Recent Dollar Trends

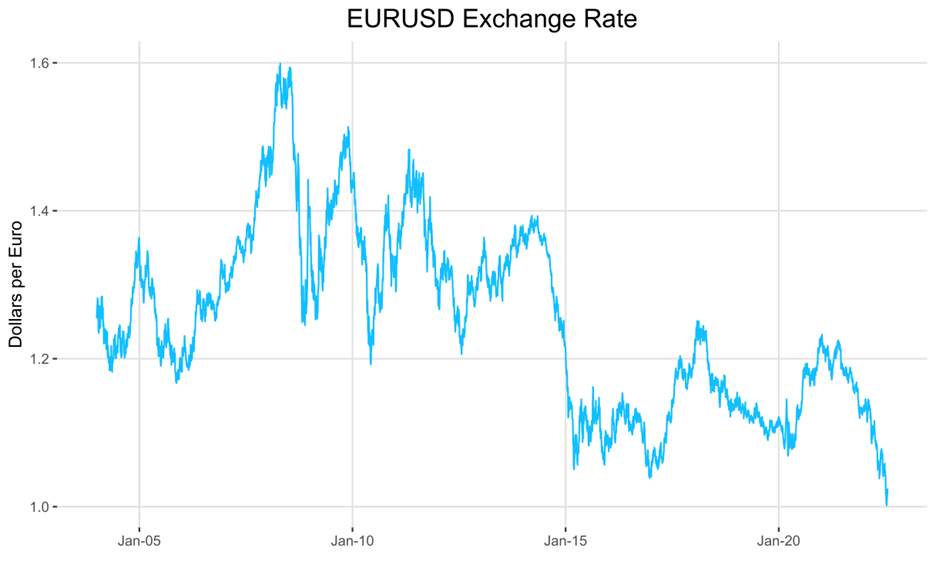

The U.S. dollar is very much in the limelight of late, with the greenback relentlessly climbing against its developed market peers. The euro to dollar exchange rate (EUR/USD) is closely watched as a gauge of global sentiment and is the most heavily traded currency pair in the world. The euro recently touched parity with the dollar this month, with one euro worth one dollar – a level last seen 20 years ago.

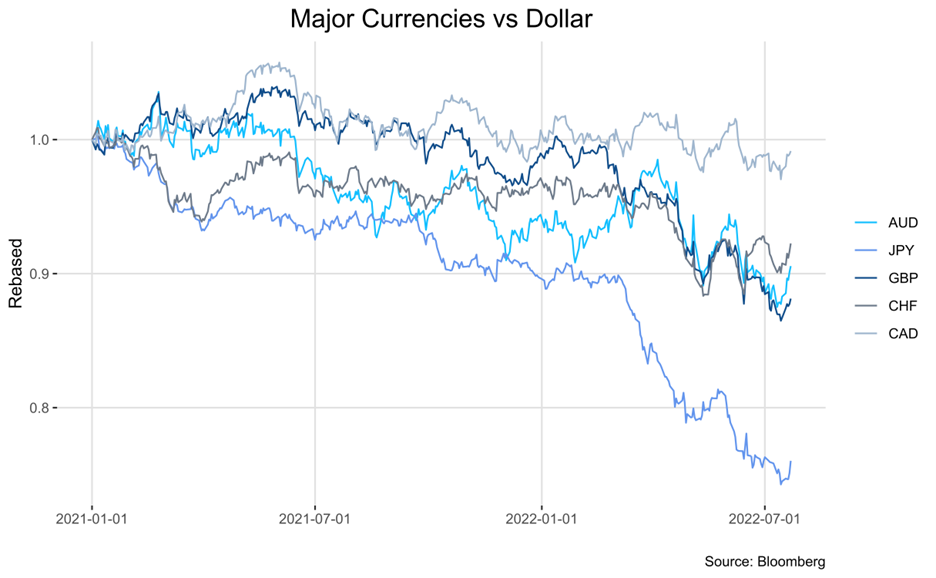

The euro, however, is not alone in depreciating relative to the dollar. Most of the Majors have weakened throughout the course of 2021. What is driving this trend, and can we expect it to continue?

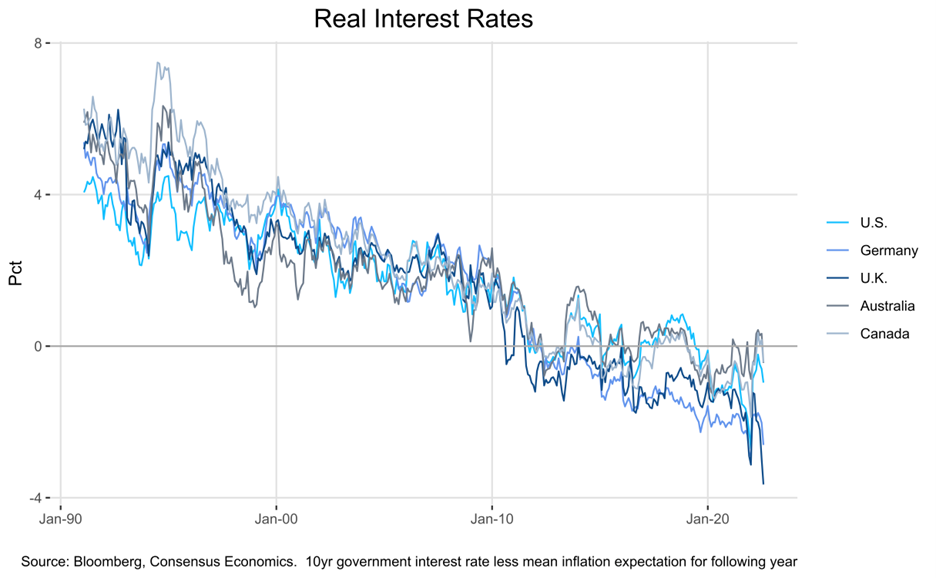

Central banks around the world are facing rapidly increasing price pressures the world over. Real interest rates (proxied by nominal rates less inflation expectations in the chart below) have tumbled throughout Europe and the U.S.

Nonetheless, countries face notably idiosyncratic macroeconomic situations (take, for example, the natural gas crisis in Europe). As a result, policy responses have varied widely. The central banks that have been most aggressive in combating inflation have seen concomitant relative strength in domestic currencies.

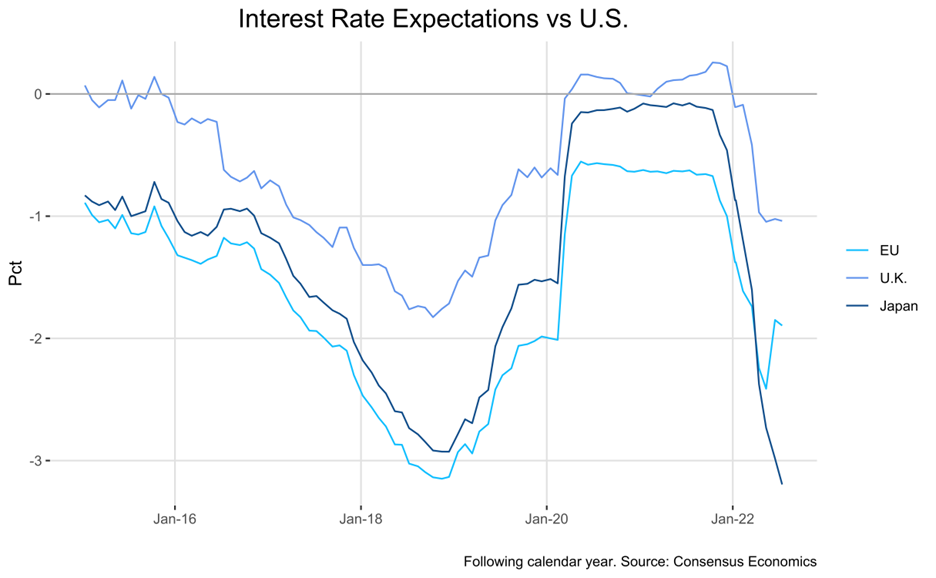

Australia and Canada’s central banks have been among the most hawkish developed economy banks in 2022, raising policy rates by 1.35 – 2.5% each. Their currencies have fared relatively well against the dollar. Being major commodity exporters, of course, is also helpful. The ECB, meanwhile, has just raised rates by 50bps for the first time in a decade, and the Bank of England has hiked 1.25%. These interest rate differentials (that is, interest rates relative to the U.S.) and expectations thereof are the main drivers of dollar strength this cycle. The chart below depicts economists’ expectations of U.S. interest rates a year ahead, less expectations for a second country.

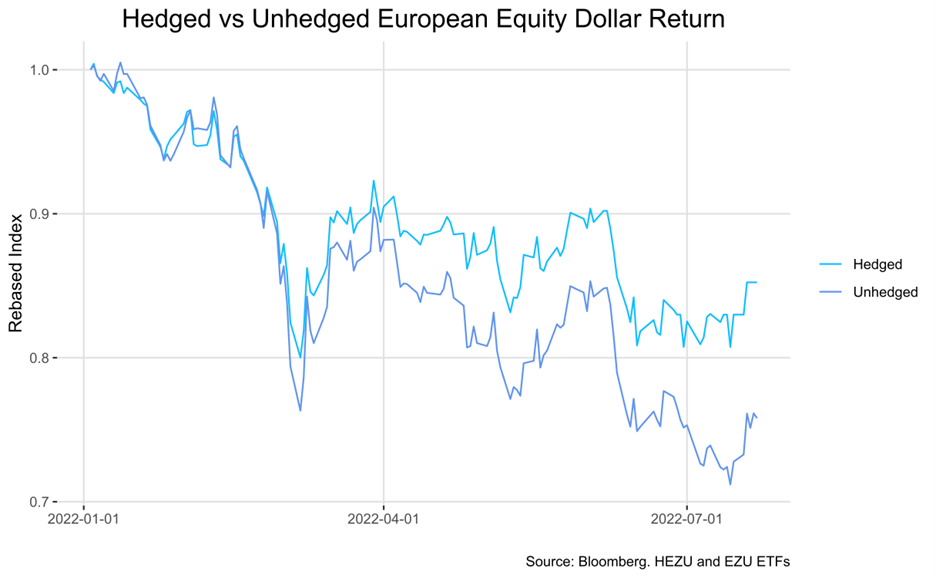

Even those who do not speculate directly on currencies should be aware of major trends in FX markets. A hedged equity exposure to the Eurozone has performed 13% better than unhedged exposure year-to-date.

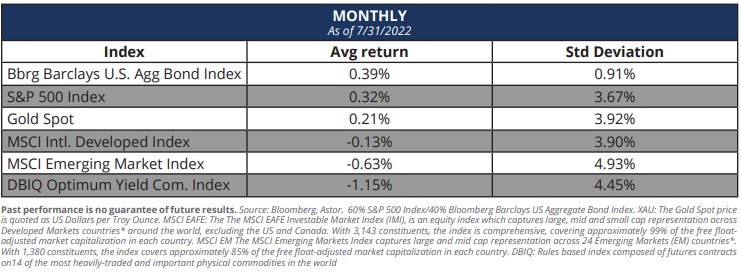

Indeed, a strong dollar has typically been a mixed bag for risk assets. The table below depicts the following month average return and standard deviation for asset classes after the Bloomberg dollar index has seen a 10-year z-score of 1 or higher. Notably, investment bonds and golds perform well: dollar strength often coincides with risk-off behavior and the search for havens, roles that bonds and gold typically fulfill. International equities and EM equities underperform, which is almost tautological, although one could have reasonably expected some form of mean reversion following a period of local currency weakness. A strong dollar is also bad for commodities, which aligns neatly with theory – most commodities are priced in dollars, and so a higher price leads to weaker demand.

What are the prospects for continued dollar strength in the second half of 2022? Any hint of global recession, additional geopolitical conflicts, or liquidity or banking event would add to dollar tailwinds via the dollar’s haven role. Much of the market, however, is expecting the Fed’s hiking cycle to come to an end in 2023, with rate cuts following a shallow recession. If a U.S. recession dampens domestic inflation, does not spill over to the rest of the world, and causes the Fed to cut rates, the dollar would likely depreciate. Alternatively, the Fed may cap rates in early 2023 while other central banks continue to hike to catch up, which in net would be dollar bearish. In the near term, the likely path is one of retrenchment – there is ample evidence the ECB needs to play catch up, and the bulk of Fed hikes is probably already behind us.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-290096-2022-08-01