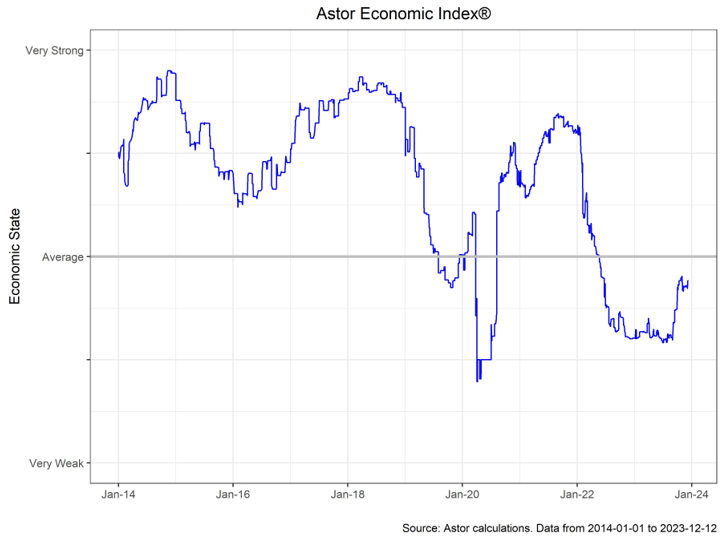

Our last reading of the Astor Economic Index® (AEI) in 2023 places U.S. economic growth in about average territory, up modestly from the beginning of the year as expectations for future growth improved. The consensus narrative agrees with this reading, seeing an economy that has finally shook off the pandemic induced shackles and returned to a more normal state. In addition to our usual reading of last month’s data, the end of the year provides us with the opportunity to place those figures in the context of 2023 and the twists and turns of the economy over the past twelve months.

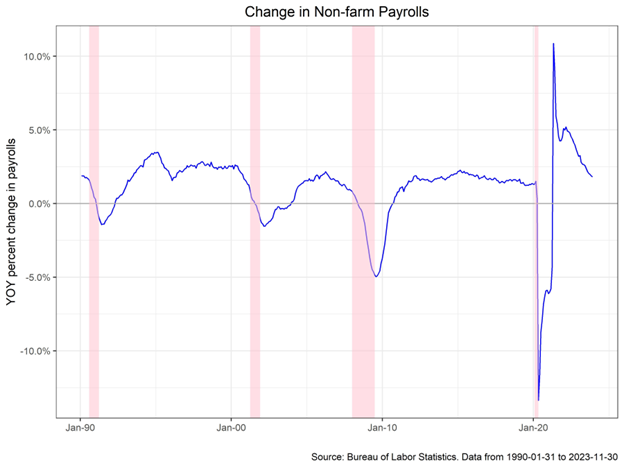

The labor market is always our first port of call, and we ended the year with non-farm payrolls up 199,000 m/m, up slightly from October and at a rate of change more in line with historical norms. Recall that nonfarms averaged 412,000 in 2022, much above the rate consistent with an economy around potential. This continued cooling is likely encouraging to the Fed, but policymakers would also like to see further cooling in wages.

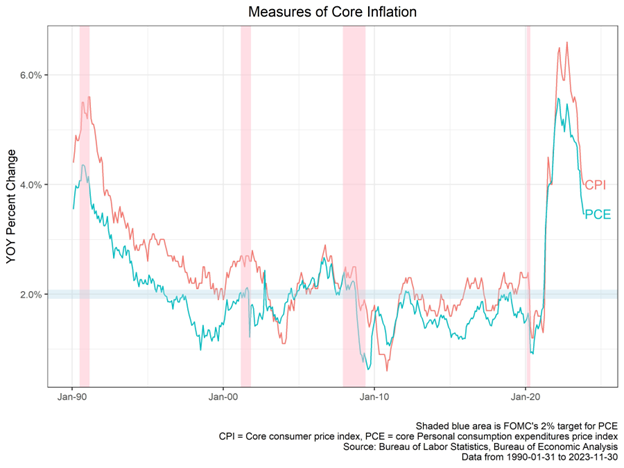

Inflation printed at 4% (core CPI y/y), the same rate as the month prior. Supercore inflation, which strips out housing from services and is seen as Fed Chair Powell’s favored measure, reaccelerated to 0.44% m/m and was led by transportation and medical care, highlighting the difficulty in the last mile of cooling. Inflation had begun the year at 5.6%, much too high, and remained there for around four months. Overall, the progress to date in bringing inflation back down to target as been encouraging, particularly with the perspective that employment has not needed to crater as a result. Nonetheless, we still have some ways to go, and much of the easy work from healing supply chains and diminishing fiscal stimulus is now behind us.

In sum, the macro picture progressed through 2023 much better than most had hoped for, with inflation moderating towards target, no major upheavals in financial markets, and growth and the labor market cooling but resilient. 2024 is unlikely to be an exact repeat, with some nascent signs of softening in employment trends, and the last bit of inflation (mostly shelter) harder to defeat. We’ll be watching the Fed, the consumer, and hiring closely in the new year.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part

2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-470994-2023-12-18