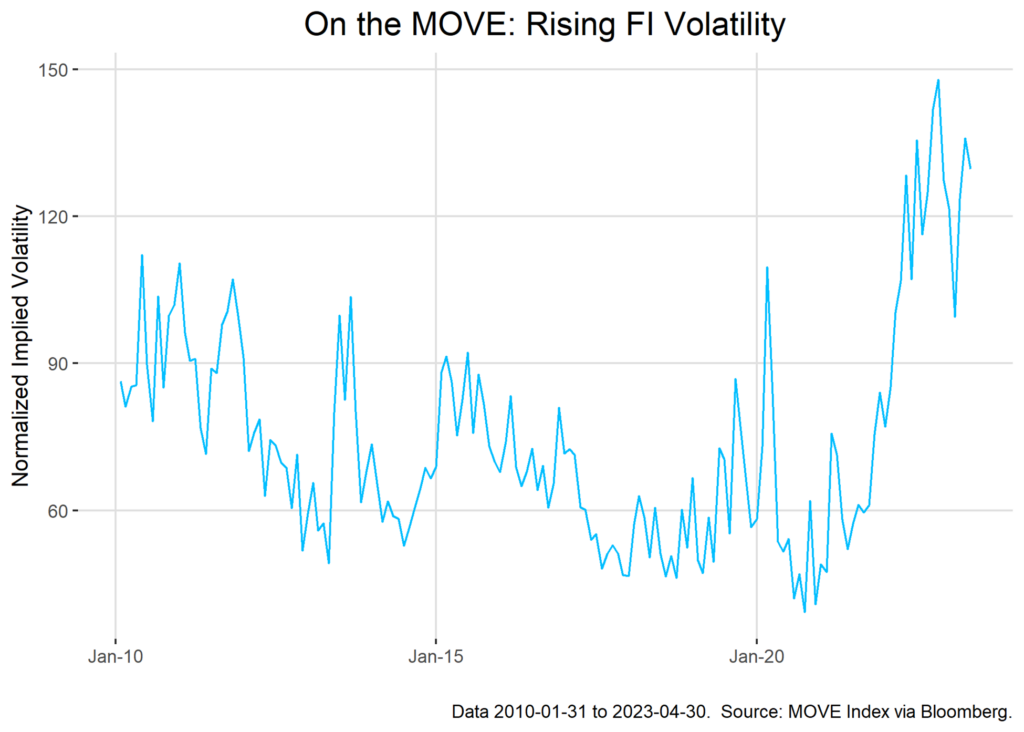

One can be forgiven for looking back on Fixed Income markets in the period between the Global Financial Crisis and the pandemic with something approaching fondness. The Great Recession and the period thereafter were dominated by concerns about the lower zero bound for rates and the need to stretch duration to get anything approaching reasonable income but were also characterized by low-rate volatility and mostly smooth sailing for Fed policy expectations.

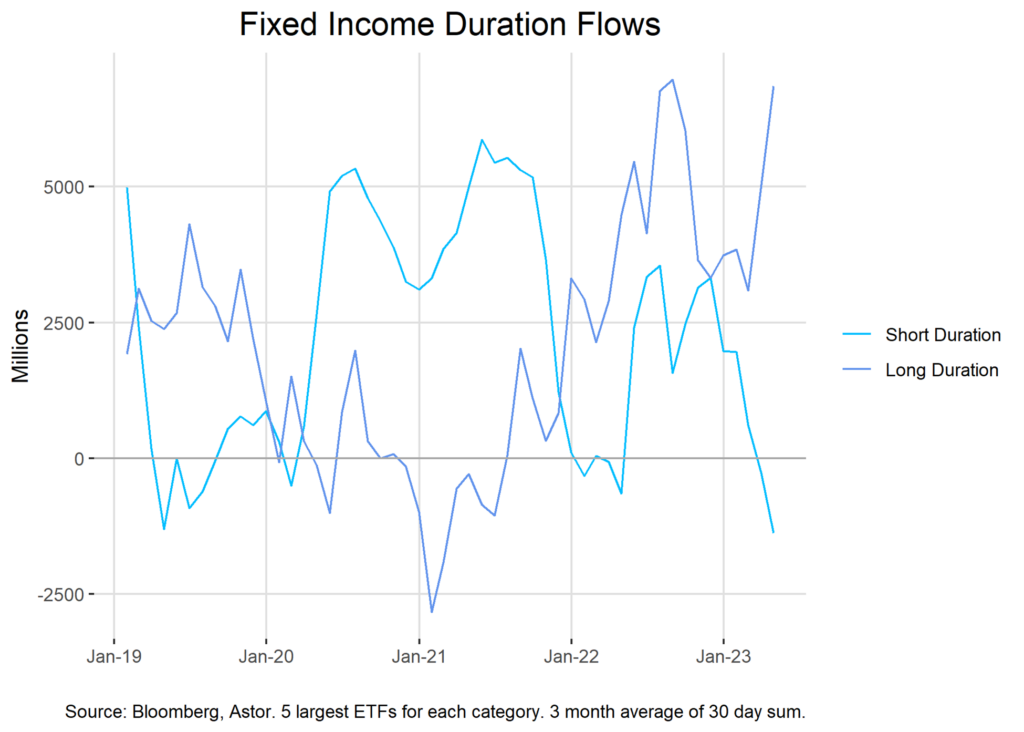

Those days look almost quaint in comparison to the current long-term. The MOVE index, a measure of fixed income volatility, has risen rapidly in the period following the pandemic. Whiplashed by unexpectedly persistent inflation and the ongoing response by the Federal Reserve, fixed income investors took refuge in shorter-duration bonds and cash in 2021, reluctant to take on duration risk during a period of unprecedented volatility. Those flows have recently reversed, as investors gain more confidence that the Fed is close to pausing (or cutting outright) and that inflation is tamed.

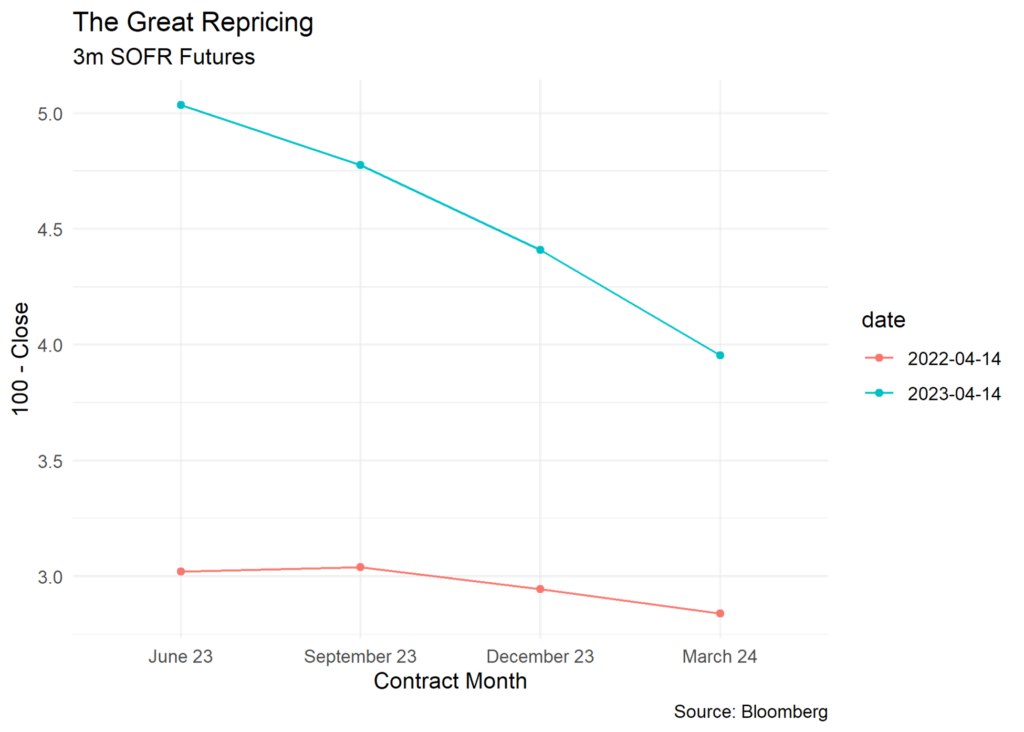

Market pricing for the front end (and thus, partly for the long end) is consistent with an adverse scenario unfolding in the near term. SOFR futures indicate an aggregate view of aggressive Fed cuts over the next twelve months from declining inflation and outright recession in the U.S. The U.S. 10yr yield was as high as 4.25% in 2022. It now sits at 3.5%, a significant move lower that must be justified by a fundamental shift in the underlying macroeconomic environment.

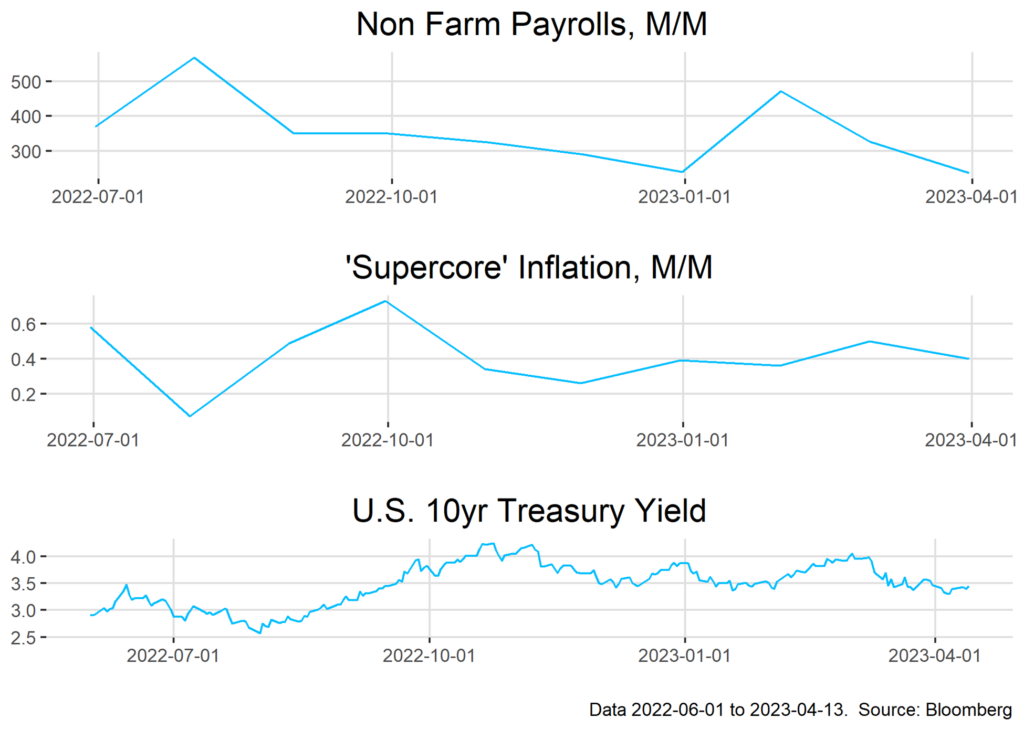

In our view, the market has probably overpriced the fleeting impacts of the Silicon Valley Bank debacle and is underpricing continued inflation and a Fed willing to stick to its guns. Headline, year-over-year inflation measures (CPI and PCE) have certainly moderated from peak levels, but there is still much to consider. Supercore inflation, which is focused on service inflation excluding housing, has shown little sign of slowing. The labor market is also surprisingly robust, with non-farm payrolls printing above the long term trend despite continued Fed hikes.

In sum, absent a material change, we think that the Fed Funds Rate is likely to remain above 5% throughout 2023, which suggests that long-term bond prices are quite rich. We will be more comfortable in considering longer duration assets when inflation shows a consistent and meaningful move lower and labor market dynamics normalize. We are watching unemployment claims closely as an indicative series for the labor market.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-375537-2023-04-24