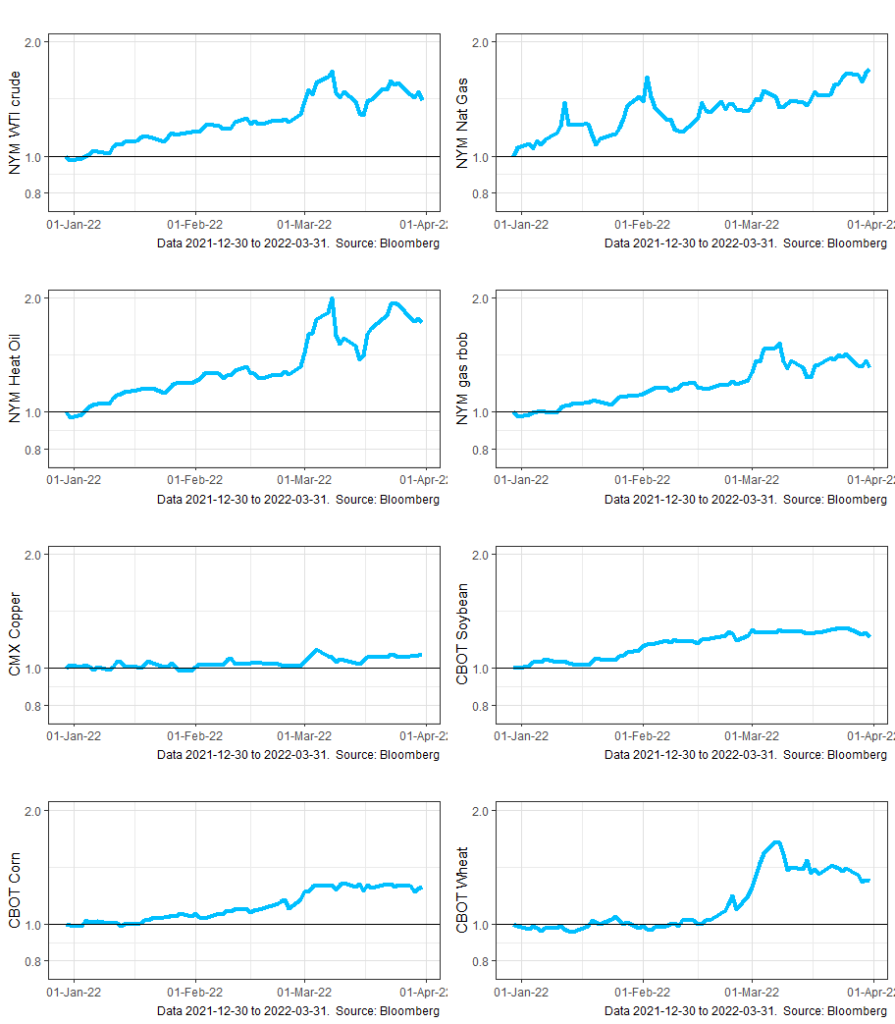

Many of the most visible commodities – energies and grains – appreciated a great deal during the first quarter as shown in the charts below for eight of the more well known commodity contracts.

There are macro factors both boosting and restraining commodity prices:

- On the bullish for commodities side:

- Shift in the composition of spending from services to goods

- Supply chain factors

- Additional unexpected disruptions from the Russian invasion of Ukraine

- On the bearish for commodities side:

- Weakening prospects for world growth

- Dollar strength making most countries primary material bill more expensive

There is an old wall street saying that the cure for high prices is high prices – that is demand destruction and increased supply should return prices to a new equilibrium. This process takes time, of course, and prices normalizing next year is cold comfort for people who have to buy gas today.

Of course, the interesting thing about commodities is that each is a world unto itself. Corn and copper have nothing in common, but we lump them into a residual category and call them commodities. I will pick out a few idiosyncratic factors below.

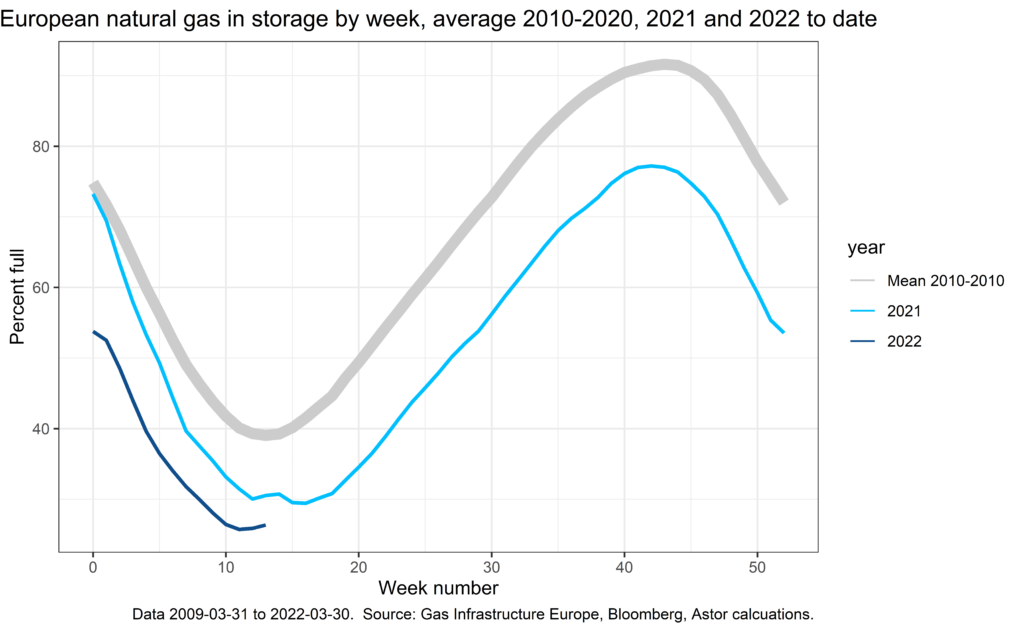

All energy futures trended up all quarter with heating oil briefly doubling in price in early March. A great deal of this is probably attributable to the war, though problems also show up in the supply numbers. The most dramatic is the European natural gas situation which, in turn, effects natural gas prices here in the US. This chart shows how much of a hole Europe started the year in: natural gas was only about 55% full in the beginning of the year vs a typical 75%.

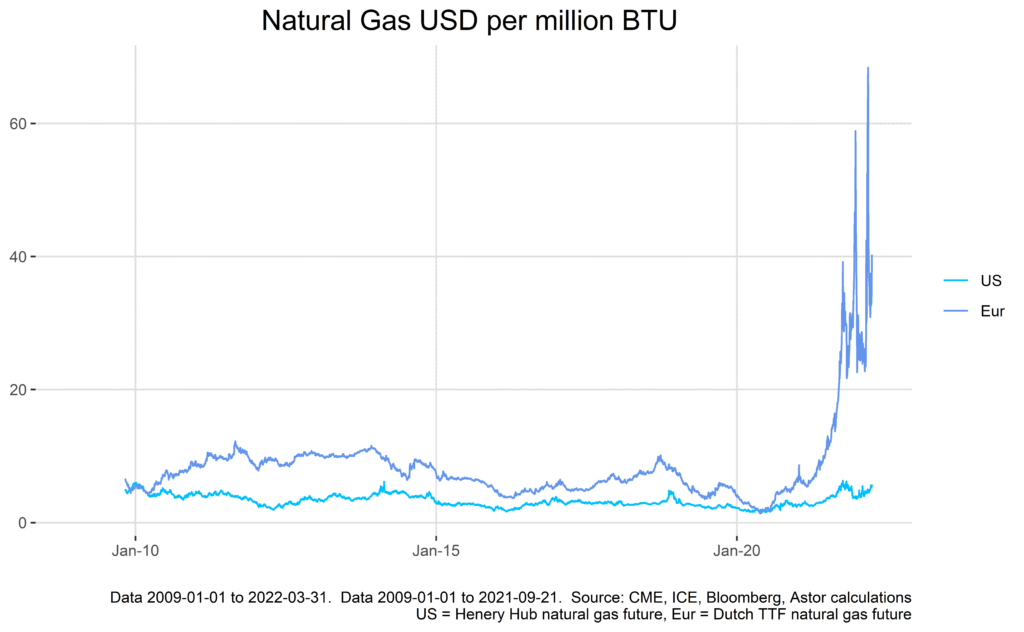

U.S. consumers may be surprised but natural gas prices in Europe are far higher than here. In the last year they have gone from about double to about six times as high. Of course, there is limited capacity to ship U.S. gas to Europe, but more is being added all the time and that positive spread likely has had some effect on moving U.S. prices higher.

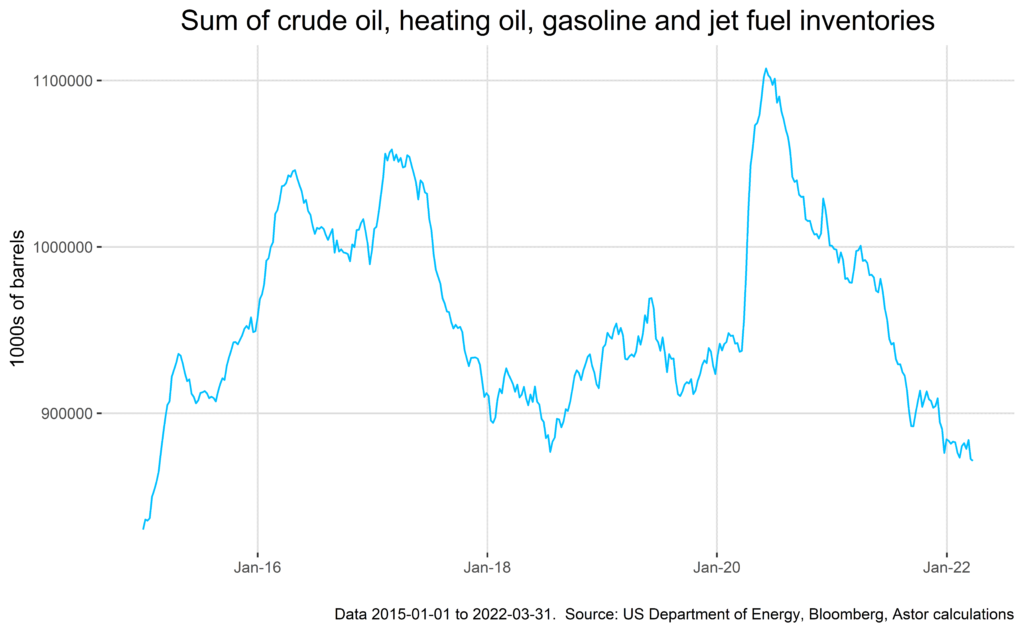

In crude oil, the world market is now expected to be in deficit (by about 0.5% of consumption) as opposed to last quarter’s expectation of a surplus of about 1%. The Biden Administration announced that it will supply oil from the strategic reserve which may ease pressure somewhat but also may have some psychological effect. Today, however, petroleum and derivative inventories are at fairly low levels.

There has not been as much pickup in production with this surge in price as the previous few years would have suggested – reportedly smaller producers are under more severe financing constraints than was the case a few years ago.

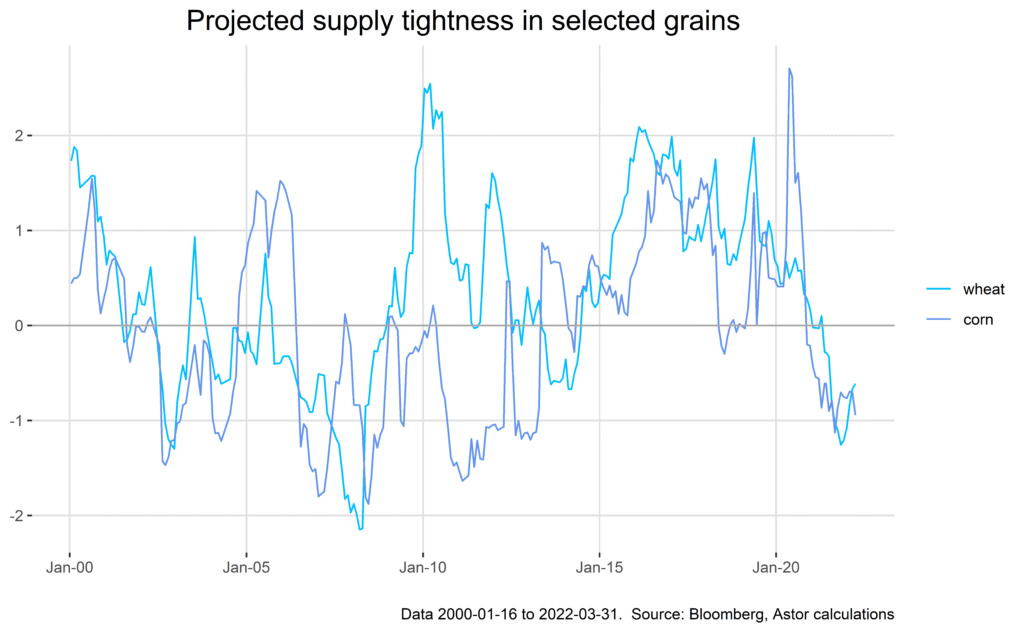

Grains were another area of rapid appreciation this year. The chart below shows a proprietary measure of grain supply, where a positive number is above average levels of grain the a negative number means there is expected to be less grain than usual. Both wheat and corn are looking somewhat tight but not unprecedentedly so. Ukraine and Russia together usually produce about 7% of world production but about 30% of world exports, so it makes sense for prices in exporting countries (such as the U.S.) to appreciate. Farmers are currently making plans for planting season so large moves could materialize.

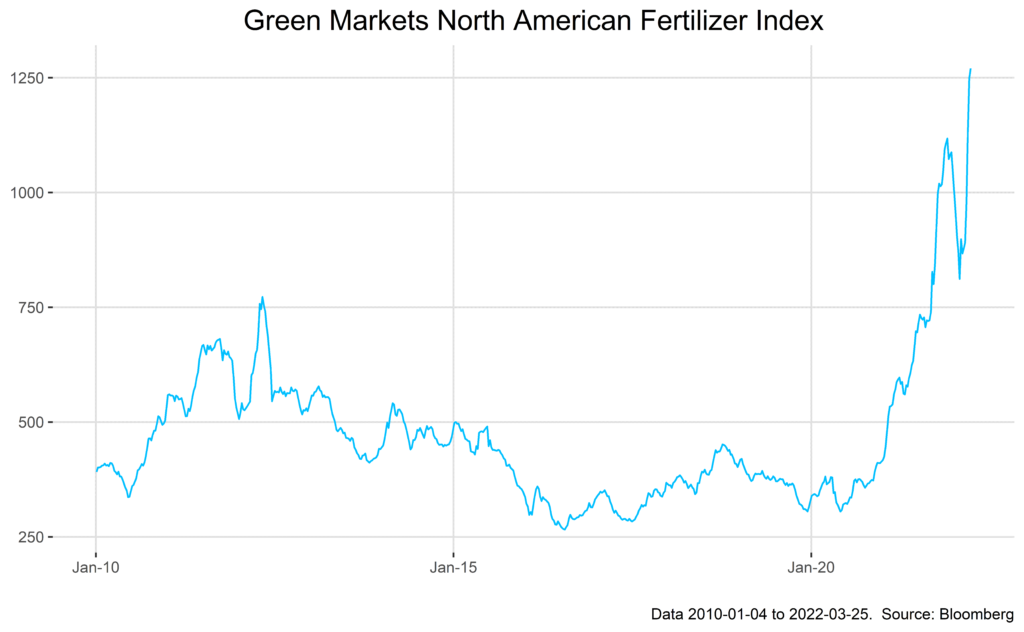

Russia also typically exports a good amount of fertilizer which the chart below shows has doubled in price recently to unprecedented levels. Tying everything back to energy, natural gas is a vital input to nitrogen fertilizer so natural gas staying expensive will tend to put a floor on prices as well, unfortunately.

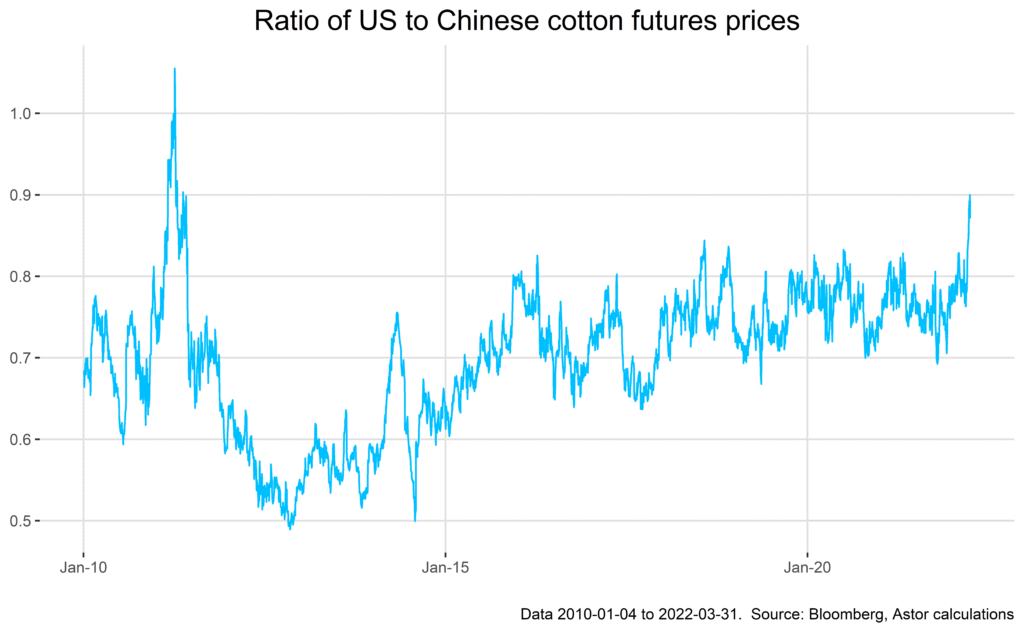

Worldwide cotton stocks are projected to be somewhat lower than normal by the end of the growing season, but recently the price of US cotton has spiked tremendously relative to Chinese cotton in the last few weeks.

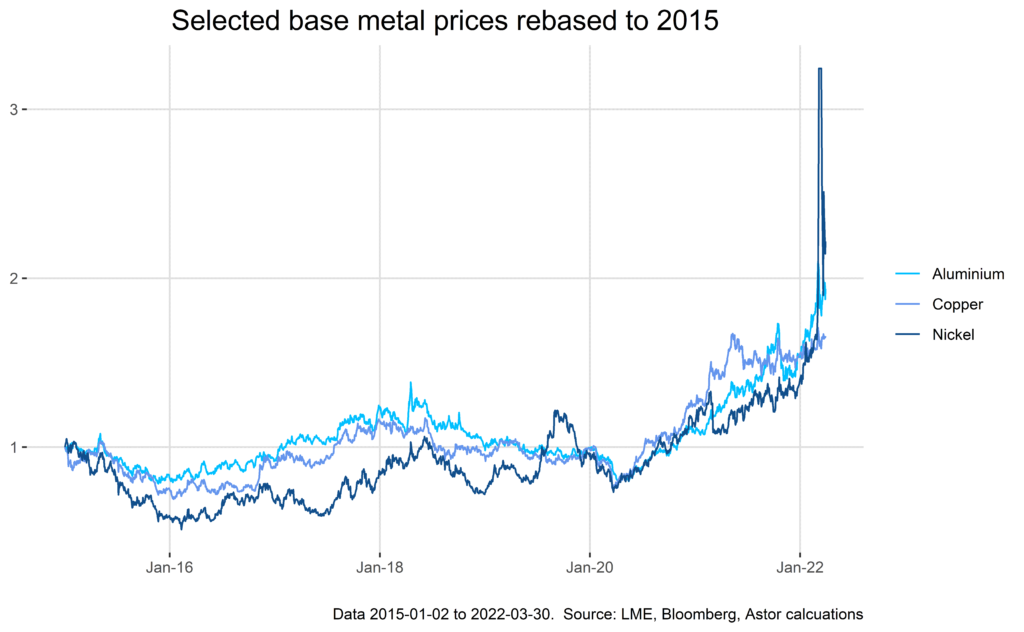

The world’s attention was briefly brought to nickel prices in early March when prices spiked even more dramatically than other prices thanks to a large producer’s hedging program getting margin calls. The market was suspended for several days but has begun to return to similar levels of appreciation as other base metals have enjoyed.

Existing supply shortages have been exacerbated by the unknown fallout from the war in Ukraine, but it may be the case that bad news has been priced into markets and prices may normalize from here.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

The information provided here is not intended to be seen as trading advice or a recommendation to trade in commodities. Commodity investing has unique risks due to leverage, margin requirements, and market volatility. You should discuss these risks with a financial professional before investing.

AIM-4/7/22-BP558