As the recent bank failures hit the news wires the headlines became sensational, with some commentators claiming that the system was imploding. Ironically, just weeks ago, the banking system was characterized as ‘bulletproof’.

To be clear, this is not 2008. That was a true banking and financial crisis with a complete breakdown of the banking and financial system, rates were not the main driver. Lack of oversight in the mortgage markets, easy lending practices along with many other leveraged assets created a perfect storm when rates started to rise.

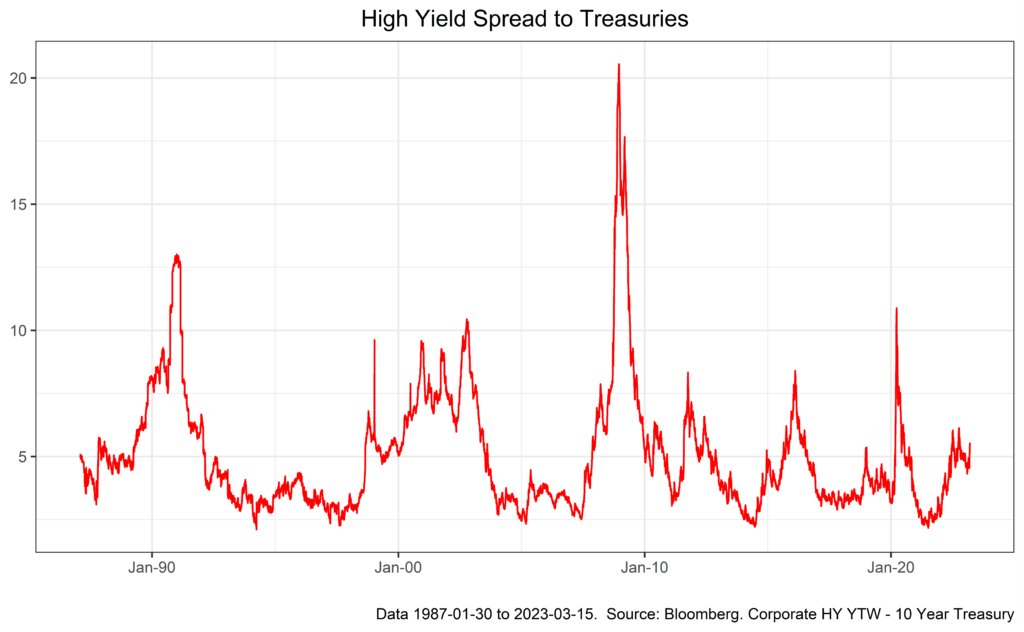

In my view, 2022/23 is different. While credit is relatively stable (chart 1) rates have figuratively exploded! The Fed Funds target rate went from 0-25% to 4.5% in less than 12 months, 2X higher in the first 12 months of this hiking cycle as we experienced in the pre-financial crisis cycle…The rate risk may feel similar, but the ‘ruin’ is different. With credit risk somewhat stable, the risk is interest rates impact the value of bonds, not systemic credit repricing. Of course, there are risks and losses, but the problem is not the same as levered loans on inflated and sometimes worthless assets.

Like the super/hyperinflation we have been experiencing, the obvious is sometimes the right answer. When you add trillions of dollars to an economy with no acknowledgment of the impact that those dollars are going to have on inflation because some fancy formula was created to explain the outcome. Well, that is just arrogant! Too much money chasing too few goods is the simplest explanation of inflation. With no plan on how to withdraw this money from the economy would only leave more dollars circling through and these funds bypassed the banking system and were sent directly to the mailbox. The result, as a logical economist would argue is a super/hyperinflationary environment that is non-transitory. For policymakers to think otherwise was foolish. The cash needed a way to return to the “printer” so that it does not keep circulating causing higher and higher prices. If the price of goods spikes because consumers have more money to compete for scarce goods, why would the price come down, or be transitory, if the money was still in the economy? This ignorance is what caused the fed to raise rates higher and faster than anyone could imagine.

That miscalculation left the Fed in a conundrum. Aggressively raise rates and slow the economy, possibly creating a recession, or stick to the mantra that inflation was transitory and let inflation get even more out of control thus causing a more devastating recession. Since this was the biggest fiscal stimulus ever, with the largest increase in inflation ever, it should be no surprise that it would take the largest and fastest rate hike in 40 years to fight it.

And now we are seeing some of the consequences of being blind-sided, if not even being misled, about faster rate hikes. Banks took in record amounts of deposits during the pandemic and the savings rate hit new highs. Banks needed to invest these deposits (read: lend) but couldn’t do it fast enough, so they purchased what they thought were safe investments, US treasuries. As rates rose the value of these securities declined. These securities are held in two categories at banks; HTM or hold to maturity and AFS, available for sale. HTM does not need to be marked to market as they are expected to be worth 100 at maturity. However, if these bonds are sold prior to maturity, and a bank suffers a loss, the bank needs to record that loss now. As the yield curve inverted, investments that didn’t match maturities became problematic as borrowing long costs more than lending short term.

So this brings us to the current dilemma; death by inflation or by higher rates? Inflation impacts everyone, and one of the Fed’s mandates is price stability. However, raising rates can also cause problems for the economy. This leaves the fed with a dilemma, raise rates to fight inflation or lower rates to support the banking system (The economy seems ok so far).

To me it is a simple answer, raise rates as inflation is NOT under control in my opinion. Prices are inelastic to the downside, especially if wages are up and unemployment is low. So, my vote is to raise rates, just hope the yield curve becomes positively sloped in the process.

As for the stock market? The range for the decade could be set, with the possibility of a few percentage points near the lows and that wouldn’t be the worse thing to suffer. Because in a few years when this rate cycle is behind us, we could be headed into the greatest deflationary cycle we have ever seen. It’s too early to worry or prepare for that specifically, and I could be wrong, but stand by…Yikes!!

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-363101-2023-03-22