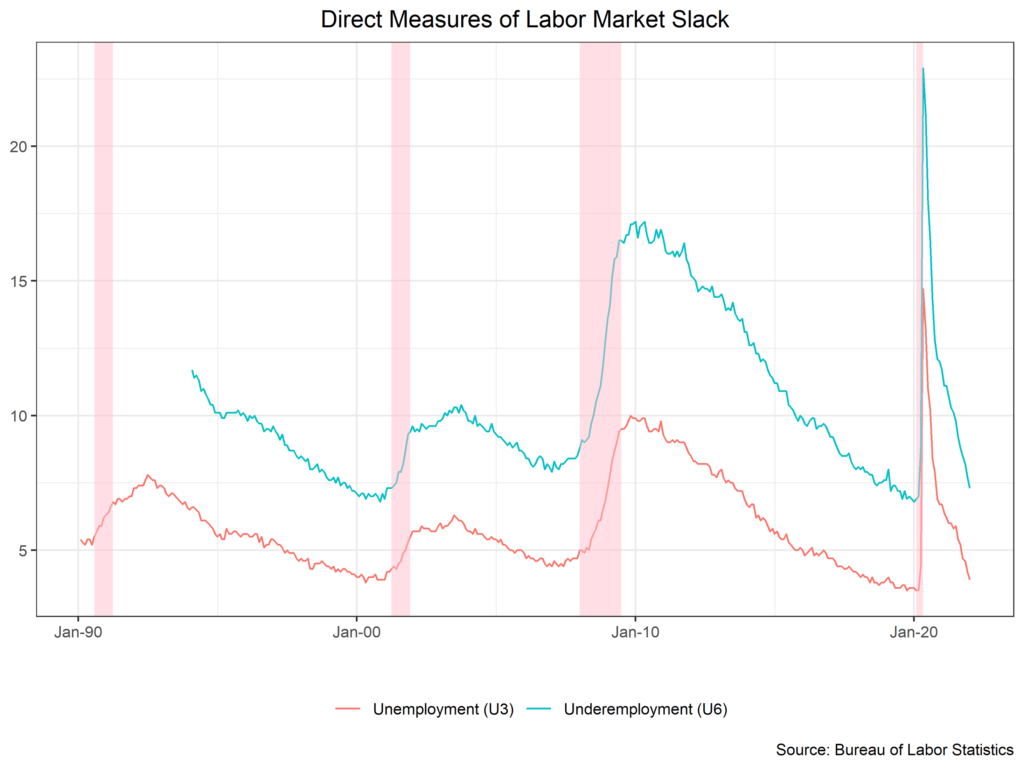

Take the labor market first. The December non-farm payroll report posted a modest gain of 199,000 but continued the trend of a rapid recovery in unemployment. The U3 unemployment rate began the year at 6.7% and has since declined to 3.9%, an astonishing pace compared to any prior recession (see the chart below). In aggregate, the labor market appears to be in good shape, and as the pandemic (hopefully) wains, it seems most likely that payrolls will continue to recover in 2022 as the economy strengthens further. However, the tension between hiring and wages is likely to increase. In order to bring workers off the sideline in an increasingly tight labor market, many employers will have to raise salaries to attract new hires. Real wage gains this year have been tepid, having begun the year at 3.8% y/y and ended at -2.4%.

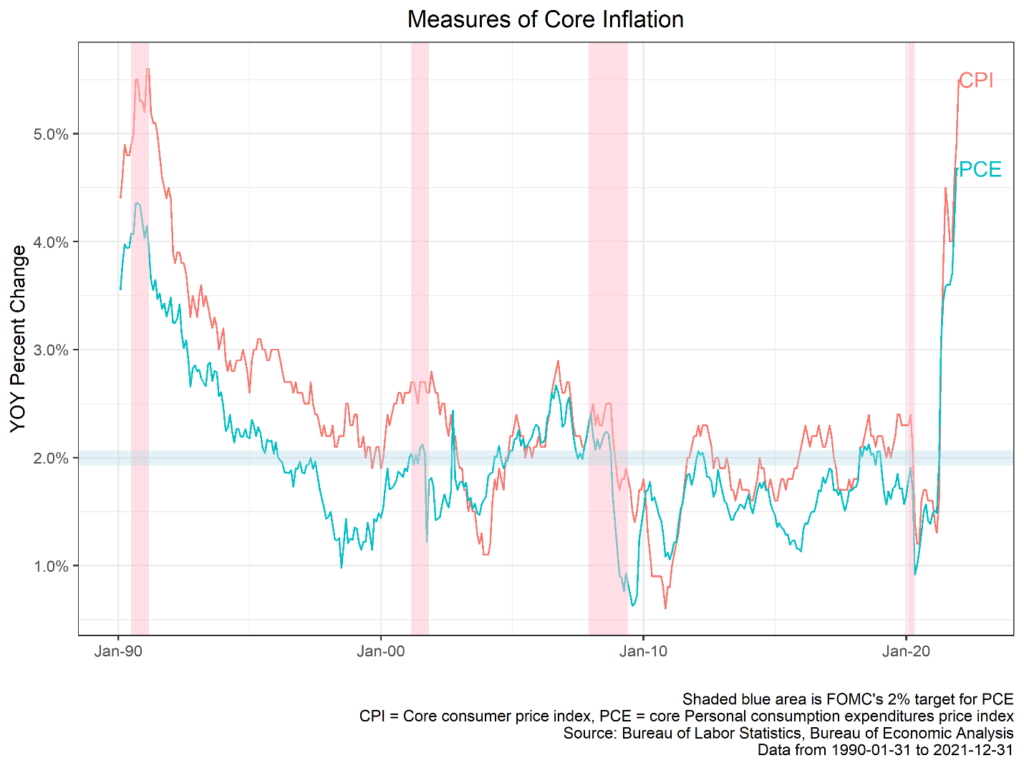

This, of course, brings us to inflation. Headline CPI entered 2021 at a meager 1.4% and finished the year at a very hot 7.0% y/y (0.5% m/m, 5.5% core). The December gain was led, as usual, by vehicles. The most likely scenario for 2022 is a moderation in inflation , but with price pressures that remain well above the Fed’s target. Much of inflation has been driven by components that were not (and are not) expected to be long lasting- the key risks for these categories are continued turmoil in supply chains and consumers maintaining their preference towards goods . Should consumers continue to buy goods, inflation would continue to be driven by cyclical factors. The structural risk towards moderation in the medium term is higher labor prices via a wage-price spiral and rent increases, the latter of which has begun to pick up steam.

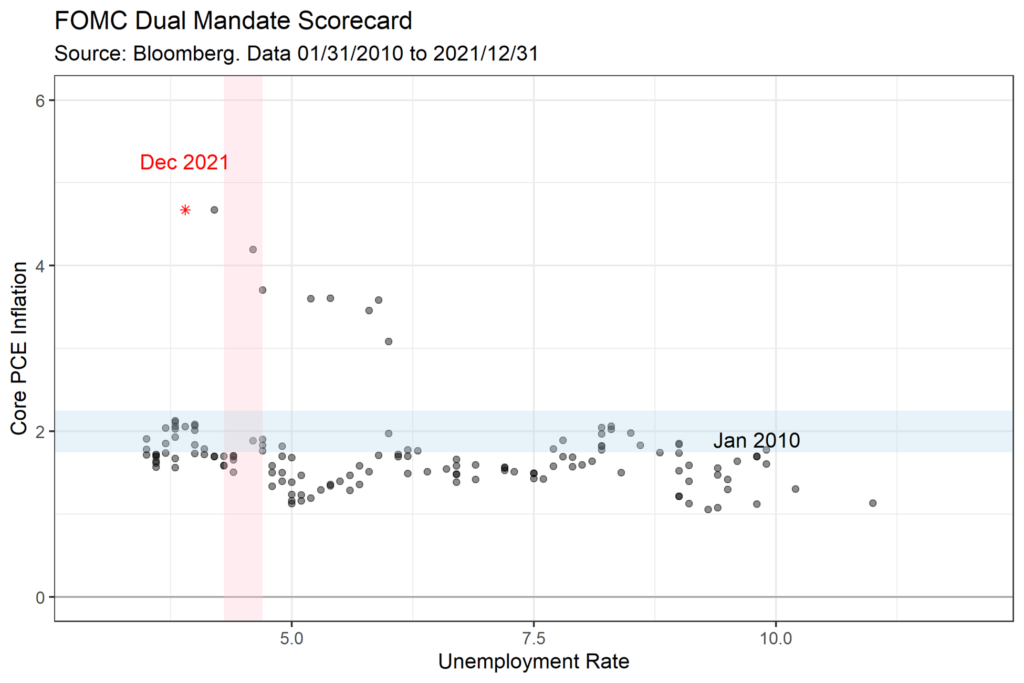

All this calls into question previous assumptions about the Federal Reserve’s reaction function. Since the Great Recession, the Fed has been faced with very few hard choices regarding its dual mandate of stable prices and unemployment. With the theorized neutral rate of interest low, inflation contained and unemployment dropping, the Fed had the luxury of keeping policy rates low and enjoying sustained economic growth and labor market gains. In fact, inflation appeared to be such a specter of days past that the FOMC shifted to an average inflation targeting framework to help dispel fears of a disinflationary or deflationary spiral.

The Fed no longer has this luxury, and, despite hopes of a swift normalization of supply chains and transitory price pressures, is now seen as more willing to act to combat hotter and more persistent inflation. This is despite the apparent mismatch in its toolkit with the current problem: that is, tamping down on the demand side via higher rates in response to a problem that has largely originated from the supply side. Ultimately, the concern is that if inflation proves persistent despite rate hikes, the Fed will be willing to tolerate rising unemployment in order to maintain credibility and adhere to the stable prices component of its mandate.

Although we’ve spent some time mentioning risks to the 2022 outlook, it’s worth repeating that 2021 was mostly sunny (or partly cloudy, depending on your world view) in economic terms, with massive labor market gains and a strong economy, inflation notwithstanding. Our base case for 2022 is similarly positive, with more economic growth and moderating inflation. Nonetheless, we will be watching economic data very closely over the coming year and listening for changes in the Fed’s policy stance.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

AIM-1/19/22-BP517