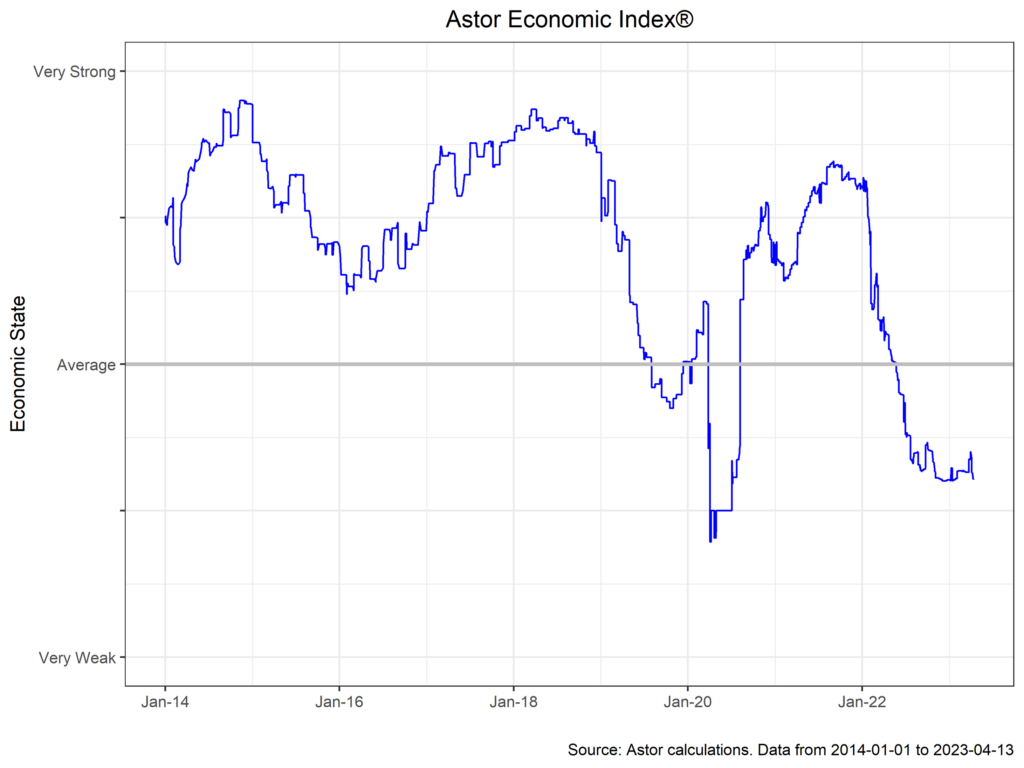

The data for the month of March showed a slight cooling of the U.S. economy but wasn’t fundamentally view changing for the domestic near-term trajectory. The Astor Economic Index® stayed in the same range that it began in 2023, at a level consistent with below-average growth.

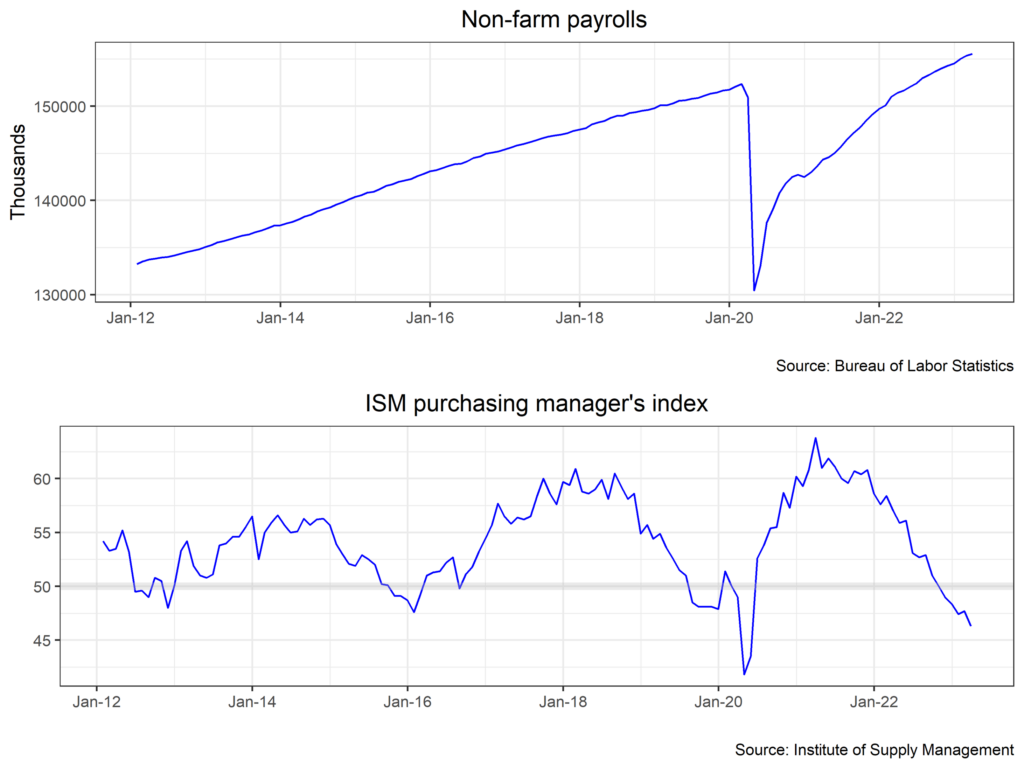

One of the big puzzles of the current macroeconomic cycle has been the (perhaps overly) robust labor market. Monetary policy works with a lag, and its impact on job hiring is somewhat indirect, but the Fed has singled out the tight labor market as a lodestar in making further progress in the fight against inflation. Low unemployment leads to competition for workers, pushing wages up (which printed up 0.2% m/m in real terms), and thus forcing prices higher as companies look to retain margins. Non-farm payrolls have averaged 351,000 m/m in the last 12 months, and March’s print of 236,000 was lower in the context of recent history, but still indicative of ongoing hiring and strong demand for labor. The Fed will probably take some small comfort in the slight cooling but will want to see lower gains in the months to come, as well as further cooling in wage growth.

Speaking of cooling, the ISM purchasing manager’s index for manufacturing continued its slide, falling further into contraction (i.e., below 50) to 46.3. The fall was led by declines in new orders and prices paid, the latter of which suggests that supply chains for manufactured goods have mostly healed. The ISM services PMI, meanwhile, fell from 55.2 to 51.2, still in positive territory but showing a substantial cooling in new orders. It is worth noting that other PMIs, like the series published by S&P/IHS Markit, are less adverse due to differences in the surveyed universe.

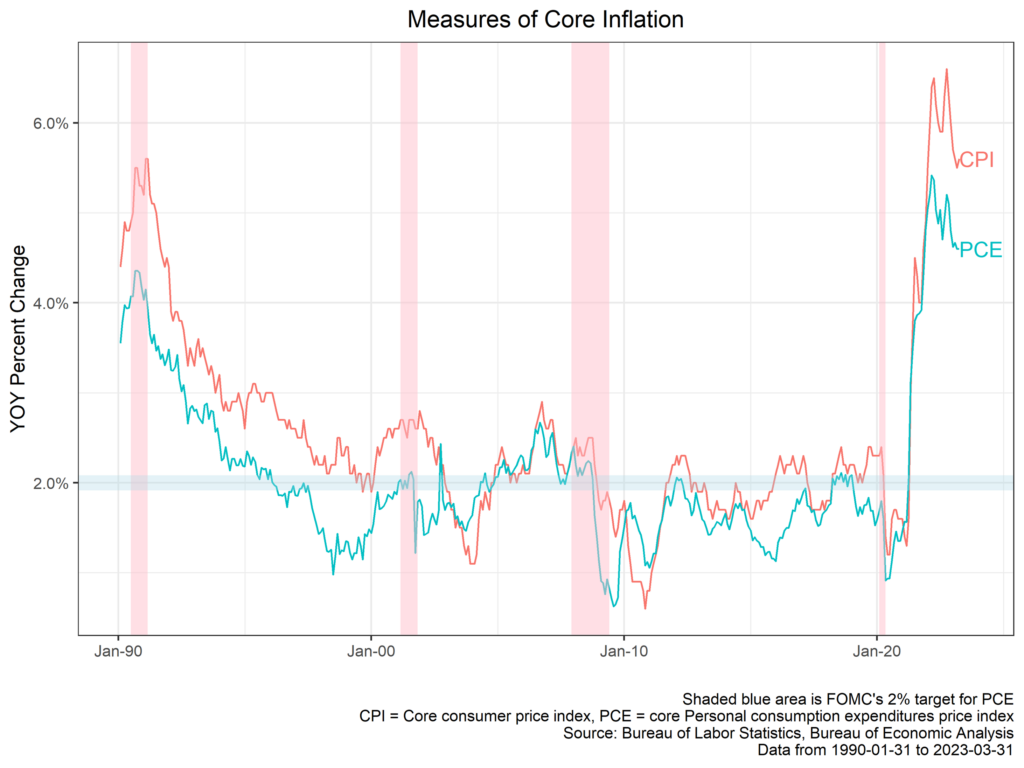

As the split in PMIs presages, inflation this year is mostly driven by services categories rather than the demand for goods we saw throughout the pandemic. Headline CPI for March printed at 5.0% y/y (0.1% m/m), with core higher at 5.6% y/y (0.38% m/m), about in line with estimates and a bit lower than the previous two months. Core prices were led by shelter (up 0.25% m/m, which is widely expected to cool in coming months) and transportation, and headline inflation was brought down by declining energy prices. There was something to like in this inflation print for both the doves and the hawks. On one hand, trimmed-mean inflation (which excludes big outliers), was the lowest in two years, as was the median CPI. On the other hand, the so-called supercore (which excludes food, energy, used cars and shelter), is still around 4%. Much of inflation, in other words, is dependent on shelter prices, but pressures are still broad.

In sum, the labor market and prices probably leave the Fed on track for a further hike of 25bps at the May FOMC meeting. Beyond that, it seems increasingly likely that the Fed may sit on the sidelines for a while to allow the effect of tighter policy to run its course. Market participants are increasingly convinced that the Fed will move into cutting mode in the second half of the year. Should inflation once again prove more persistent, or the labor market resilient, they may be in for a surprise.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

MAS-M-372889-2023-04-18