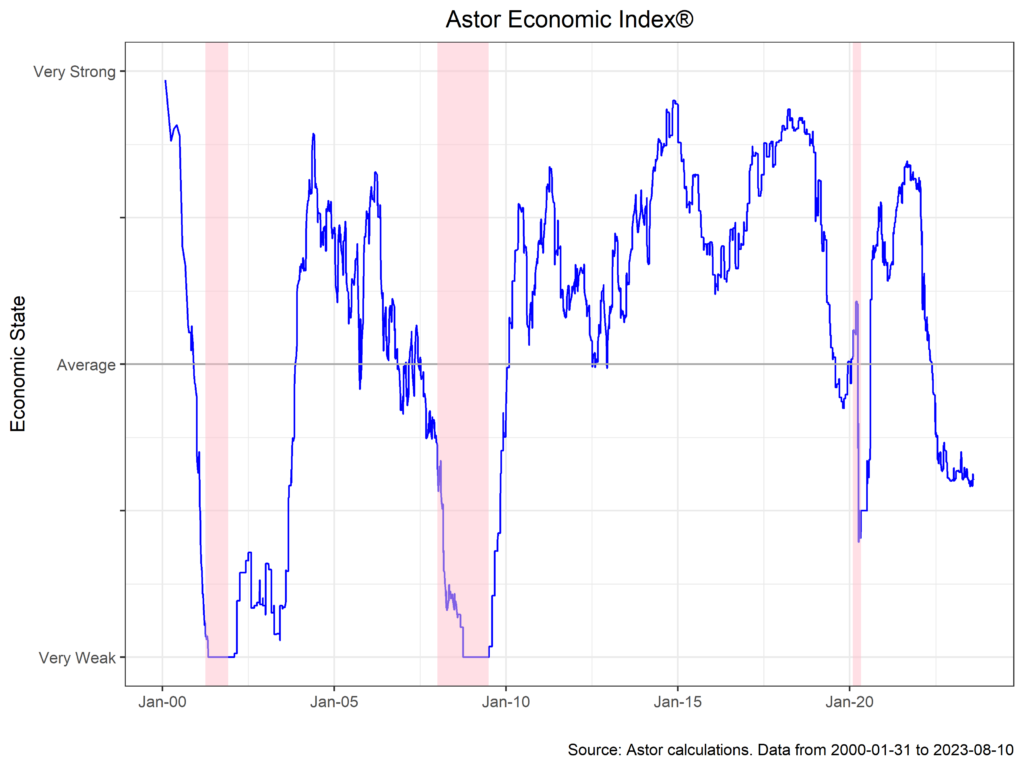

The U.S. economic picture has been essentially unchanged for the past few months, with a general trend towards disinflation, growth returning towards potential, and a secularly tight but slowing labor market. The Astor Economic Index® agrees with this narrative, ending the month of July at a level consistent with below potential output, driven mostly by poor manufacturing sentiment. We discuss the disparity between incoming hard and soft data and the near-term outlook for inflation below.

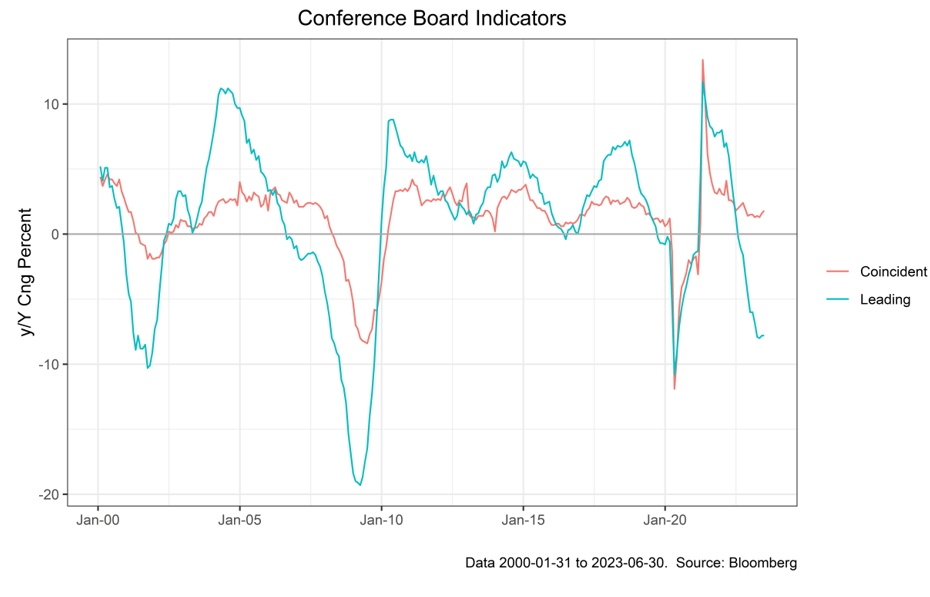

We have more data to measure the state of the economy than at any time in our past, and in a sense, we are spoiled for choice. Any number of narratives can be constructed about the health of the ongoing U.S. expansion depending on what series is emphasized. This muddle is exemplified in the growing contrast between observed (hard) data and survey (soft) data. As we’ve noted in the past, the labor market, a source of hard data, shows the U.S. is some ways from a recession, with the July non-farm payroll printing at a respectable 185,000 gain. Meanwhile, purchasing manager indices, which are survey based (that is, based on responses from purchasing managers), are quite pessimistic, with the July manufacturing PMI printing at 46.4 in contraction territory. The Conference Board aggregates some of these series into Coincident (hard) and Leading (mostly soft) indicators. The gap between these indices is historically large.

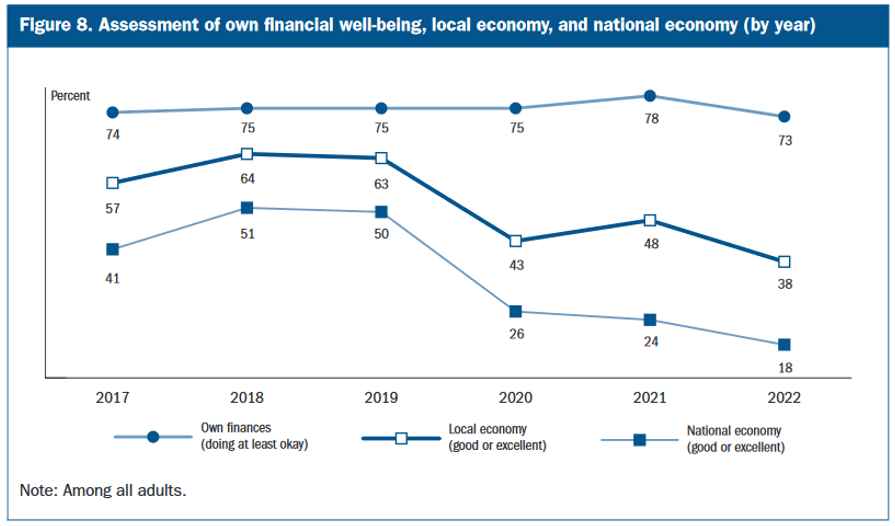

How do we explain this disparity? Interestingly, many Americans are increasingly pessimistic about the general state of the U.S. economy, but quite sunny about their personal finances and local economies. A meager 18% of survey respondents say the current economic situation is at least okay. However, 73% of the same respondents say their own finances are good. Politics certainly play a role, but a better explanation is probably fiscal transfers and real wage gains to lower-income households in the post-pandemic era.

Chart via Federal Reserve

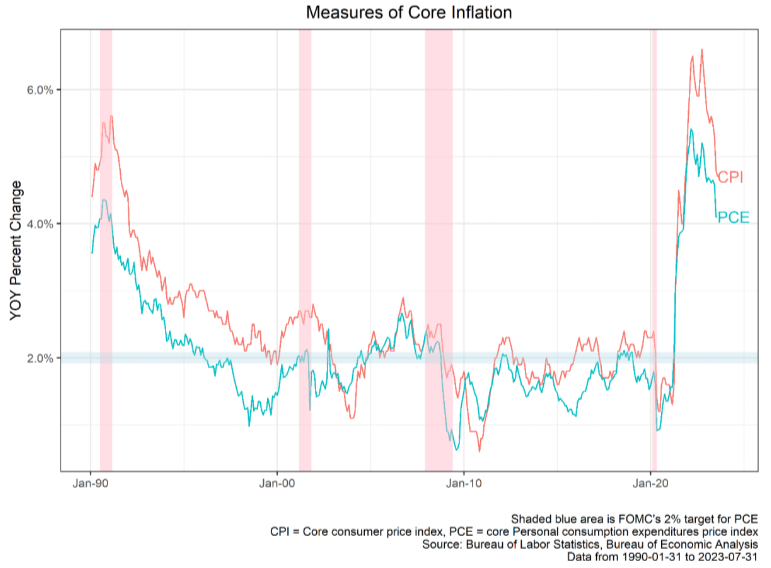

Inflation, meanwhile, printed at 0.2% m/m (3.2% y/y, core 4.7% y/y). It is less clear that inflation will follow a smooth glide path towards the Fed’s target of 2% core PCE. Several trends that have contributed in the past, like disinflation in energy, housing and health care costs, are likely to stop or outright reverse over the next quarter. The trend remains towards a durable cooling in price pressures, but inflation will have ups and downs over the course of the year.

As a result, the Fed saw enough evidence at the July 26th meeting to raise the policy rate by 25bps to a target range of 5.25 – 5.50%. The post meeting conference and subsequent communications by Fed officials indicate two schools of thought evolving within the FOMC. First, the Fed believes that the vast bulk of its work is behind it and has reached a level of rates roughly consistent with restrictive policy. As a result, the Fed can afford to be data dependent; that is, reduce forward guidance and react to data as they come in. The second is that the Fed believes that policy may need to be higher for some time as inflation remains modestly above target. NY Fed President John Williams recently stated that “I expect that we will need to keep a restrictive stance for some time”, a sentiment echoed by other Bank presidents. Given the turbulence of the inflation outlook, this is probably accurate, barring a marked cooldown in the labor market.

In sum, we see an economy that will continue to cool, although a recession in 2023 is not yet our base case. We expect inflation, and thus Fed policy and market pricing of assets, to zig and zag throughout the remainder of the year, although the trend, viewed in retrospect, will be towards disinflation. We will be watching key underlying components of inflation in the months to come, as well as higher frequency measures of the labor market.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services. The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-415145-2023-08-11