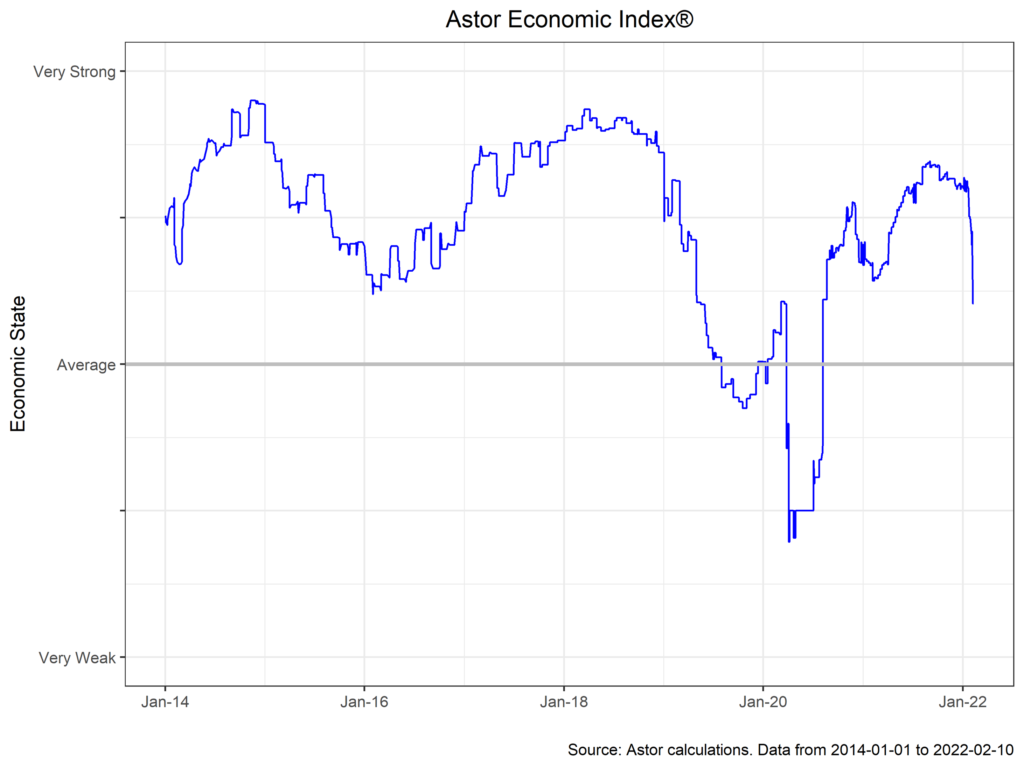

January proved an exciting month for macroeconomic data, with some clarity gained on the near-term trajectory of the U.S. economy and the state of inflation. We’ll begin with the Astor Economic Index, which has begun to move down rather precipitously of late. Although the AEI’s movement over the past month might make for a concerning looking chart, we have been talking about this likely decline for some time. Our expectation, barring any sudden shocks, is that domestic output will revert towards trend as fiscal support rolls off consumer balance sheets and the threat of the pandemic begins to wane. The AEI is capturing this return towards potential output, and indeed remains above what we see as average economic growth. The AEI’s reading comports with other nowcasting measure: the Atlanta Fed, for example, sees Q1 real growth at 0.7% (Q/Q SAAR). A composite of private forecasters is slightly more optimistic at 1.7%.

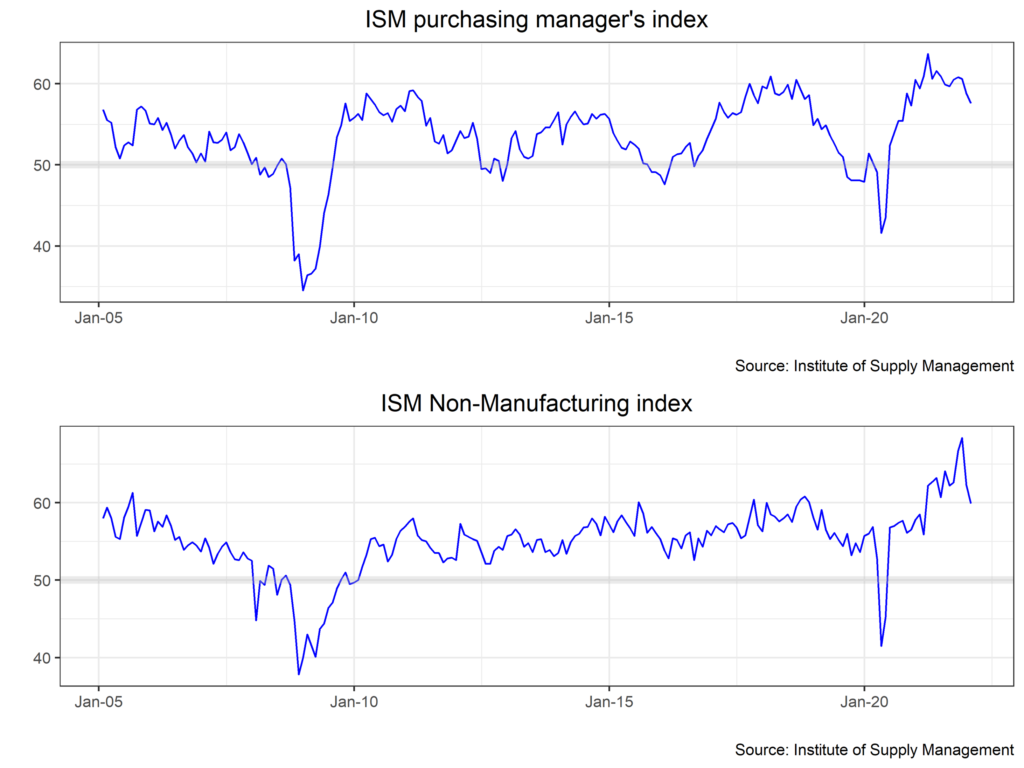

Much of the data support the economy coming off the boil into something more akin to a simmer. Purchasing Manager Indices, for example, have declined from their lofty and historic pandemic highs to something more approximate to historical norms. To be clear, both services and manufacturing PMI point to solid growth, and some of the decline is in fact salubrious: for example, delivery delays and backlogs dropped, pointing to improvement in supply chains.

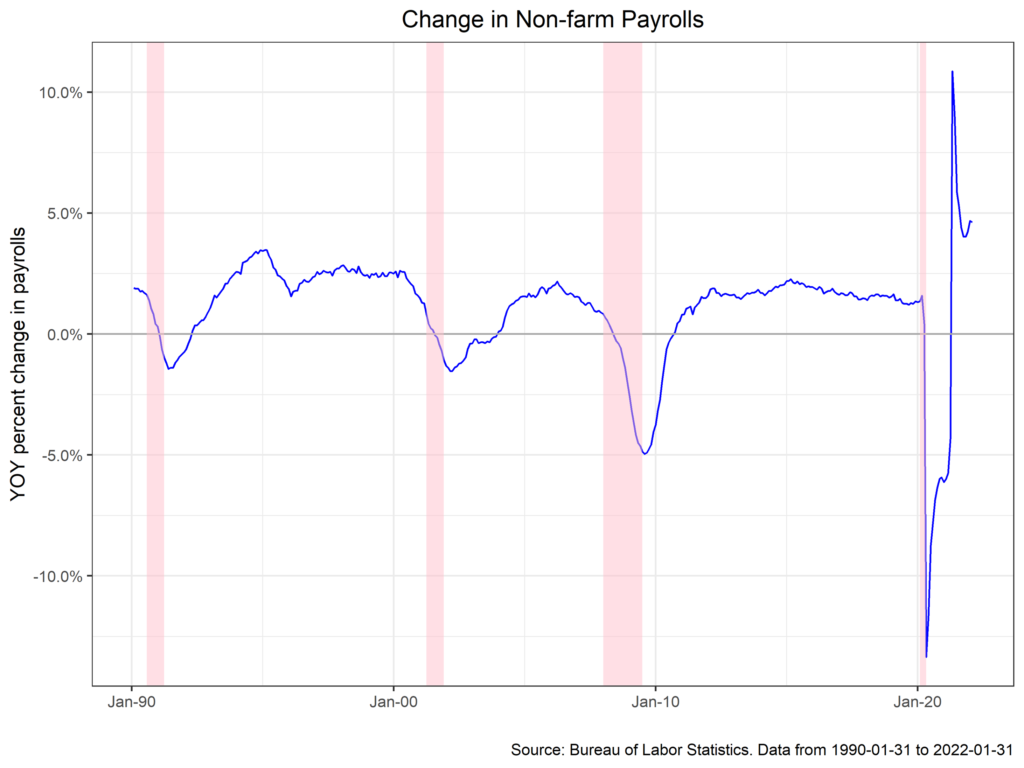

Non-farm payrolls, meanwhile, are tougher to parse. January’s number flew in the face of expectations, printing at a solid month over month gain of 467,000 with some very robust upward revisions of prior months. Prima facie, the gain suggests a resilient workforce against the backdrop of an omicron surge. However, digging behind the headline results in a more fraught interpretation. Some statistical quirks around population estimates probably caused the number to be stronger than it would have been otherwise, and other adjustments make clear the impact that omicron had on the workforce. Average hourly earnings improved 5.7% y/y (1.7% in real terms), consistent with comments by managers in PMI reports regarding difficulties hiring and retaining workers.

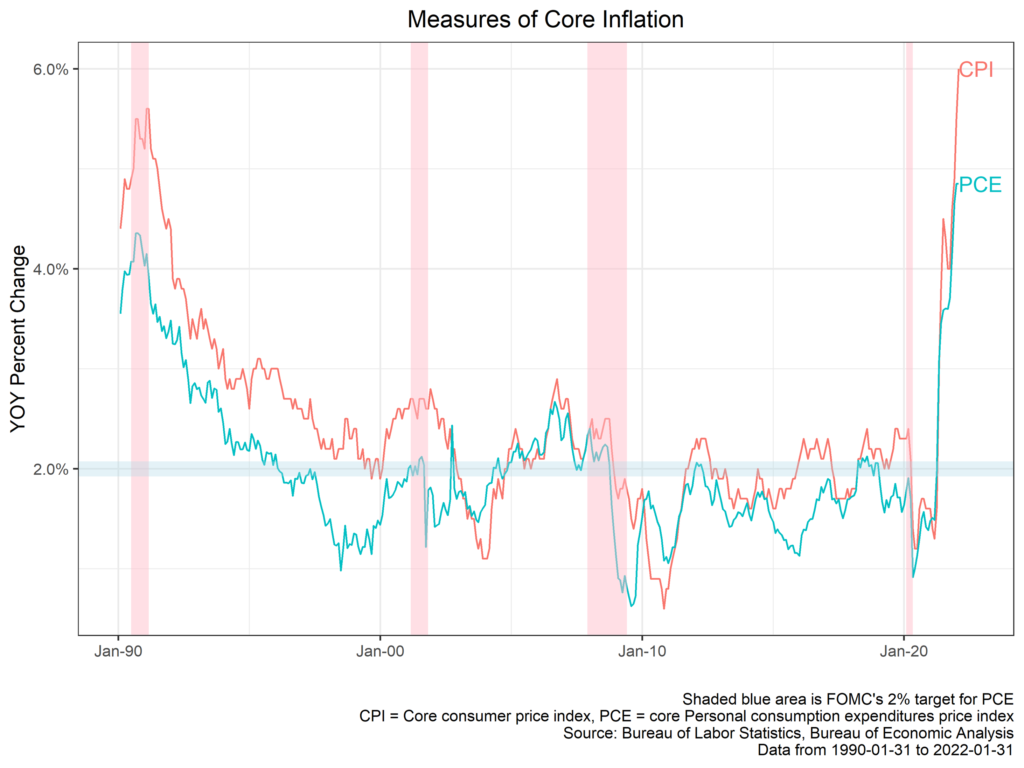

Inflation contained little of the opacity seen in payrolls. The Consumer Purchasing Index print for the month of January was undeniably hot at 7.5% y/y (7.3% survey), with the core figure at 6%. The month over month figures were at 0.6%. Notably, price pressures are now seen across all categories, including the previously cooler services components. All eyes are now on the Federal Reserve. Market participants are now pricing a 50bps hike at the March meeting, with the yield curve flattening as a result. The Fed, however, appears less clear eyed about this prospect, with recent comments suggesting a 25bp is still the most likely outcome.

In sum, the economy is ticking along well, but inflation and the Fed’s reaction are crucial downside risks to the outlook. Although difficult to forecast, our baseline view is that inflation will begin to moderate over the next quarter. However, should price pressure remain durable and the labor market robust, expect the Fed to move quicker than previously thought. We will be listening to communications from the Fed very closely over the coming month.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

AIM-2/11/22-BP540