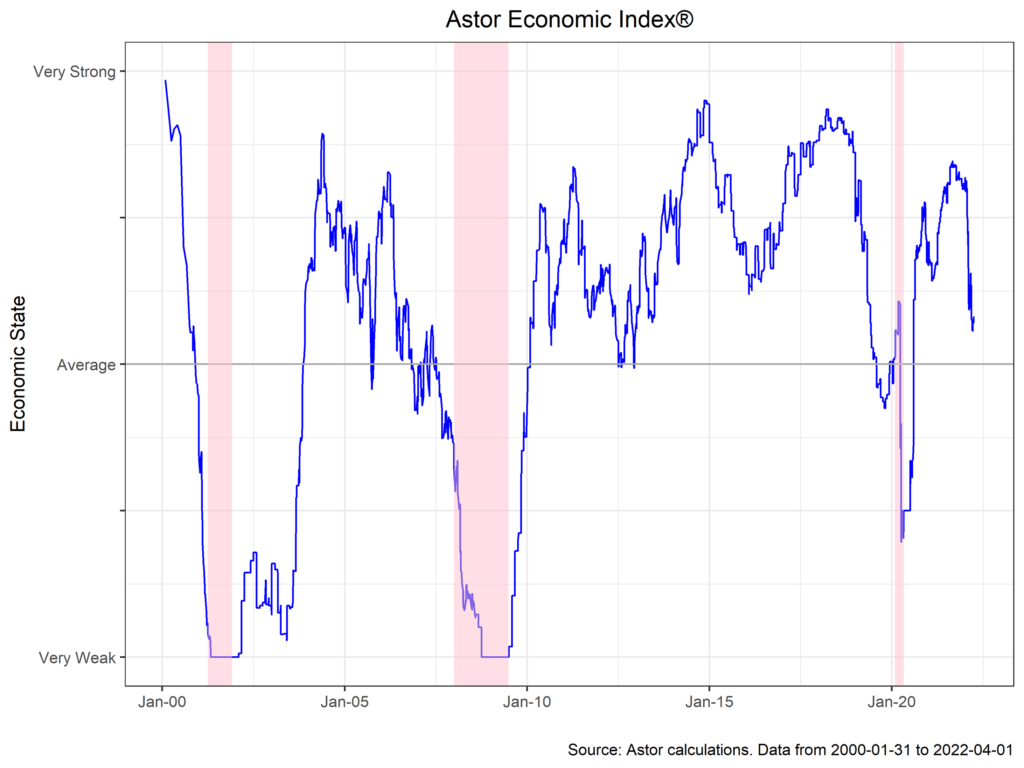

The Astor Economic Index continued its slide in March, consistent with our reading of a cooling but still strong economy. The domestic macroeconomic outlook is at an interesting crossroads, with persistent inflation, negative real wages, and high input costs on one hand, and very strong labor market dynamics, corporate earnings, and solid output growth on the other. In aggregate, of course, the sum of these observations gives the Federal Reserve substantial cause to tighten faster than they may have thought appropriate in the past, which we touch on later in this note.

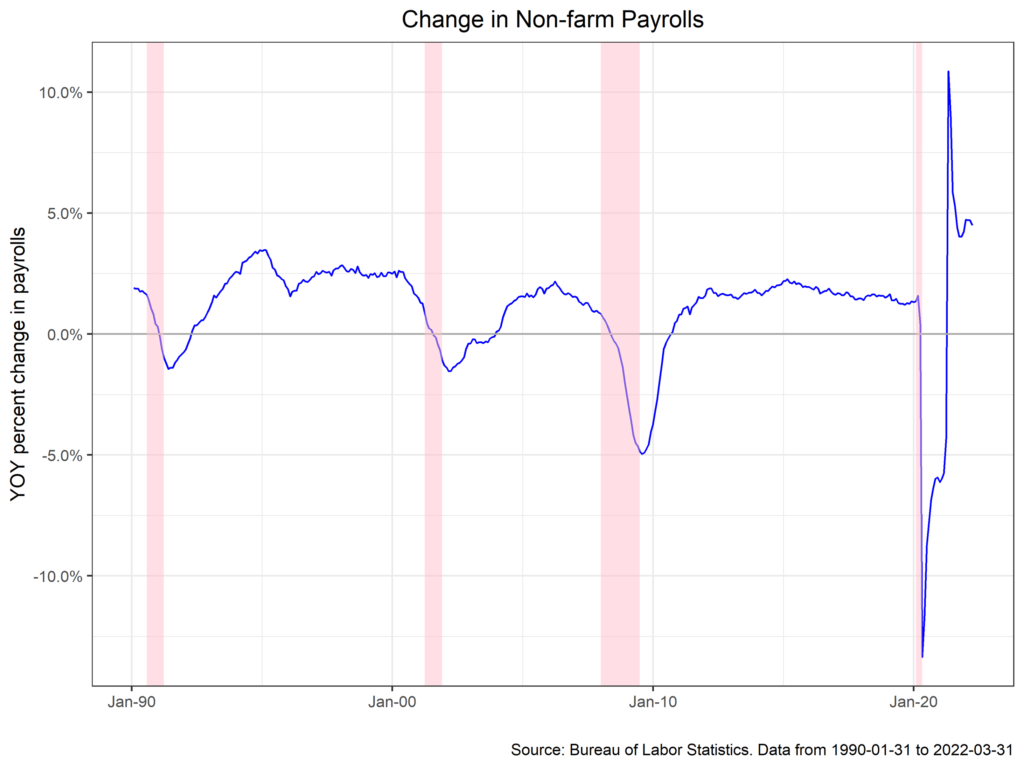

Non-farm payrolls have gone from the key data point of the U.S. economy to almost an afterthought, but the most recent print of 431,000 m/m shows that it is worth reiterating the strength of the U.S. labor market despite growing concerns about the trajectory of the broader economy. Its also worth noting the number of employees who have moved off the sideline and back into the labor market. Recall earlier concerns that structural shifts due to Covid-19 had permanently reduced the pool of available labor. It now looks like those worries were misplaced: prime age participation is on the rise as fiscal support rolls off consumer balance sheets and nominal wage gains lure workers back in.

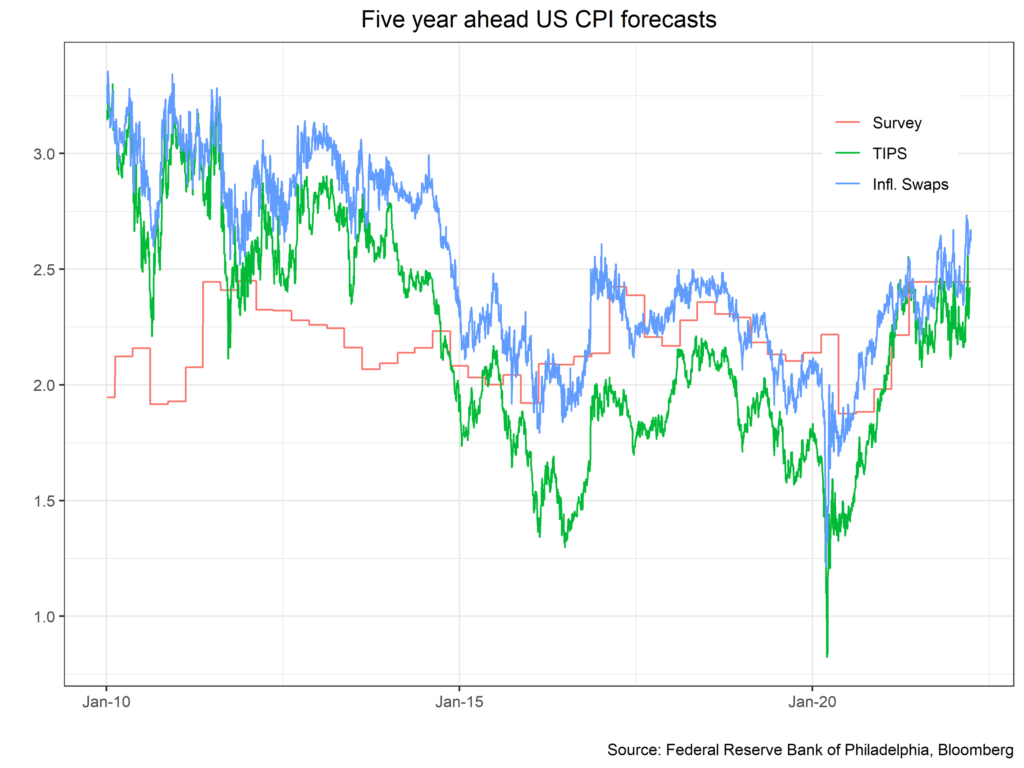

As a result, it’s reasonable to conclude that the labor market has reached or is approaching a level consistent with the Fed’s full employment mandate. Focus has thus turned to the other half of the Fed’s mandate (stable prices) and perhaps even to the oft forgotten third mandate of moderate long term interest rates. There is no doubt that inflation is hot and perhaps getting hotter: the most recent core PCE print, the Fed’s preferred measure, was 5.4% y/y. Curiously, forward inflation expectations, which the Fed pays attention to quite closely, have remained relatively anchored, suggesting market participations take the Fed at its word that it will do what it takes (as it has in the past) to tame inflation.

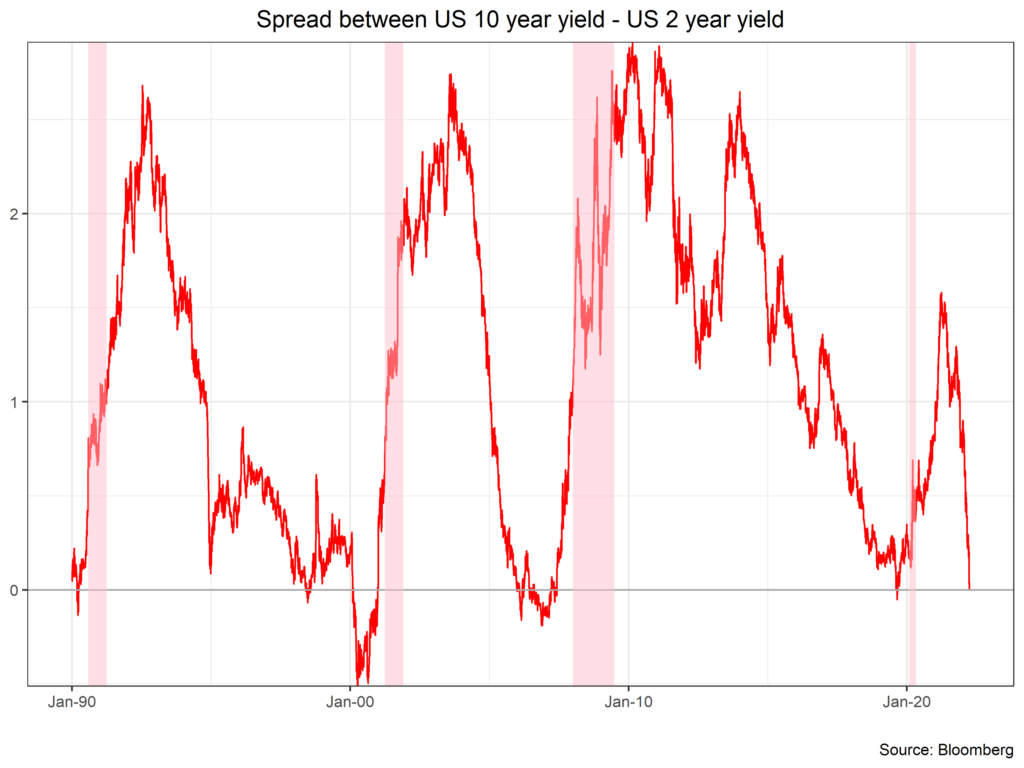

On that note, what should we expect the Fed to do over the coming year? Even prior to the first rate hike of the cycle FOMC participants began communicating substantially more aggressive forward guidance. St. Louis Fed President James Bullard recently suggested 350bps as an appropriate target rate for the Fed at the end of 2022. Quantitative tightening, if we must call it that, also looks to start in May, with $60bn of Treasuries and $35bn of agency debt (mortgages) set to roll off the balance sheet every month. Market participants have reacted accordingly, pricing in a faster path of hiking in near end rates.

Ultimately, the path of the U.S. economy in 2022 is highly dependent on how precisely the Federal Reserve guides the economy to a steadier state. It’s also worth remembering that some of the dynamics at play are well out of their hands – no amount of hiking will cause foundries in Taiwan to produce chips faster, or force OPEC + to pump more oil. Nonetheless, one thing the Fed can do for certain is cause a recession in the United States if they must. No one on the FOMC would find that a desirable outcome, and it is still not our base case, but should inflation prove stubborn, it is worth being well prepared for as the economy returns to potential. We will be watching the Fed and inflation dynamics closely over the coming months.

Astor Investment Management LLC is a registered investment adviser with the SEC. All information contained herein is for informational purposes only. This is not a solicitation to offer investment advice or services in any state where to do so would be unlawful. Analysis and research are provided for informational purposes only, not for trading or investing purposes. All opinions expressed are as of the date of publication and subject to change. They are not intended as investment recommendations. These materials contain general information and have not been tailored for any specific recipient. There is no assurance that Astor’s investment programs will produce profitable returns or that any account will have similar results. You may lose money. Past results are no guarantee of future results. Please refer to Astor’s Form ADV Part 2A Brochure for additional information regarding fees, risks, and services.

The Astor Economic Index®: The Astor Economic Index® is a proprietary index created by Astor Investment Management LLC. It represents an aggregation of various economic data points. The Astor Economic Index® is designed to track the varying levels of growth within the U.S. economy by analyzing current trends against historical data. The Astor Economic Index® is not an investable product. The Astor Economic Index® should not be used as the sole determining factor for your investment decisions. The Index is based on retroactive data points and may be subject to hindsight bias. There is no guarantee the Index will produce the same results in the future. All conclusions are those of Astor and are subject to change. Astor Economic Index® is a registered trademark of Astor Investment Management LLC.

AIM-4/8/22-BP559