Fed minutes from last month’s meeting were released on Wednesday (8/16). After a summer of disinflation, many were hoping for a policy narrative congruent with the downward price movement we’ve seen in 2023: something akin to a final act. While there were a few dovish dissenters that were reluctant to raise the target rate, the overall message was that the work was not done. The Fed is concerned that inflation will remain stubbornly elevated away from the central bank’s 2% target.

The Fed’s communication has several potential implications. First, it will likely keep the prospect of elevated short-term rates intact for the near future. Second, Fed guidance reinforces a recent move higher in long-end rates to create more uncertainty for investors that were beginning to contemplate extending fixed income exposure further out in the curve.

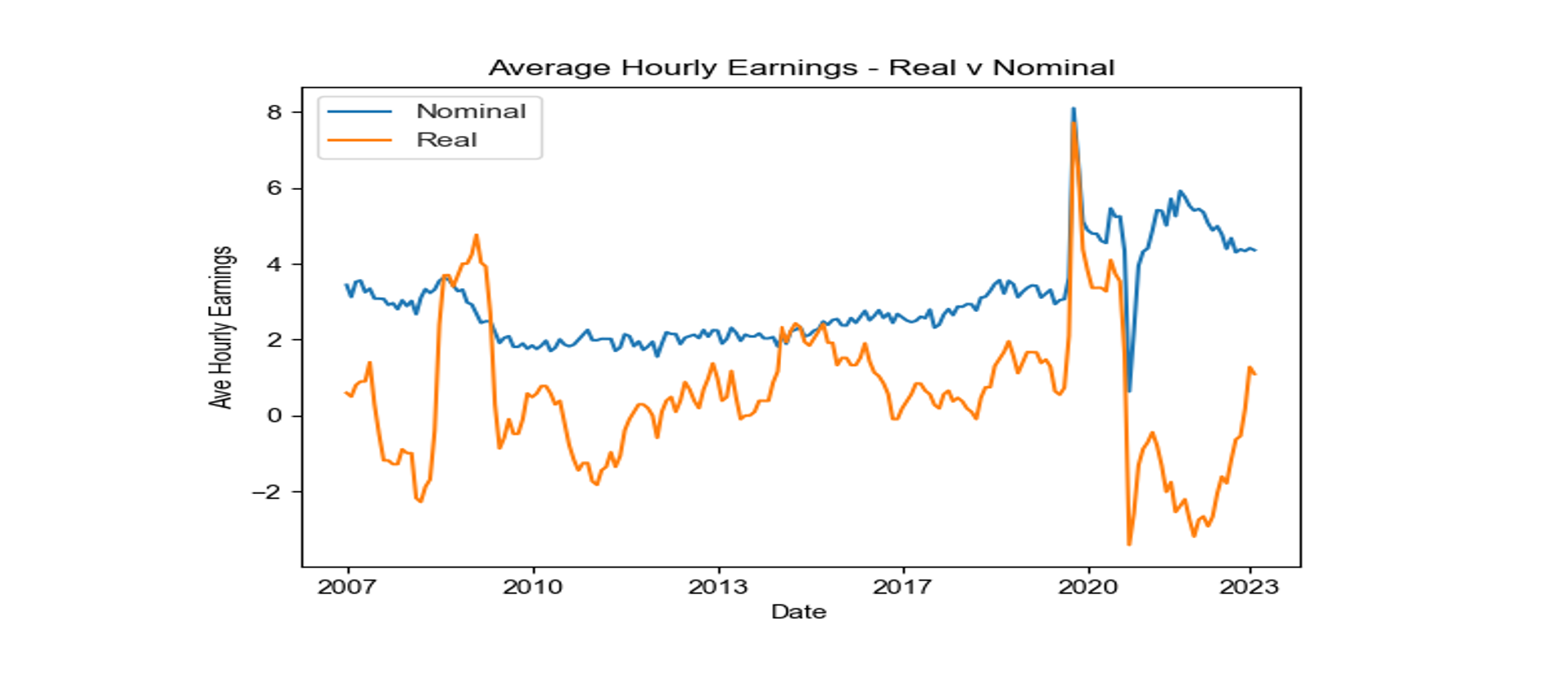

Complicating the picture is the stubbornness of U.S. payrolls, which have continued to string together solid gains month over month. While monthly gains have moderated, the U.S. unemployment rate sits near an all-time low, near 3.6%, almost a year and a half after the Fed embarked on its latest rate hike campaign. Average hourly earnings (YoY) have settled into a 4.25% – 4.5% range. With moderation in inflation, this has given consumers a boost in real purchasing power, pushing real wages back positive after almost hitting a near -4% (YoY) level in mid-2022 (see figure 1). This has kept the consumer in the game for now, confounding investors and economists looking for a 2023 recession.

Source: Bloomberg

Portfolio Positioning:

The crosscurrents of Fed policy, inflation and economic growth make portfolio position in fixed income crucial. During the initial phase of Fed rate hikes in 2022 and early 2023, the game plan was clear: stay short duration and higher quality, while interest rates moved, and credit spreads widened. Now, however, as we move toward this “terminal” rate phase and try to map the macro-outlook to other areas of the fixed income market, questions arise.

With credit spreads tight, risk in high yield seems asymmetric. Are investors left with essentially punting on duration risk? Are ~4.25% yields on 10-year Treasuries the point to start taking on duration risk, or are we moving toward 5% and above? The 2yr/10yr Treasury yield curve has remained at or below -0.5% for the longest period since the 1980’s. That will resolve at some point, but will it happen by short rates moving down or long rates moving up? Or both?

These questions are what investors must decide when positioning their fixed income portfolios in this environment. 2022 was costly if you were heavy in Treasuries and investment grade, and long duration. 2023 started off well on the prospect of moderating disinflation, but the road has proved challenging, as disinflation does not mean the Fed’s target inflation rate is in reach.

These are the questions Astor focuses on in our investment committee meetings, and our views on relative risks and rewards impact our decisions on how much credit and how much duration to have in the portfolio..

Our Current View:

• Short rates are yielding more than long rates in treasuries

• There is a higher probability of rates remaining elevated than falling in the near term

• Credit spread risk appears asymmetric

This has led Astor fixed income positions to remain in mostly short duration fixed income composed of floating and fixed rate treasury and investment grade positions. We continue to look for opportunities to either extend duration or investment grade exposure and also add credit risk to the portfolio. But as macro questions remain and the interest rate picture is challenging, we are pleased with our current risk profile. This approach helped the Astor Active Income portfolio outperform the Bloomberg U.S. Aggregate Bond benchmark both in 2022 and into the current year. Click here for current performance or visit astorim.com.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-417615-2023-08-18