The U.S. economy is not in want of compelling data points of late, with prints in all sorts of indicators well outside of historical norms. The challenge, of course, is that many of these series are in open contradiction. For its part, the Astor Economic Index® (AEI) indicates an economy that is cooling (or has already cooled). We discuss several of the series driving the AEI, as well as, the recent change in the market’s perception in the Fed’s reaction function, below.

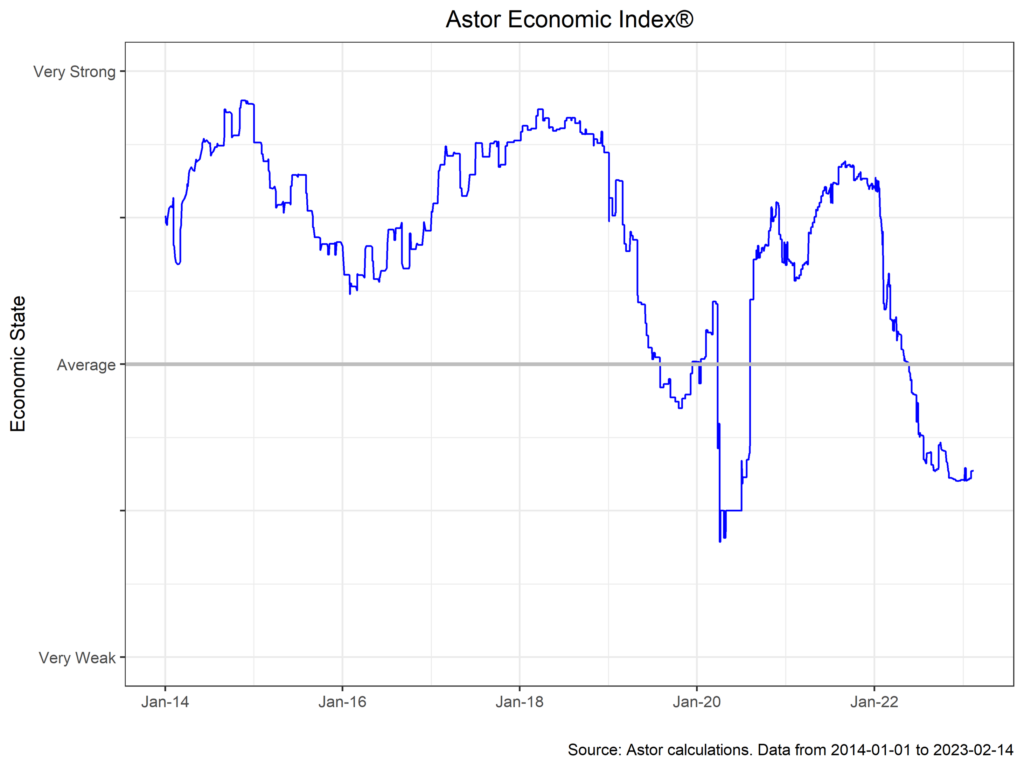

The AEI has been essentially stagnant in 2023, with continued weak PMIs counterbalanced by a red hot labor market. The current level of the AEI has historically coincided with weak economic growth, but it remains above the “very weak” depths.

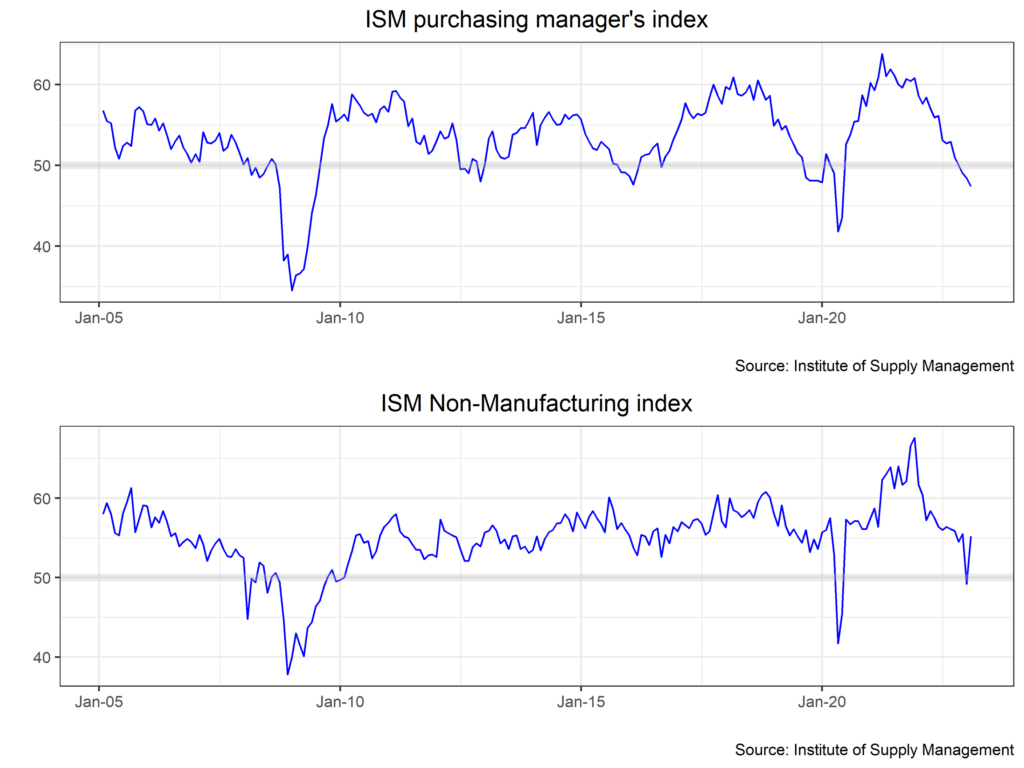

The non-manufacturing component of Purchasing Manager Indices (i.e. services) staged a remarkable rebound in January, with the index printing at 55.2, up from 49.2 the month prior and returning to a level indicative of sector growth. The uptick was led by business activity and new orders, two crucial subcomponents. ISM Manufacturing, meanwhile, continued its decline, printing at 47.4, with new orders falling. A potential driver is that the U.S. consumer has perhaps resumed normal consumption habits, with a preference for services over goods.

Non-farm payrolls were well above consensus, printing at 517,000 m/m (consensus forecast 189,000). There were some minor quibbles around seasonal adjustments and other methodological concerns, but make no mistake: the magnitude of this number is difficult to handwave away. The labor market sets up an interesting dynamic for the Fed (and for investors), as policymakers would like to see a substantial easing in labor markets (and thus in wage growth). So far, there have been no signs of companies slowing hiring or shedding jobs beyond anecdotes in the tech sector.

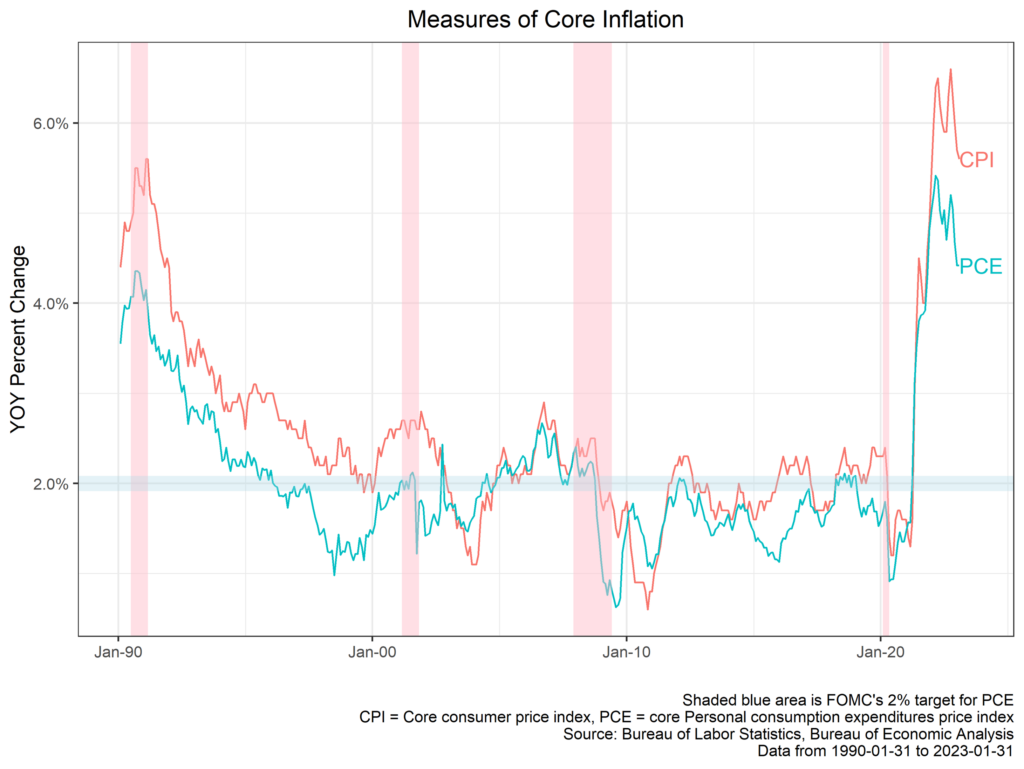

CPI came in appropriately hot at 6.4% (0.5% m/m) , with core at 5.6% (0.4% m/m). Core inflation appears to have leveled off at a higher level than the Fed would like, with the 4 months or so of m/m readings around 0.3% – 0.4%. Hopes that the services component of inflation would start to trend downwards on the back of lower shelter costs were dashed, with core services ex. shelter up 0.27% m/m. Good prices, however, have continued to soften, suggesting that the Fed will be closely watching services in the months to come

Both non-farm payrolls and CPI will probably give the Fed serious second thoughts towards its telegraphed rate hike pause, which was thought to be as soon as March/April. We’ve noted repeatedly that market participants and the Fed were at odds around the future path of monetary policy. The market had been discounting the possibility of higher for longer monetary policy for some time, with expectations for as much as 50bps in cuts in 2023 observed in Fed Funds Futures markets as recently as last month. These readings, as well as Fed communications, have finally led the market to take the Fed at its word when it says the terminal rate is likely above 5%. As things stand now, the market is pricing a terminal rate around 5.3% (suggesting another two hikes of 25bps) and dropping back to 5% around year end.

The economic tea leaves are a bit of a muddle at the moment, but the U.S. economy seems to be getting along fine, with some signs of cracks in consumer balance sheets and survey data. The possibility of a hard landing, with the Fed hiking well into restrictive territory, as well as that of a soft landing, or no landing at all, seem equally likely at this point. We will be watching incoming data closely for any advance signs of broadening weakness in the U.S. economy, and for incipient softness in the labor market.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-350159-2023-02-14